Chris Ball

Reveal Menu

3 financial lessons we learned in 2020

2020 was a challenging year. National lockdowns, job insecurity, and the threat of coronavirus itself might have left your clients thinking about the things that truly matter to them.

With challenges set to continue into 2021, now is a great time to look back and reflect. Here are three lessons we learnt in 2020 that your clients can take into the new year.

What clients value most

The arrival of coronavirus and the subsequent UK-wide lockdown in March affected everyone differently. Some of your clients might have been forced to stay away from family and friends for an extended period, either to shield or protect a shielding family member. Others might have been furloughed.

For clients whose social interactions centre around their employment, a prolonged spell away from the office might have made clear how crucial the work environment is. For others, lockdown might have highlighted the importance of spending time with family.

We can help your clients formulate a long-term retirement plan based on their financial position as well as their values.

A client who missed the social interaction of the workplace might consider a move to phased retirement. For those clients who missed the time spent with children or grandchildren, we might help them to increase their pension contributions to allow for earlier retirement.

2020 helped teach us what we value most. Whatever matters most to your clients, we can help action an existing plan or formulate a new one.

2. The benefits of staying calm and focussing on the long-term

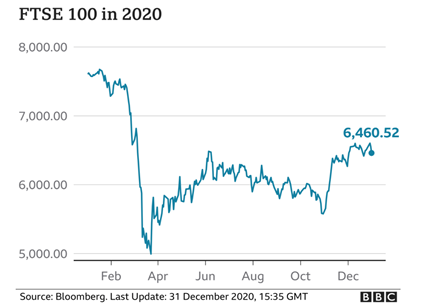

In March 2020, the FTSE 100 fell by 10%, marking its worst day since 1987. The Dow Jones and the S&P 500 experienced similar declines. Over 2020 as a whole, the BBC reports that ‘the FTSE 100 fell 14.3%, its worst annual performance since the 2008 global financial crisis’.

Despite this poor performance, 2020 taught investors some valuable lessons.

The message we gave our clients last year was don’t panic, stay invested, and focus on the long term. It might have been a difficult year, but it is clear that withdrawing funds at the height of the crisis in March would have seen investors miss out on the gains that followed.

Source: BBC

Investment should always be a long-term strategy and 2020 highlighted the reasons for this.

Short term market volatility is to be expected, no matter what the cause. Keeping calm and non-emotional isn’t easy – and it’s been even more difficult during the pandemic – but remaining invested is the best way for your clients to see a recovery.

Blips will occur but the general trend of the markets is an upward one. By staying strong when markets are down, your clients stand the best chance of taking advantage of market upturns when they arrive.

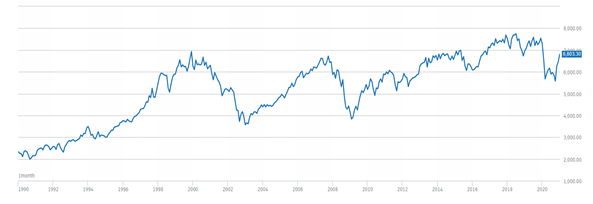

FTSE 100 since 1990:

Source: London Stock Exchange

The thirty-year period from 1990 includes the global financial crisis, the bursting of the dot-com bubble and the war in Iraq and yet the upward trend is still visible.

We’ve seen tough times before. We can use our vast experience to help clients manage their investments, and by reminding them of the lessons of 2020.

3. Tax changes might be on the way to rebalance the books

The coronavirus pandemic cost the UK government around £280 billion last year, according to a review conducted by the Treasury. A Statista report confirms that the furlough scheme alone cost over £46 billion. Balancing the books will be a priority for the government this year and the money may come from taxes.

Chancellor Rishi Sunak called for a review into Capital Gains Tax (CGT) back in June 2020. The Office of Tax Simplification returned with recommendations that could double the number of people paying the tax, providing the government with £70 billion in revenue by 2026.

Aligning CGT with Income Tax rates could see your clients facing a larger CGT liability this year. Speaking to us could help them budget for this change.

Inheritance Tax (IHT) might also be in the spotlight. Early in 2020, the All-Party Parliamentary Group for Inheritance & Intergenerational Fairness (APPG) made several suggestions for IHT changes.

Current rules mean IHT is payable if a gift-giver dies within seven years of making the gift. The rate payable is calculated on a sliding scale with IHT liability removed entirely after year seven. The APPG suggestion to scrap the ‘seven-year rule’ would have consequences for many.

The IHT treatment of unused pension pots could also change this year.

Currently, unused pots on death before age 75 remain outside of an individual’s estate for IHT calculation purposes and 100% can be passed on to a chosen beneficiary. On death after age 75, a beneficiary pays tax on the amount they receive, at their marginal rate.

Although no changes have been confirmed or are due to come into force yet, we can help your clients to mitigate the impact of these changes, should they occur in the future.

Get in touch

At Boolers, we can use our combined experience and expertise to help your clients. Taking into account their financial position as a whole, we can consider the impact of future changes to legislation, allowing your clients to focus on what they value most.

If you have clients who would benefit from financial help to reach their long-term goals, please get in touch with us. Email enquiries@boolers.co.uk or call 0116 2407070.

Please note

The Financial Conduct Authority does not regulate estate planning, tax planning or will writing.