John Allen

Reveal Menu

3 simple ways to avoid getting caught as the Inheritance Tax net widens

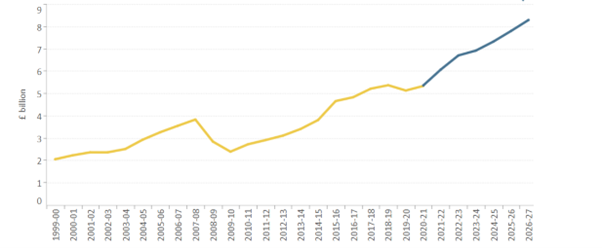

An economic forecast by the Office for Budget Responsibility (OBR) has found that UK families could face a £37 billion Inheritance Tax (IHT) liability over the next five years.

This marks a 36% rise compared to the £27 billion collected between 2017 and 2021.

IHT receipts, 1999 to 2027 (projected):

Source: OBR

The government’s decision to freeze the nil-rate band and the residence nil-rate band (at £325,000 and £175,000, respectively) means that the IHT net is widening.

As the value of your clients’ estates grows, tax-efficient estate planning will become increasingly crucial.

Thankfully, there are ways to reduce a potential IHT liability and Boolers can help your clients to find the right approach for them.

Keep reading for three ways to reduce IHT.

1. Make tax-efficient use of your unused pensions

Before we take a closer look at IHT rates and rules, it’s important to remember that pensions usually fall outside of the estate for IHT calculation purposes. Factoring pensions into estate planning could make a huge difference to your clients.

Unused pension pots on death can be passed on to a chosen beneficiary, tax-free in some cases. This is not the case once a pension is in payment.

Your client must nominate a pension beneficiary. This is done using an “expression of wish” form through your client’s pension provider, rather than via their will.

Once a beneficiary is noted, they could receive:

Efficient pension planning means taking a holistic look at all of your client’s potential income streams in retirement. This is likely to include non-pension wealth like savings, investments, or regular rental income from buy-to-let properties.

Where substantial non-pension wealth exists, it might be possible for your clients to take their pension pots later in retirement, or even as a last resort. This could be incredibly tax-efficient and maximise the amount they can pass on – potentially tax-free – to loved ones.

2. Charitable legacies have several financial and non-financial benefits

The nil-rate and residence nil-rate band are both currently frozen until at least 2026. Over the next four years, as your clients’ houses and investments increase in value, they might become liable for IHT.

The value of an estate that exceeds the IHT threshold is subject to tax at 40%.

One way to decrease a potential IHT liability is to decrease the value of an estate, possibly by giving money away to charity. This has several benefits.

As well as lowering the value of your client’s estate, it also allows them to support a cause they care about. Not only that but donating more than 10% of their estate to charity actually reduces the rate of IHT payable, from 40% down to 38%.

There are three main ways your clients can leave a charitable legacy in their will:

3. Making the most of HMRC gifting rules

Giving while living allows your clients to lower the value of their estate through tax-efficient use of HMRC’s gifting rules.

It also has the benefit that your clients will be able to see the good their money does, passing on a living inheritance earlier in the recipient’s life, possibly at the time when they need it most.

They might consider these gifting exemptions:

Normal expenditure out of income

Your clients might use this exemption to contribute to a child or grandchild’s pension or Junior ISA, for example. Regular gifts can be made tax-free if it can be proven that the gift was made from income, without detrimentally affecting your client’s standard of living.

Annual exemption

Your client can gift £3,000 each year, without tax to pay. What’s more, the limit is per individual and can be carried forward for up to one year.

That means a couple who don’t use any of their annual exemption in this tax year could gift £12,000 in the next.

Small and exempted gifts

Gifts of up to £250 – for birthday or Christmas presents, for example – can be made tax-free.

It is also possible to give tax-free wedding gifts of up to £5,000 as a parent and £2,500 as a grandparent. Non-relatives can gift up to £1,000 to the married couple.

Get in touch

With IHT tax receipts rising, we can help to protect your clients from an avoidable liability. If you have clients who would benefit from long-term financial and estate planning, please get in touch. Email enquiries@boolers.co.uk or call 0116 240 7070.

Please note

The Financial Conduct Authority does not regulate estate planning, tax planning or will writing.