Gavin O’Neill

Reveal Menu

The rise of “all-or-nothing” retirement

Covid-19 has had a polarising economic effect in the UK. Among the 72% of households that were able to save money due to reduced lockdown spending, it has created six million “accidental savers”. For others, furloughed or made redundant, the pandemic has meant a struggle to make ends meet.

Now, a Hargreaves Lansdown survey, as quoted in the FTAdviser, confirms that the pandemic has widened the gap in retirement planning too.

While coronavirus has helped people form concrete ideas about their retirement, those approaching pension age have widely contrasting opinions on what their best option looks like.

The report points to a rise in the number of people wanting to retire earlier than planned, as well as a rise in those deciding to keep working for longer.

What is the right choice for you and how can financial planning help you decide? Keep reading to find out.

Number of retirees wanting to retire before the State Pension Age doubles compared to before the pandemic

The new research from Hargreaves Lansdown has found that those wanting to retire between age 50 and State Pension Age has more than doubled, rising from 4% before the pandemic to 10% after.

The increase in those wishing to retire now has been even more pronounced among women. The number of women that want to stop work altogether has tripled, rising from 4% to 12%.

Reasons behind this choice vary wildly, but, for many, the decision to retire will have been forced upon them.

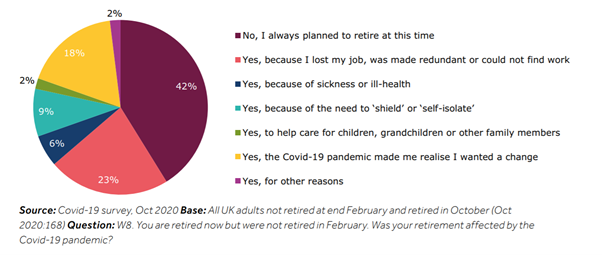

Source: FCA Financial Lives 2020 survey

The FCA Financial Lives 2020 survey found that almost three in five (58%) of those who retired between March and October 2020 did so because of Covid-19.

Of those, 23% retired because they lost their job, were made redundant, or could not find work. A further 9% retired because of the need to shield or self-isolate.

Even for those not forced into the decision, Covid played a part. 18% confirmed that the pandemic had made them realise they wanted a change.

If you have opted to retire earlier than originally planned, it might be because you welcomed the time at home with loved ones. It might have made clear the compromises work was forcing you to make. Or maybe the “accidental savings” you accrued during lockdown gave you the buffer you needed.

There are pros and cons to retiring early

Pros

The benefits of retiring early might include improved health. This could allow you to do the things you’ve always dreamed of, such as world travel.

You might be able to spend more time with your children or grandchildren or change your career. AgeUK confirms that the number of self-employed people aged 65 and over has more than doubled in the past five years.

Cons

You will need to know exactly where your income is coming from, and how much is left.

Back in February, we looked at four reasons why you might opt to take your pension as a last resort and it is worth bearing these in mind.

Taking a considerable sum to cover immediate luxuries could push you into a higher tax bracket; you could get emergency taxed too. If you access your fund using Pension Freedoms you could trigger the Money Purchase Annual Allowance (MPAA), reducing future contributions.

With life expectancy at almost 80 years for males and over 83 for females, you might have to budget for thirty or even forty years.

There are tax benefits to not taking your pension at all. You can pass 100% of your unused pension funds on to the next generation tax-free, in certain circumstances. Leaving a pension untouched can be a tax-efficient way to pass on wealth.

Numbers wanting to remain in full-time employment have risen by 4%

The numbers of those who want to continue working full-time increased from 38% to 42%.

Some will have made that choice through financial necessity. While the pandemic has created six million accidental savers, only 5% have put that money into a pension. Others, who were furloughed or made redundant, might have stopped pension contributions entirely.

Money Marketing reported last year that 25% of us reduced our pension contributions during the pandemic and that will have long-term repercussions on the size of retirement pots.

If you have decided to continue working for longer, the loneliness of lockdown and the social aspect of your career might have played a part.

Pros and cons

Pros

An obvious reason to leave your pension intact for longer is that you will make more contributions and benefit from the effects of compound growth.

After a lengthy career, you will have built up considerable knowledge in your field. Working for longer might allow you to move into a consultancy role, giving you a perfect opportunity to decrease your hours gradually.

You might use a small pension or income from elsewhere – such as from buy-to-let properties – to supplement this phased retirement.

Cons

One downside to working for longer will be time spent away from your family. You’ll need to weigh up the financial necessity and social benefits against the things you could be doing once you retire.

Get in touch

After contributing to a pension throughout your career, making important retirement decisions can be hard. There is no “right” answer, and whether you are contemplating retiring earlier or later than planned, the decision is yours.

But Boolers are here to help. If you are worried about the long-term implications of your retirement decisions or would like to discuss your plans in more detail, please contact us today.

Please note

The minimum retirement age is currently 55, rising to 57 in 2028.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.