Richard Borrington

Reveal Menu

5 things your clients need to consider when accessing their pension at 55

Since the introduction of Pension Freedoms in April 2015, retirees have been able to access the whole of their pension fund in one go, from age 55.

According to HMRC, the value of flexible withdrawals since that date now exceeds £37 billion. Of that amount, retirees aged over 55 accessed £7 billion. The Financial Conduct Authority (FCA) also confirms that during 2019, more than half of those accessing pension pots for the first time withdrew them completely.

It can be very tempting for clients to take pension benefits as soon as the chance arises. The coronavirus pandemic and its effect on stock markets have also led to panic.

The consequences of taking pension benefits too soon can be far-reaching though. Here are five things your clients will need to consider when taking their pension at 55.

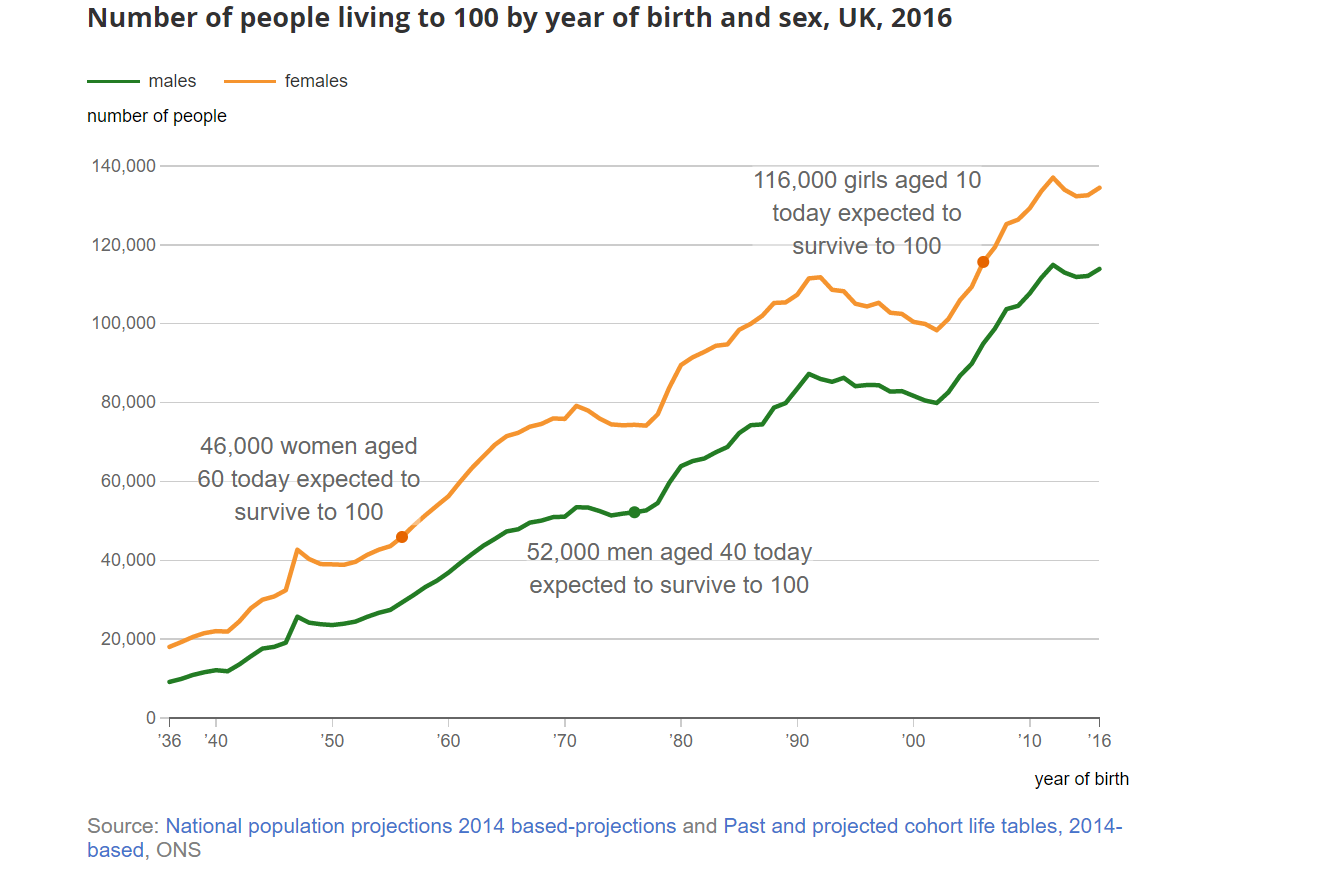

1. Life expectancies are rising

Figures from the Office for National Statistics (ONS) confirm that the current average life expectancy for women at birth exceeds 83 years. For men, the figure is close to 80.

That means a client retiring at 55 today, might need their retirement fund to last for the best part of a quarter of a century. Not only that, but the ONS also looks at the rising numbers of people who will reach 100.

The report concludes that of women aged 60, 46,000 could become centenarians – that’s a 12.3% chance of turning 100. If your client is a 40-year-old male, their chance of turning 100 is 13.3%.

Source: ONS

Some clients choosing to retire at age 55 might need to budget – by making sustainable withdrawals or balancing a lump sum with other revenue – for a period of 45 years.

2. Fitting pension income into a wider financial plan

Your clients will have several pension options to choose from at retirement. These are:

It is important that your clients understand how a pension withdrawal fits into their wider financial plan. We can help them with this.

An annuity, for example, supplies a regular income. This might be perfect for someone with fixed, known expenses, who has other investments or a secondary income to cover discretionary expenditure.

Your client can use Flexi-Access Drawdown to supply a regular income, but it can include tax-free lump sum withdrawals too, up to a maximum of 25% of your client’s pension pot. This flexibility is great for covering one-off, irregular expenditure such as holidays.

But budgeting withdrawals over an extended period – especially factoring in short-term volatility such as we’ve seen recently – can be difficult.

Considering a client’s other sources of income, their desired standard of living and their plans for the future can help us to decide the best way for them to access their pension, and when.

3. The pros and cons of accessing a lump sum

Taking a whole pension pot in one go will free up a huge amount of capital. Your client’s retirement plans might include world travel, house renovation, or helping children onto the property.

Equally, a lump sum can be a great way to reduce the debt a client takes into retirement. Using the money to pay off a mortgage means that all your client’s retirement income can go on maintaining their desired lifestyle.

Weighing up the desire to reduce debt now or leave pension funds invested with the potential for future growth, isn’t easy. Professional financial advice can help.

4. The Money Purchase Annual Allowance (MPAA)

Your client might trigger the MPAA when they access their pension benefits using certain Pension Freedom – or ‘flexible’ – options.

The Pensions Annual Allowance is the amount that the client can pay into a pension in a tax year and still get the benefit of tax relief. When your client withdraws taxable funds from a Defined Contribution (DC) pension as part of a lump sum, or as taxable income from Drawdown – they will trigger the MPAA.

For the 2020/21 tax year, this lowers the Annual Allowance from £40,000 to £4,000. This drastically decreases the amount your client can contribute to other pensions they hold while benefiting from tax relief.

Taking retirement benefits at age 55 means missing out on years of tax-efficient pension savings.

5. The value of advice

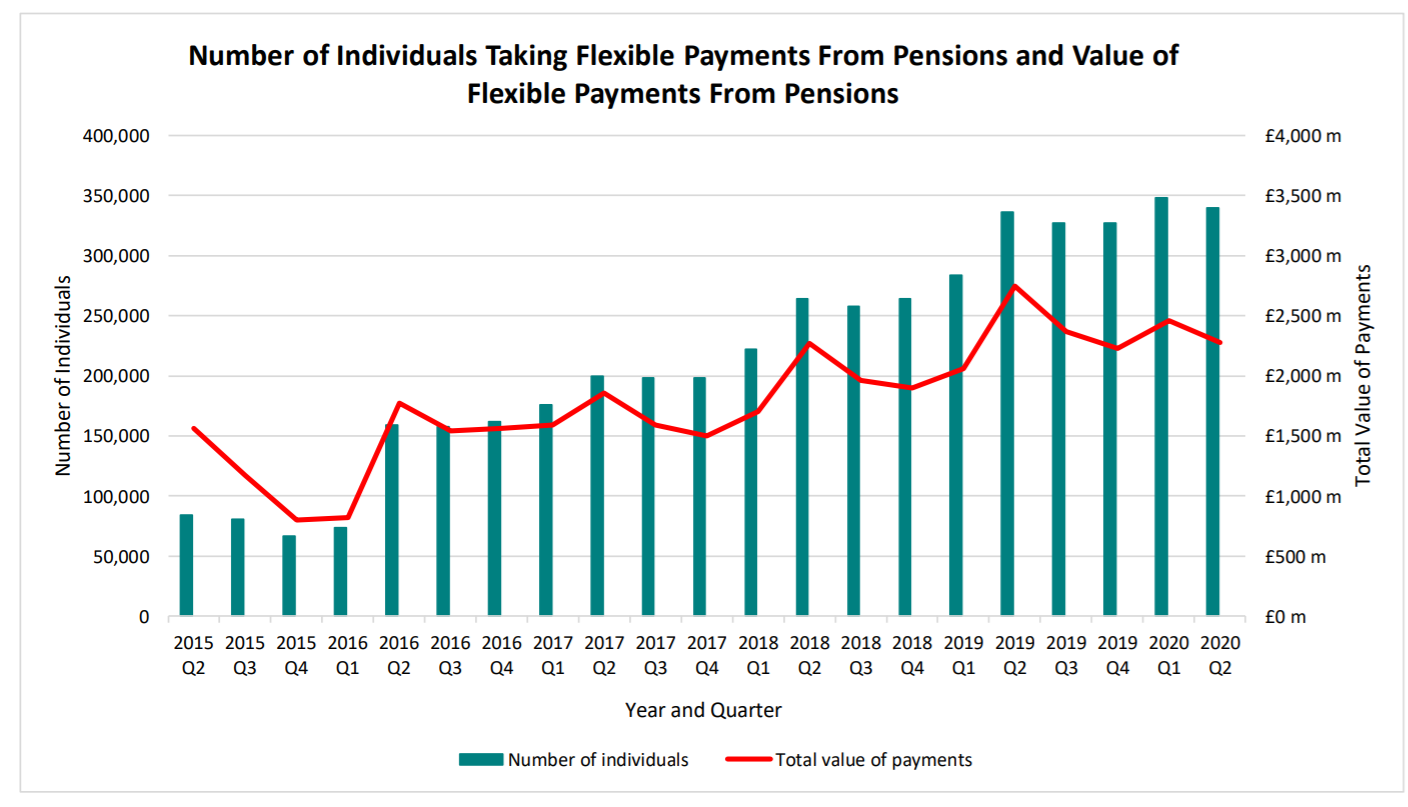

Pension Freedoms give retirees choice and flexibility, but a level of responsibility too. Since the government introduced flexibility, the number of people taking advantage of these new options has been steadily rising.

In 2015, around 60,000 to 70,000 individuals withdrew flexible pension benefits each quarter. By 2019, that amount had risen to around 300,000 per quarter.

The number of people requiring advice is increasing too.

Source: HMRC

Your client’s retirement pot is designed to last them for the rest of their life.

Not only that, but it needs to maintain their desired standard of living, cover unexpected future costs such as later life care, and potentially leave enough to pass some onto the next generation.

Accessing pension funds early isn’t necessarily the wrong thing to do. But as with all financial matters, it is dependent on a client’s personal circumstances.

By sitting down with your client and discussing their long-term goals and aspirations, and understanding their financial situation, we can help your client make the choice that is right for them.

Get in touch

If you have any clients that are considering taking their pension at age 55 and who could benefit from advice, please get in touch with us. Email enquiries@boolers.co.uk or call 0116 2407070.

Please note

A pension is a long-term investment. The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. The interest rates at the time you take your benefits could also affect your pension income.