Chris Ward

Reveal Menu

Divorce and the pension wealth gap: How advice can help your clients get their fair share

The Independent reported recently that divorce enquiries increased by 95% at the start of 2021, compared to the same period in 2020.

The enforced proximity caused by coronavirus lockdowns was said to be the main contributing factor, with women making the majority of new queries.

Yet a recent report from the University of Manchester has highlighted the gender wealth gap on divorce, showing a huge disparity between men and women’s wealth, before and after a divorce. This is a result of many factors, including a gap in average earnings and differences in life expectancy.

Divorce is a stressful time, but clients with an adviser who fully understands their financial position have a much better chance of receiving their fair share, whichever side of the divorce they are on.

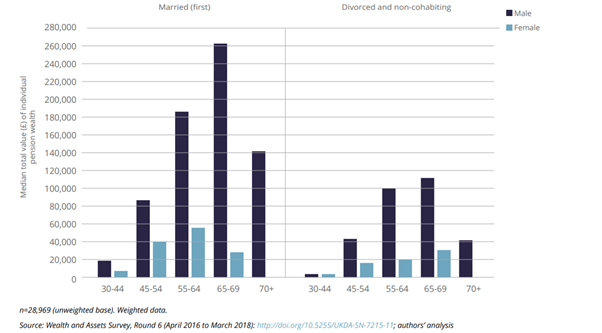

The pension wealth gap could leave your female clients £180,000 worse off in retirement… even before a divorce

Research from the Centre for Economics and Business Research (CEBR) suggests that the gender pension gap has widened to more than £180,000 for those over 55.

While men can expect to retire with around £20,700 a year, the figure for women is less than £15,000. This is despite women contributing a higher percentage of their earnings, a disparity caused by their lower average salaries.

The University of Manchester research goes on to highlight how this difference affects men and women at different ages, while married and following a divorce.

Source: The University of Manchester

Notes: n=28,969 (unweighted base). Weighted data. Source: Wealth and Assets Survey, Round 6 (April 2016 to March 2018): UK Data Service; authors’ analysis

Financial advice can help your clients get their fair share

While clients might approach their adviser for help with investing the proceeds of a divorce, our job can – and ideally should – start much earlier.

Our involvement from the beginning of the process allows us to help your clients achieve the best possible outcomes, ensuring the solution is right for their needs, both now and in the future.

Because we take the time to get to know all of our clients, we are well placed to take their entire financial position into account, giving back a sense of confidence and control at a stressful time.

Assets in divorce can be unevenly distributed and this is especially true for pension assets. Our experience can help to ensure your clients get their fair share of any pension entitlement however the pension provision is split.

Pensions can be split in different ways on divorce

A pension sharing order

Where a pension sharing order is put in place, pension assets are divided by an exact percentage worked out by the courts.

If your client is the party receiving additional pension funds, they can opt to keep them in the same scheme as their former partner or transfer the fund to a new scheme. In both cases, the funds will be held under your client’s name from that point.

A pension offsetting order

Offsetting attempts to even up disproportionate pension provision by giving a higher value of non-pension assets to the party with the smallest pension fund.

If your client undertook a “home building” rather than “bread-winning” role in the marriage, for example, they might be entitled to a greater share of a jointly held property, thereby offsetting the pension they missed out on through being unable to work.

A pension earmarking order

An earmarking order apportions a percentage of the pension assets to the other party, but they can only be accessed once the pension is taken. This ties both parties together financially until at least pension age.

We can help calculate a fair valuation for your clients’ pensions

While defined contribution (DC) plans have a value based on the number of contributions received, defined benefit (DB) plans can be harder to value.

We can calculate the cash equivalent transfer value (CETV) of all your clients’ plans, providing a clear understanding of the pension provision your client holds currently. This will help them to make long-term financial plans based on the likely outcome of the divorce, though it is worth noting too that a CETV figure isn’t fixed.

Get in touch

Whether your clients are looking to invest an additional pension amount or need to change their plans having parted with some of their retirement provision, long-term financial planning can help your clients make the most of whatever pension wealth they have.

A divorce is a stressful and worrying time but knowing that expert advice is on hand can benefit your client, emotionally and financially, providing peace of mind as well as the best possible financial outcomes.

If you have clients who would benefit from divorce advice, please get in touch. Email enquiries@boolers.co.uk or call 0116 240 7070.

Please note

This article is for information only. Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.