Chris Ball

Reveal Menu

6 valuable benefits of giving while living

Recent figures published by MoneyAge suggest that more than 30% of investors with adult children plan to pass on a living inheritance this year.

While more than half (57%) indicated that they would gift between £1,000 and £10,000, a fifth of responders confirmed they would be gifting £50,000 or more. In total, this could equate to more than £12 billion of transferred wealth in 2022.

Giving while living has received increased publicity in recent years, not least thanks to the Giving Pledge, co-founded by US billionaires Warren Buffett, and Melinda and Bill Gates.

You don’t need to be a billionaire, however, to enjoy the benefits of giving while living, rather than opting for the traditional route of distributing your assets only on death. The benefits can be non-financial, as well as financial.

Here are six reasons why you might consider choosing a living inheritance.

The non-financial benefits of giving while living

1. See the joy your money brings while creating lifelong memories

The obvious issue with distributing your wealth on death is that you won’t be around to see the effect your generosity has on the lives of your beneficiaries. Giving while living can change that.

Not only will you be able to witness the joy your money brings to your loved ones, but you’ll be creating lifelong memories for yourself too.

Helping a child to pay for a once-in-a-lifetime holiday, supporting a grandchild through further education, or providing a deposit on a first home is something that your whole family will benefit from.

2. Passing money on earlier, when it is needed most

It might not be the gift itself that is important, so much as the timing of it. If you wait to provide an inheritance on death, your children could be approaching retirement themselves and your grandchildren might already have families of their own.

Providing cash gifts when your children are just starting out in life could make all the difference to their ability to buy their dream home or start a family at the perfect time for them.

3. Being there to shape how your money is used

While trusts can be a good way to add stipulations to the money you leave behind, being there to shape how the money is used first-hand will give you even greater control and could prove even more rewarding.

If you want to provide a house deposit for a child or pay off the student loan of a grandchild, you can. You’ll be sure that your money is going exactly where you want it to go – and where you deem it to be most needed.

There are plenty of financial benefits too

4. The chance to reduce the value of your estate

With Inheritance Tax (IHT) thresholds frozen until at least 2026, FTAdviser confirms that the Treasury could receive an additional £985 million in death duty over the five years of the freeze.

The nil-rate band is frozen at £325,000, while the residence nil-rate band (which comes into effect if you pass your family home onto the next generation) is frozen at £175,000.

If you are worried that the value of your estate could exceed these thresholds, giving gifts during your lifetime could be a very tax-efficient way to pass on your wealth, reducing the value of your estate and the tax liability you leave behind on death.

5. HMRC rules allow you to make tax-free gifts

You can lower the value of your estate by taking advantage of HMRC’s annual exemption. This allows you to give away £3,000 each tax year.

The exemption can be carried forward for one year and applies separately to couples. That means you and your partner could potentially gift £12,000 during a single tax year if neither of you used your exemption in the previous year.

You can also make regular gifts using the normal expenditure out of income exemption. This allows you to contribute to a child’s Junior ISA or pension, for example, during your lifetime. You’ll need to ensure that the gift comes from income and doesn’t detrimentally affect your standard of living – and that you can prove this to HMRC.

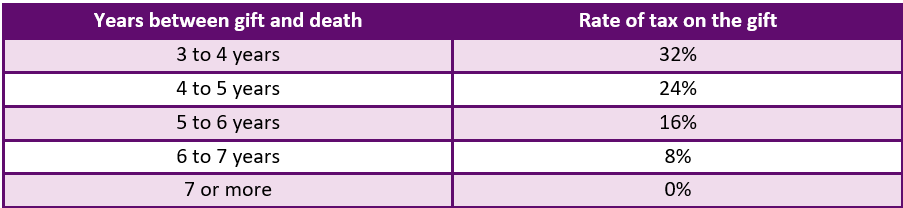

6. You’ll have a greater chance of living for 7 years after making the gift

You can make as many gifts as you like during your lifetime, outside of HMRC’s exemptions. These are known as “potentially exempt transfers” (PETs) as the gifts will only become liable for tax if you die within seven years of making the gift.

Gifts you make in the three years before your death are taxed at 40%. If you die within three to seven years of making the gift, the rate of IHT payable is measured on a sliding scale known as “taper relief”, as follows:

The earlier in life you begin making gifts, the greater the likelihood that you’ll survive beyond seven years, rendering any gifts you make tax-free.

Remember that taper relief only applies to gifts that exceed the nil-rate band. Taper relief does not reduce the value transferred; it reduces the tax payable as a consequence of that transfer.

Get in touch

Boolers can help you with all aspects of your estate planning, including helping you to decide on the most tax-efficient ways to give a living inheritance. If you would like to discuss leaving your wealth to the next generation, or any aspect of your long-term plans, please contact us today.

Please note

The Financial Conduct Authority does not regulate estate planning, tax planning or will writing.