Simon Watts

Reveal Menu

2024 End of Year Market Update: The Times They Are A-Changing

We entered 2024 expecting a year punctuated by democratic elections and a continuation of geopolitical tensions. What we experienced was a pivotal year in global politics, marked by significant events, seismic power shifts and no resolution to the ongoing conflicts in Ukraine and Gaza. After the dust settled on 74 national elections (plus the EU parliamentary election) we bid “farewell” to Biden, Sunak and Kishida, “hello” to Trump, Starmer and Ishiba, and “as you were” to Modi, von der Leyen, Putin and Zelensky.

Looking back on a momentous year in political terms, we see that from a markets perspective the dominant factors that directly influenced investment returns were still inflationary pressures, central bank policies and corporate earnings, and as we shall see, these impulses were largely positive for equity markets.

Bonds

The market exuberance and optimistic trajectory for interest rate cuts we started with in 2024 was dealt a dose of reality in January when the Bank of England and the US Federal Reserve both intimated that they will not be rushing to lower rates until there was conclusive evidence that the labour market had slowed down to bring wage growth to sustainable levels.

Consequently, UK government debt (gilt) yields rose sharply at the start of the year as expectations were revised to rates remaining higher for longer. A strong (though slowing) US economy ensured their rates remained stable, plus growing UK political uncertainty spurred by speculation over the timing of a general election led gilt yields higher into the mid-year.

Inflation falling closer to the Bank of England target of 2% and a resounding election victory for Labour gave hope for a period of relative stability and brought some respite for yields from July onwards. However, by September yields were rising again as the US economy remained stubbornly strong, and polls indicated a second Trump presidency could become a reality (which is relevant because his domestic and foreign trade policy is anticipated to be inflationary).

Source: Financial Times

Over the year, gilt yields rose strongly from 3.5% to 4.6%. This may not sound much of an adjustment, but it is a yield shift of over 30%, and as bond yields normally perform inversely to their valuations, this is negative for capital values.

Over the last quarter, the MSCI Markit Iboxx Gilts index finished the year 4.0% lower. Our gilt exposure consists mainly of a holding in the passively managed Vanguard UK Government Bond Index, which returned -4.4%. However, this was improved upon by our decision to disinvest fully from the fund ahead of the Budget in October and reinvest in November, which saw us add value by repurchasing at a price that was 1.5% lower than when we sold it.

Premier Miton Strategic Monthly Income (held in Cautious and Balanced portfolios) led the way with an annual return of 8.0%, followed by the Artemis Strategic Bond and Rathbone Ethical Bond funds with returns of 5.2% and 5.1% respectively. Nomura Global Dynamic Bond (held in Adventurous portfolios) returned 4.2% over the year.

Further interest rate cuts in 2025 should provide a tailwind for bond valuation, but inflationary stimuli such as a strong US dollar and the impact of employer National Insurance contributions in the Budget being passed on as price increases could limit UK rate cuts. We will maintain our current level of bond exposure and have no plans to increase it further at present.

Interest Rates & Inflation

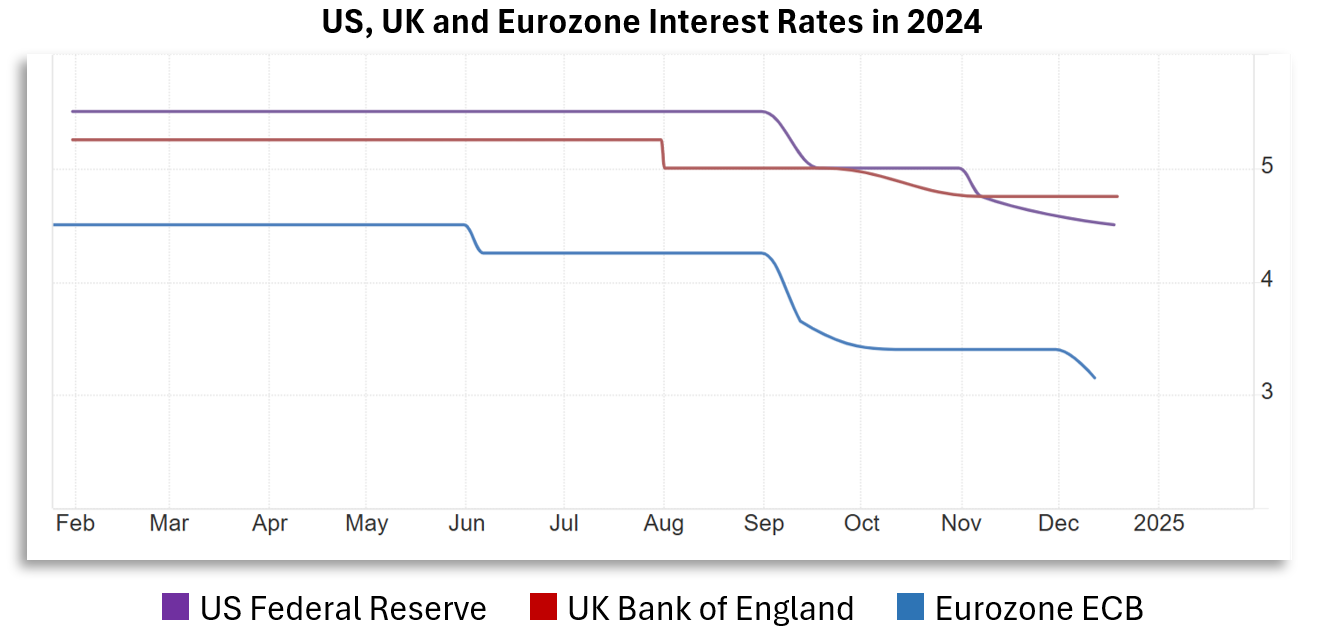

Towards the second half of 2024 the Federal Reserve, Bank of England and European Central Bank finally commenced the interest rate cuts they first signalled in November 2023. The Fed cut rates 3 times by a total of 1%, the BoE twice by 0.5% in total and the ECB 4 times by 1.35% in total to rates of 4.5%, 4.75% and 3.15% respectively. The UK now has a higher base rate than the US for the first time since 2022 (briefly) and before that 2015.

Source: Trading Economics

The Bank of Japan unexpectedly raised rates by 0.25% in August due to continuing Yen weakness, causing widespread (though mercifully brief) consternation in global markets. This is because a stronger Yen has a huge impact on global liquidity due to what is known as the “carry trade”, where investors borrow in low-yielding currencies such as the Yen, to invest in higher-yielding ones. The surge in the Yen caused investors to unwind these positions, causing a sell-off in global risk assets (e.g. shares).

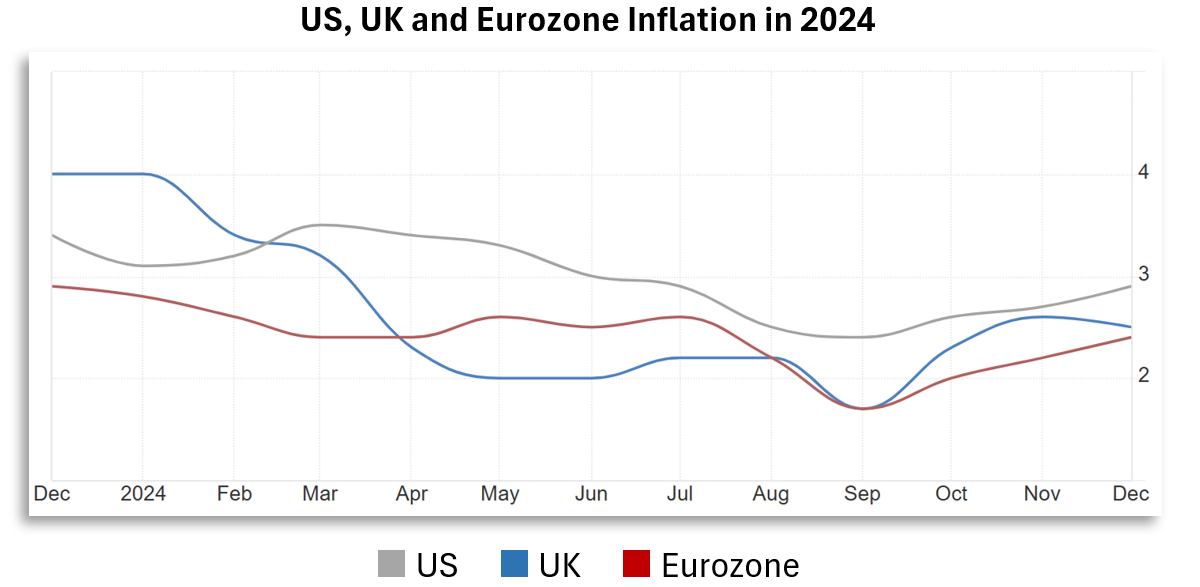

US, UK and Eurozone inflation remained buoyant throughout the year, but in a range much lower than we have seen since mid-202. Briefly, UK and Eurozone inflation dipped below their policy target rate of 2% briefly before rising again.

Source: Trading Economics

With US inflation trending upwards without having reached the Fed’s 2% target, their case for interest rate cuts is weaker, unless their economy weakens significantly. We would expect US equity and bond markets to remain sensitive to any economic data releases and Fed guidance/announcements in 2025.

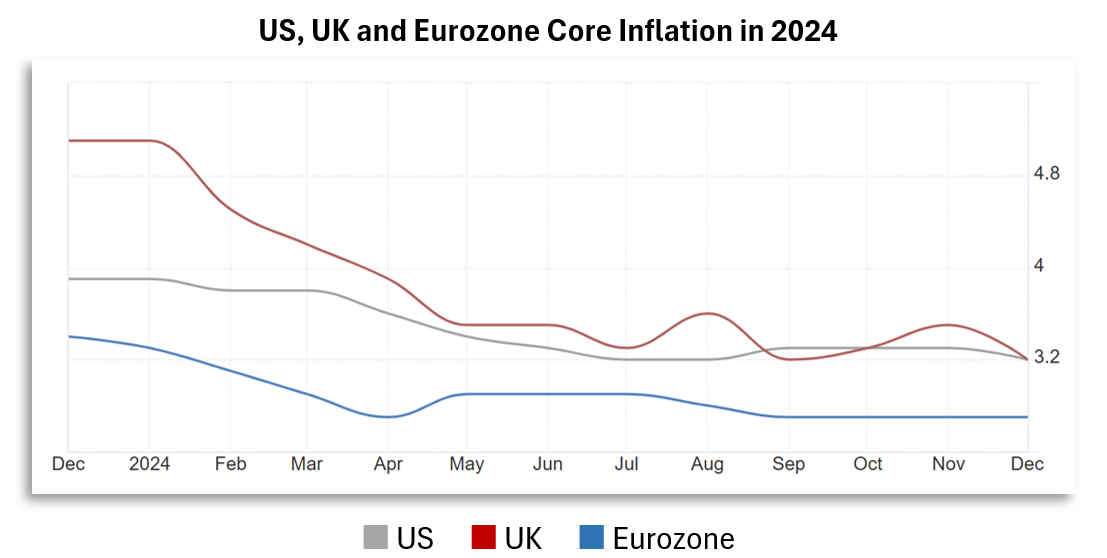

One set of data that might provide some justification for further rate cuts is core inflation, which appears to be either trending downwards or stable. Core inflation is important as it measures the price of a selection of goods and services but strips out more volatile prices such as food and energy, and is keenly watched by Central Banks. In December, UK core inflation dropped to a 4-year low of 3.2%.

Source: Trading Economics

Inflation in 2025 will be largely beholden to the rate of global economic growth and the trade policies Trump may pursue – whilst predictions can be obtained for the former, the latter is currently a mystery.

UK Equities

2024 was another positive year for UK equity funds, almost regardless of market capitalisation and style, as lower inflation led to slightly lower interest rates later in the year, but optimism over future rate cuts led to a surge in confidence in the first half of 2024.

The Large Cap Value-biased MSCI United Kingdom index was up 9.1% for the year, reflecting the outperformance of Large Cap and Value stocks; the MSCI United Kingdom Large Cap and MSCI United Kingdom IMI Value indices rose by 11.1% and 11.9% respectively.

Unsurprisingly then, fund holdings with a Large Cap and/or Value bias outperformed in 2024. Leading the way was Artemis UK Select, which replaced the JO Hambro UK Dynamic fund in March. The estimated fund return from holding JO Hambro and then Artemis from March was 21.4% for the year, relative to the JO Hambro UK Dynamic annual return of 11.5%. JO Hambro UK Equity Income returned 20.1% and our other core UK holdings returned between 8.9% and 16.1%. Disappointingly, Liontrust UK Smaller Companies produced a return of -0.3%, following a very strong performance in the final quarter of 2023.

The UK’s economy has shown resilience over the last couple of years, but there are ongoing concerns about inflation and economic growth post-Brexit. Inflationary pressures and corporate tax increases could affect consumer spending and corporate margins, impacting equity market performance, though there are many individual UK companies that will continue to perform robustly almost regardless of these conditions. For this reason, we continue to favour of an actively managed (stockpicking) approach for our UK equity exposure.

UK equity valuations remain compelling, unlike the eye-watering (and arguably unsustainable) valuations of certain US big tech-related companies who have already seen significant share price growth. We therefore continue to believe that selective UK equity exposure remains appropriate due to its long-term growth potential and to dampen US market risk.

Overseas Equities

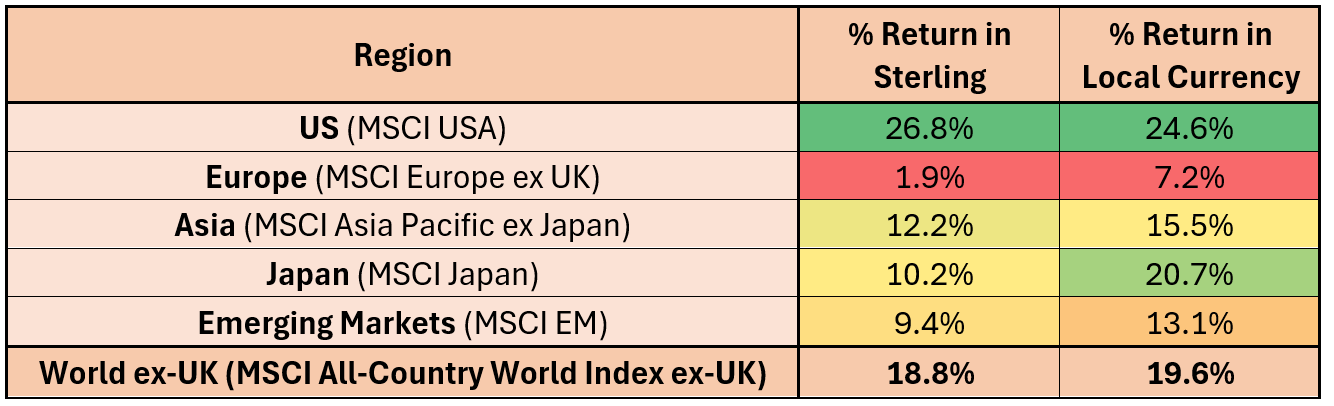

Index performances for overseas equity markets in 2024 are shown below in both Sterling and local currency:

The above table shows that US equities led the way in 2024, followed by Asia and Japan. However, we can also see that currency fluctuations have more than halved the return we should have enjoyed on Japanese equities and reduced the return on other overseas markets except for the US, where the stronger dollar has enhanced returns for UK-based investors.

The effect of currency fluctuations of overseas holdings should always be borne in mind when building or managing an investment portfolio, and aside from US equities we can see that most of the returns from our UK equity holdings have been superior to the Sterling-adjusted returns from overseas holdings in 2024.

Of our global equity holdings, the Polar Capital Global Insurance fund produced an excellent return of 26.8% for the year, whilst the rules-based, passively managed iShares Edge MSCI World Quality Factor ETF and Rathbone Global Opportunities fund returned 18.7% and 17.2% respectively.

North America

The US represents a fascinating investment opportunity that has produced some extraordinary returns in recent years, with the S&P 500 index soaring again in 2024 – albeit riding on the back of the “Magnificent 7” stocks (Apple, Nvidia, Microsoft, Amazon, Alphabet, Meta Platforms and Tesla).

However, a prolonged period of outperformance has seen the valuation of most of these stocks stretched beyond reasonable bounds (even for the US) and they are overly represented within the S&P 500 index, accounting for nearly a third of its market capitalisation. Indeed, these companies are now so large that they currently account for almost a quarter of the MSCI World index, and Apple, Nvidia and Microsoft are now each worth more than the FTSE 100 index (UK’s 100 largest companies). These companies are absolutely huge and can skew a whole index when they individually outperform (as some have recently). Our concern is that this outperformance cannot last indefinitely, and they present a significant downside risk if held in high proportions. Add to this the uncertainty Trump could bring to their domestic politics, there will clearly be winners and losers amongst US companies.

Nevertheless, the US is still the world’s largest economy, with a strong reserve currency, technological advantages in many sectors and is widely regarded a relative safe haven in times of economic and geopolitical uncertainty. When the Covid epidemic saw half of the global economy shut down, US equities outperformed; if the world’s current worrying geopolitical backdrop worsens, we would expect US equities, bonds and the dollar to continue to perform robustly relative to other equity markets and currencies.

Our view towards the US has therefore modified in recent months from pursuing a neutral weighting to a slightly positive one. That said, whilst we do have exposure to Magnificent 7 stocks we also “allocate around” them so that we do not have the same weightings in them that pure index exposure would provide. We do this by holding small and mid cap stocks, large cap industrials and financials as well as themes such as Insurance, Healthcare, Infrastructure and Artificial Intelligence.

Our core S&P 500 ETF holding returned 26.9% in 2024, whilst our remaining US equity holdings returned between 11.0% and 13.9%. However, as shown above our thematic Polar Global Insurance holding produced practically the same return with zero Magnificent 7 exposure.

Predictions for the US economy of a mild recession in 2024 were completely off the mark, though in 2025 the economy is expected to experience a slowdown in growth, following the tightening of monetary policy in previous years. Inflation is expected to moderate further, but consumer spending, which drives a significant portion of US gross domestic product, will be under pressure as interest rates remain higher for longer. We remain cautiously optimistic for US equities.

Europe

European equities struggled in 2024 as economic growth wavered (hence the faster trajectory of ECB interest cuts), with the manufacturing sector bearing the brunt of high energy costs, weak export demand, and widespread and costly regulation.

Concerns remain that European auto manufacturers failed to innovate over the past 30 years, investing in diesel and petrol vehicle development and underinvesting in hybrid and electric vehicles, leaving themselves exposed to Chinese competition.

Political woes persisted in Germany and France where the rise of Far-Right political parties reveals underlying and growing concerns and frustration around rising taxation (already among the highest in the world in France) and immigration. Limited exposure to Artificial Intelligence also weighed on the relative performance of European equities, leaving the Eurozone trailing behind global peers. However, some sectors, such as luxury goods, continue to perform strongly.

Our single European equity holding (BlackRock European Dynamic) returned a modest, but benchmark-beating return of 3.6% over the year.

We remain underweight European equities and continue to keep this under review.

Japan

Japanese equities were the second-best performing overseas equity in 2024, having outperformed the US equity market by 2% in 2023, but as happened in 2023 the Japanese Yen depreciated even further against Sterling (despite the fact the UK cut rates by 0.5% and the Bank of Japan increased them by 0.25%), halving the Japanese equity benchmark return in Sterling terms.

Over the year, the Japanese equity market exhibited notable resilience and growth, driven by a combination of domestic economic factors and broader global trends. Government stimulus measures, alongside a gradual recovery in consumer spending helped support investor confidence. Strong industrial production and positive business sentiment contributed to the bullish sentiment and Japan’s exporters, especially in the tech and automotive sectors, took advantage of the weaker Yen and solid demand from overseas markets.

We have made some changes to our Japanese equity allocation, but our two constant holdings for 2024, M&G Japan and iShares Core MSCI Japan IMI ETF returned 11.7% and 9.5% respectively in 2024.

We slightly reduced our Japanese equity weighting in 2024 but remain overweight and will continue to do so for the foreseeable future.

Asian & Emerging Markets

In 2024, China’s equity market experienced a year of mixed performance. After a poor start to the year China’s economy showed signs of stabilisation and recovery. However, as economic growth and equity markets began to flounder in the third quarter, the Chinese Communist Party and People’s Bank of China announced several fiscal and monetary measures to stimulate economic growth. Whilst many economists are sceptical of the likely long-term effectiveness of these measures, they nevertheless buoyed Chinese equities temporarily, and the MSCI China index finished the year 21.6% higher. Excluding Japan and China, Asian equities returned 9.0% for the year (FTSE Asia Pacific ex Japan ex China).

The Chinese government is likely to continue pushing structural reforms, especially in sectors like real estate, technology and energy. Any significant reform could either provide a boost or cause further market volatility. Government intervention and increased regulation, particularly in the tech sector will be a key determinant of future investor demand. The trade relationship between China and the US under Trump will also be a significant factor, as any escalation in tensions or a change in trade tariffs could negatively impact Chinese equities.

Most Asian equity markets finished in positive territory, though there was a wide dispersion of returns. The top performer was Taiwan, with the MSCI Taiwan index finishing the year 36.8% higher, in stark contrast to the MSCI Korea index, which finished the year 22.0% lower. Whilst political upheaval in South Korea escalated in December, their equity market had already been in decline for several months.

In 2024 our Asian equity funds – Schroder Asian Alpha Plus and Stewart Investors Asia Pacific Leaders Sustainability – returned 11.4% and 6.7% and our sole Emerging Markets equity holding (Fidelity Emerging Markets) returned 7.1% for the year.

In other Emerging Markets, Latin American nations generally struggled, with the exception of a resurgent Argentina, whilst India enjoyed another good year with the MSCI India index rising 13.6%. Emerging European equities returned around 7%.

We monitor Asian and Emerging Markets closely, as despite their recent significant challenges they have the potential to outperform over the coming years; whilst we do not have any immediate plans to add to our existing exposure, we are likely to do so as soon as we believe the fundamentals have improved.

Portfolio Performance & Changes

Portfolios across all risk categories in the main will have finished firmly in positive territory, with the more equity-heavy Adventurous portfolios outperforming as they did in 2023. In performance terms they will have now made up for and moved on from the extraordinarily negative market conditions of 2022, which challenged all of the main asset classes.

Previous monthly commentaries have detailed the changes we have made to portfolios, but it is worth summarising the broad direction of portfolio changes throughout the year.

Following the steep fall in gilt prices in January, we invested from cash balances into the Vanguard UK Government Bond Index fund. We added to this holding in June and, as alluded to earlier in this commentary, we sold this holding in full in the run up to the October Budget, buying it back in November and taking advantage of further price falls in the interim.

In March we sold the JO Hambro UK Dynamic holding, having been notified of the fund manager’s intention to leave the group. We reinvested the proceeds into Artemis UK Select, having followed the progress of the fund manager Ed Legget for some time. This proved to be a good move in relative returns to date. At the same time, we also sold the iShares Edge MSCI World Value Factor ETF holding and purchased the iShares Edge MSCI Global Quality Factor ETF in recognition of the changing economic backdrop, which should see global Quality stocks outperform as inflation bottoms out and interest rates begin to fall. Again, this proved to be a worthwhile change, with the difference in return for the remainder of the year being 7%.

For Cautious portfolios, in March we also sold their existing Asian equity holdings (either Schroder Asian Alpha Plus or Stewart Investors Asia Pacific Leaders Sustainability) and purchased the Jupiter Asian Income fund, which has zero exposure to Chinese equities. This “de-Chinafication” change was made with the intention of managing portfolio risk for Cautious clients, acknowledging that they also had exposure to Chinese equities within the Fidelity Emerging Markets fund.

We reduced weightings in M&G Global Listed Infrastructure in June to widen our thematic exposure into Healthcare, purchasing the Polar Healthcare Blue Chip fund. Relative returns have been similar, though it is early days – we believe that over the long-term portfolios will benefit from this additional diversification.

In October we reduced our Japanese equity exposure in favour of US equities, reinvesting the proceeds into the Invesco S&P 500 Equal Weight ETF. As the name implies, this fund holds each of the index constituents in equal measure, avoiding the heavy bias towards Magnificent 7 stocks, and was added to complement the existing iShares (market cap weighted) S&P 500 Index ETF holding. At the same time, we rationalised our Japanese equity exposure, selling our longstanding holding in ManGLG Japan Core Alpha holding and retaining the M&G Japan and iShares Core MSCI Japan IMI ETF holdings.

Finally, to cap off a relatively busy year for portfolio changes in November we added to the newly-established Invesco S&P 500 Equal Weight ETF to tilt portfolios slightly further towards US equities, reducing holdings in Fidelity Emerging Markets, M&G Global Macro Bond or Vanguard UK Government Bond Index respectively for Cautious, Balanced and Adventurous portfolios.

Conclusion

Simply put, compared to 3 years ago the world seems to be in a better place economically (lower inflation and falling interest rates) but in a worse place geopolitically (war in Ukraine, greater volatility in the Middle East and the prospect of a more confrontational approach to US/China relations and global trade). We are arguably in a new Cold War phase, the difference being that this time it is multipolar, and the “Peace Dividend” era we have enjoyed in the West for the last 30 years (when economies benefitted from diverted funds from military spending cuts) is now definitively behind us.

From a consumer perspective, practically everything is significantly more expensive than it was 3 years ago, which for many leads to a greater level of caution when making financial decisions. The cost savings incurred by Covid lockdowns and the money saved therein has largely been spent, and these factors all have implications for future corporate earnings.

Business confidence varies geographically and is also sector specific. In the UK, large employers of predominantly minimum wage workers will feel the pinch of employer National Insurance increases, which could result in price rises, reduced expansion plans, reduced recruitment or even redundancies (or a combination of these). This could be both inflationary and detrimental to future corporate earnings.

Climate change also drives the political agenda, with some countries pursuing Net Zero policies with more vigour than others, pushing up energy costs but driving innovation in new cleaner energy technologies. This, along with immigration policies are fuelling political unrest in Western Europe and beyond.

Turn on any news channel and all of these issues can meld into a single, worrying narrative of global turmoil and decline. Yet, if we step back from the noise of a news media that deliberately appeals to our fear instinct to grab our attention, we can see that there are plenty of positive factors that, at least from a markets perspective, can drive positive performances for portfolios.

As the world changes, opportunities change as well, and we must be mindful that we adapt our strategies to continue to profit from them. A second Trump presidency may export all sorts of instability to different parts of the world but it could also benefit others. For example, “friendshoring” has seen China lose industrial production but India and Vietnam gain it. The development of AI capabilities will require huge expansion of data capacity and digital infrastructure. Efforts to tackle climate change presents investment opportunities in new technologies and resource management.

History has shown that investors with the foresight and courage to invest through market cycles and political uncertainty are ultimately rewarded, often because they are already holding the investments everybody else demands once the outlook becomes clearer.

As always, we will continue to invest with our focus on the medium (3 to 5 years) to long term (5 years plus) and will modify our investment approach as changing conditions require.

THE BOOLERS INVESTMENT COMMITTEE