Simon Watts

Reveal Menu

3 useful ways to cut Inheritance Tax and leave more money to your loved ones

The Treasury’s Inheritance Tax (IHT) receipts have hit record highs recently. For 2022/23, the government’s IHT take hit £7.1 billion, increasing by more than a billion from the previous year.

With IHT thresholds frozen – and those freezes recently extended – MoneyAge reports that receipts could grow to £8.4 billion by 2027/28.

The next few years will see more and more families affected by what is often dubbed “the UK’s most hated tax”.

But there are ways to tax-efficiently manage your wealth and estate, helping to lower the liability you leave behind.

Here are just three of them. But first, a closer look at why receipts are rising.

The nil-rate band has remained unchanged since 2009

The nil-rate band is the threshold above which IHT usually becomes payable. It is £325,000 for the 2023/24 tax year. Since April 2017, estates have also benefited from a residence nil-rate band of £175,000. This applies when you pass on your main residence.

Your unused allowance on death can also be transferred to your surviving spouse, possibly giving them a £1 million IHT threshold.

The value of your estate that exceeds the threshold is usually taxed at 40%.

Back in his 2021 spring Budget, chancellor Rishi Sunak froze the nil-rate and the residence nil-rate band until 2026. Sunak’s not-quite-successor, Jeremy Hunt, used his 2022 autumn statement to extend those freezes until 2028.

While the residence nil-rate band was introduced in 2017 at £100,000, it slowly increased to £175,000 and has remained at that level since 2020. The nil-rate band, though, hasn’t changed since 2009 – a long 14 years.

3 simple ways to minimise the IHT liability you leave behind

1. “Giving while living” using gifts and HMRC gifting exemptions

While you might be planning to give most of your wealth away on death, “giving while living” has several benefits.

Not only will you be around to see the difference your money makes, but you’ll also be lowering the value of your estate, and so the IHT liability you leave behind.

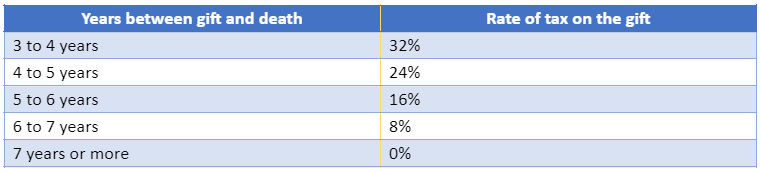

You can gift as much as you like during your lifetime, although the gifts will only be free from IHT if you survive for seven more years after the date the gift is given. For this reason, gifts made during your lifetime are known as “potentially exempt transfers (PETs)”.

On death within the first two years after a gift is made, tax is payable at 40%. On death between three and seven years later, a taper applies:

Some HMRC exemptions, though, allow you to make gifts that are immediately IHT-free. These include:

2. Placing assets in a trust, taking them outside of your estate for IHT purposes

Using gifts can reduce the value of your estate now, lowering a potential future liability while giving yourself the best chance of beating the “7-year rule”. But what if you want to retain some control over the money you gift?

A trust allows you to set assets aside for your chosen beneficiaries until a future date. In the meantime, those assets are looked after by a trustee.

A trust can be especially useful if you want to leave money to grandchildren who are not yet able to look after the money themselves.

There are two main types of trust:

It’s important that you fully understand the rules and implications of the trust you choose, so be sure to contact us before you decide.

3. Spending and enjoying your money now to lower your liability

It’s worth remembering that the simplest way to lower the value of your estate is to spend your money. Your wealth was hard-earned and using it to enjoy your retirement is a completely valid option.

Ticking items off your bucket list, enjoying experiences, and making memories with loved ones could be a great way to lower your potential IHT liability, and could even mean there’ll be no IHT to pay.

You might find that a combination of gifting, trusts, and personal spending is the perfect mix.

Get in touch

At Boolers, we can help you to manage your wealth and estate planning tax-efficiently, ensuring that your wishes are carried out, while your loved ones’ IHT liability is as low as possible.

If you would like to discuss your estate planning, please contact us today.

Please note

The Financial Conduct Authority does not regulate estate planning, tax planning or will writing.

Remember that taper relief only applies to gifts in excess of the nil-rate band. It follows that, if no tax is payable on the transfer because it does not exceed the nil-rate band (after cumulation), there can be no relief. Taper relief does not reduce the value transferred; it reduces the tax payable as a consequence of that transfer.