Richard Borrington

Reveal Menu

3 financial insights we’ll be factoring into our client advice this year

Financial headlines over the last couple of years have been dominated by the cost of living crisis. Record-high inflation and soaring energy bills have left millions of UK households feeling the squeeze.

So far, 2024 has brought calming inflation but confirmation of a recession. There’s also the potential market upheaval of elections in the US and at home.

The year is set to be unpredictable but there are some forecasts and potential trends worth noting. We can use these to help ensure the advice we give to our clients is the best for them.

Keep reading for your look at what 2024 might bring for financial markets and global headlines and how our expert knowledge could help you and your clients.

1. Economic growth is set to improve, but not until 2025

Latest figures from the Office for National Statistics (ONS) confirm that the UK has dipped into a recession.

ONS figures estimate that the UK’s Gross Domestic Product (GDP) fell by 0.3% between October and December 2023. This followed a 0.1% fall in the previous quarter.

GDP is estimated to have increased by 0.1% overall in 2023, compared with 2022. But, taking to X (formerly Twitter), the Resolution Foundation confirms that this amounts to a near-24% drop compared to the dominant trend before the 2008 financial crisis.

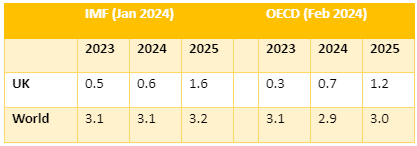

On 15 February, the government published GDP growth forecasts from the International Monetary Fund (IMF) and the Organisation for Economic Cooperation and Development (OECD).

Source: House of Commons library

The IMF and OECD predict minimum economic growth for the UK in 2024. Both organisations forecast that the US and Eurozone will see similar growth to the UK, with only China and India pushing up the world average.

The Guardian confirms that the governor of the Bank of England (BoE), Andrew Bailey, believes there are already signs of an economic upturn, which will make themselves known in the coming months.

2. Inflation will fluctuate but end the year stubbornly above its target

Inflation began to rise in the summer of 2021, hitting a 41-year peak in October 2022, of 11.1%. The target for the Consumer Prices Index (CPI), as set by the BoE, is 2%.

One of the measures the BoE uses to control inflation is the base rate and this currently stands at 5.25%.

At the latest meeting of its Monetary Policy Committee (MPC), the BoE stated that inflation hadn’t fallen as quickly as they’d anticipated.

Inflation is now expected to hit its 2% target, though only temporarily, in Q2 2024, before rising again for the rest of the year. The rise could be moderate though, reaching around 2.75% by December.

In a change to previous projections, the MPC now expects CPI to hit 2.3% by 2026, and not reach its 2% target until 2027.

High prices will remain a significant factor for clients for the foreseeable future. This impacts everything from your clients’ household budgets to the buying power of their pension payments.

3. Global elections and geopolitical events will cause uncertainty in the markets

The US and UK populations are heading to the ballot box in 2024, but we’re not the only ones. More than 50 countries and 4 billion people will be taking part in the biggest election year on record.

The US presidential race has the power to affect global markets. With the stability (if somewhat under-par performance) of markets under Biden facing off against the uncertainty a Trump win would undoubtedly cause.

For UK investors, sticking to their long-term plans and ignoring geopolitical noise will be key.

Then there’s the UK general election to consider.

The Times Money Mentor looked at the FTSE All-Share Index since 1962 and found that performance was better in the 12 months leading up to an election than in the 12 months that followed (8.9% compared to 6.9% on average).

The winner of the election can also make a difference, though. Quoting figures from AJ Bell, Money Mentor finds that the average return was just 0.9% for the 12 months after an in-power government retained control. This compares to average returns of 12.8% when an opposition party came to power.

While stock markets are generally accepted to hate uncertainty, it appears this doesn’t necessarily hold where governments are concerned. A Labour win would lead to more uncertainty, in terms of policies and potential changes to recent Conservative announcements, not least on the Lifetime Allowance.

Whatever happens come the general election, and in the wider world – with conflict continuing in Ukraine and the Israel-Hamas war – investors must remember that their plans are long term. The key will always be to stay focused and ride out short-term economic dips to achieve long-term returns.

Get in touch

If you have clients who might benefit from the financial insights Boolers’ team of expert finance professionals can offer, get in touch. Email enquiries@boolers.co.uk or call 0116 240 7070.

Please note

A pension is a long-term investment. The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Your pension income could also be affected by the interest rates at the time you take your benefits.

This article is for information only. Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.