Duncan Pickering

Reveal Menu

Coronavirus and pensions – what does the pandemic mean for a client’s retirement plans?

In recent months, clients are likely to have seen news headlines concerning the economic impact of the coronavirus pandemic. March saw both the FTSE and Dow Jones experience their biggest one-day falls since the late 1980s and, between 1 January and 11 May 2020, the MSCI World Index fell by around 12.5%.

One of the questions that clients are likely to have is: what impact does the recent stock market turmoil have on my retirement plans?

Are clients still going to be able to retire when they want? Will they still have enough in retirement? And what should they do in response to the recent volatility?

As the current Moneyfacts Retirement Planner of the Year, we can help your clients to answer some of these questions.

Firstly, here’s what hasn’t changed

Despite the recent stock market volatility, it’s possible that not all of your client’s retirement income provision may have been significantly affected:

A quick point concerning diversification

When clients look at the performance of stock markets, it’s also important to remember that falls in the value of the Dow Jones or FTSE 100 are typically not mirrored in the value of their portfolio.

Our clients typically have diverse portfolios that include exposure to other asset classes, for precisely this type of situation.

In addition, if a client is approaching retirement and they have a Defined Contribution (DC) or investment-based pension, it’s possible that their investments have already been ‘lifestyled’.

In the years immediately before retirement, funds are often de-risked into bonds and cash in order to protect individuals from heavy stock market losses just before they retire.

The impact of coronavirus on pensions

As of 15th May 2020, the MSCI World Index – a weighted global stock index featuring 1,643 constituents across 23 developed markets, including the UK, US, Germany and Japan – had fallen by around 15% since 1st January.

During the worst point of the pandemic, global shares had fallen by around 30%. However, many markets have begun to recover since mid-March as plans to exit lockdown begin to take shape.

One of the biggest mistakes that clients can make right now is to sell investments that have fallen in value (unless some new and relevant information emerges about a particular share or fund). Selling now could result in clients being out of the market when the recovery starts to happen.

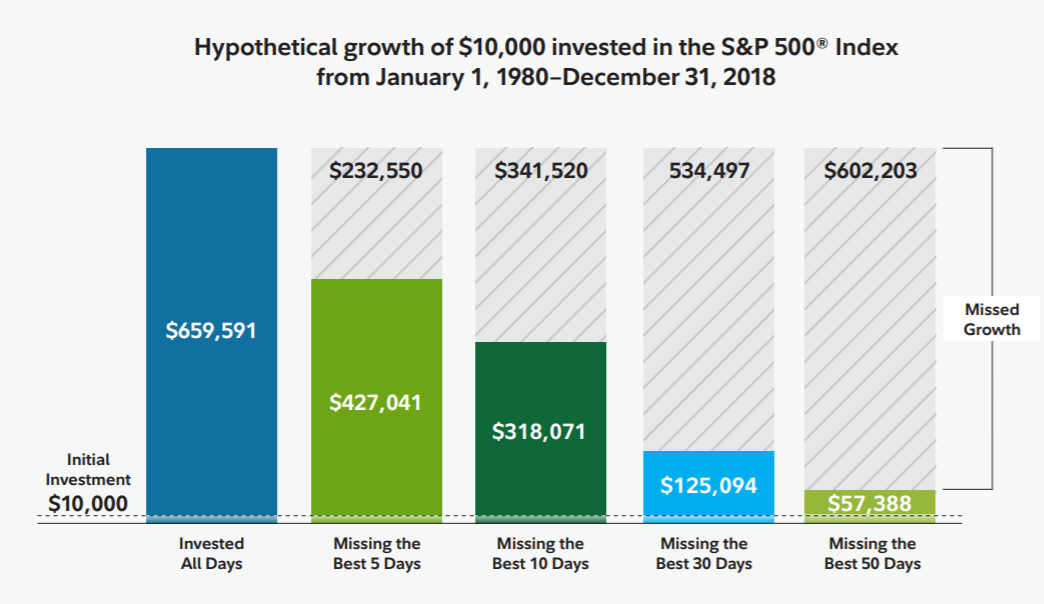

The chart below shows that spending time out of the markets can have a significant effect on a client’s long-term returns.

Source: Fidelity

If a client had missed just the five best investment days in the US between the start of 1980 and the end of 2018, they would have sacrificed $232,550 in returns. That is around £187,000 in lost growth for being out of the market for just five days.

If a client had been out of the market for the best 30 days, they would have missed growth of around £430,000.

Losses can be painful. However, history shows us that, if we are patient, markets tend to recover.

Here’s the annualised returns of the MSCI World Index over one, three, five and ten years, and since its launch at the end of 1987.

Source: MSCI

Over the last ten years, the index shows an annualised return of 9.36%. Between 31 December 1987 and 31 December 2019, the annualised return of global equities was 7.72%.

Annuity rates and dividends also fall

For clients who are already retired, or who are planning to retire in the near future, cuts to both dividends and annuity rates could result in a fall in their anticipated income.

Steven Cameron, Aegon pensions director, says: “The current market turbulence will no doubt be concerning for individuals whose pension savings are invested partly or fully in the stock market.

“If you’re about to retire and were planning to buy an annuity, you face an additional challenge as the 0.5% cut in bank base rates has meant annuity rates have also fallen.”

HL head of investment analysis, Emma Wall, says: “In recent weeks, dozens of companies have announced that dividends and share buybacks will be scrapped, suspended or delayed.

“This could put pressure on investors who rely on the natural income from stock dividends – particularly those in retirement. It’s still too soon to say with certainty whether the recent increase in values is the beginning of the end, or simply an upswing typical of volatile markets before we drop again.”

Clients could consider delaying taking their pension

If clients have many years until retirement, then there is no real reason for them to panic despite the current volatility. As we have seen, investment markets tend to offer positive returns over time, despite blips.

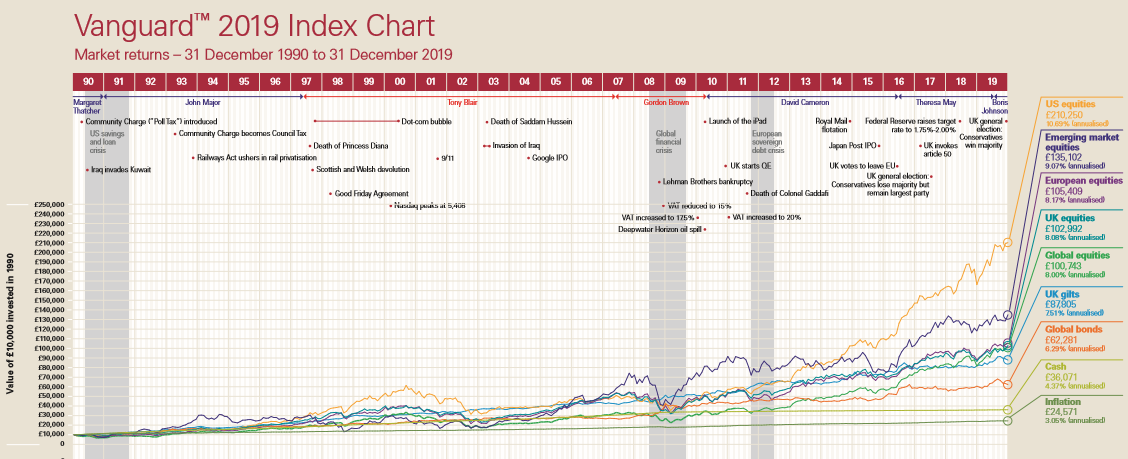

The chart below shows what £10,000 invested in 1990 in a range of investments, including UK equities, US equities and shares in ‘emerging markets’, was worth at the end of 2019.

Despite many volatile periods – the dot.com bubble, the global financial crisis, the Brexit vote – £10,000 invested in UK equities in 1990 was worth £102,992 on 31 December 2019, equivalent to an 8.08% annualised return.

Compare this to cash, where £10,000 invested in 1990 grew to £36,071 during the same period – a 4.37% annualised return.

Notes: Cash = ICE LIBOR – GBP 3 month; global equities = the MSCI World Index; US equities = S&P 500; UK equities = FTSE All-Share; inflation = Retail Price Index, (Jan 1987=100); global bonds = Bloomberg Barclays Global Aggregate; European equities = MSCI Europe; UK gilts = ICE BofA; UK gilt (local total return) emerging market equities = MSCI emerging markets; all shown gross of taxes and of fees and in GBP.

Source: Bloomberg and Factset and Bank of England, as at 31 December 2019

Being patient and waiting for markets to recover in the long term is one way that clients can ensure their retirement plans aren’t blown off course.

Another thing clients could consider is to defer taking their pension, particularly if they don’t need the income from it immediately.

If a client is in a Defined Contribution scheme, delaying when they take their benefits means that they leave it invested for longer, so they could have a bigger pension pot when they come to retire.

Deferring also means that clients can continue to save as much as £40,000 a year into a pension and earn tax relief under current rules.

Clients could also consider deferring their State Pension. For clients who have not yet reached State Pension age, their State Pension will increase every week they defer, as long as the deferral is for at least nine weeks.

A client’s State Pension increases by the equivalent of 1% for every nine weeks you defer. This works out as just under 5.8% for every 52 weeks.

Steven Cameron from Aegon also notes: “If you’re already using drawdown, or plan to move into drawdown soon, you might also want to avoid taking out any more than you need to while fund values remain depressed. The more you can leave invested, the more you will benefit if stock markets recover.”

Speak to a financial planner for advice

If you have clients who are worried about their retirement income – perhaps they don’t have many years left until they retire – then speaking to a financial planner can help.

Steven Cameron from Aegon concludes: “Those with an adviser should contact them as the first point of call. There is a risk that taking ‘panic’ action might not be in someone’s best longer-term interests.”

If you have any clients that would benefit from advice, please get in touch with us. Email enquiries@boolers.co.uk or call 0116 2407070.