Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin July 2024

Markets were mixed over the month, as slower inflation and weaker labour market data in the US increased expectations of rate cuts, which helped boost a rotation into small cap stocks and other long-duration assets. The performances of the main equity indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

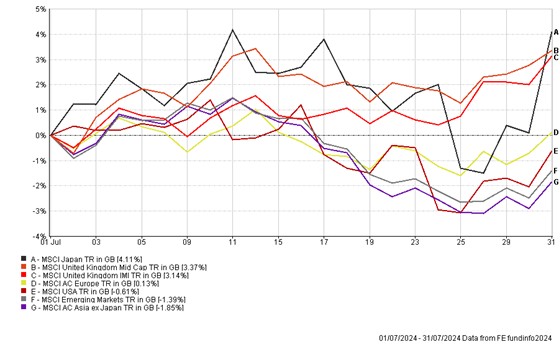

Not So Mag 7?

In the US, earnings season continued with four of the ‘magnificent seven’ reporting results for the previous quarter. Overall, investors were left slightly disappointed by the releases from Tesla, Alphabet, Microsoft and Meta, due to heightened expectations by investors that investments in Artificial Intelligence could result in feasible revenue growth at this point in the earnings cycle.

This resulted in an initial sell-off in the tech sector before a rebound towards the end of the month. The MSCI USA index fell slightly by -0.61% over the month, with most S&P companies having beaten analysts’ expectations, which suggests the resilient US economy is contributing to a broadening of earnings.

In July, we saw a catch-up trade from the laggards such as small-cap equity stocks, which are more sensitive to interest rate cuts. This was shown by the largest one-month outperformance of the Russell 2000 (small cap index) versus the Nasdaq 100 (large cap tech index) in over 20 years.

The Resurrection of the Japanese Yen

The Japanese Yen increased by 6.5% vs the US dollar, the strongest monthly move since 2016 due to market expectations of early Federal Reserve (Fed) interest rate cuts and the Bank of Japan raising rates to 0.25%. The effect of this policy divergence is the unwinding of the carry trade where investors borrow/short the Yen to gain higher yield in other dollar denominated assets. As a result, Japanese stocks initially fell on this news before bouncing back as hedge funds doubled down on their short- positions on the Yen. This move helped oversold large cap stocks, which are major exporters, to recover, as they benefit from a weaker Yen.

Bonds Hold Steady

June’s positive CPI figure and a weakening labour market have increased investor expectations for Fed rate cuts for the rest of the year. This optimism boosted US Treasuries, which gained 2.2% over the month in local currency terms. As a result, the front end of the curve rallied causing the yield curve to re-steepen, with the spread between the 10-year and 2-year US Treasury yield narrowing to its lowest level since January 2024.

In the UK, GDP growth in the second quarter came in stronger than expected, combined with sticky services inflation, suggesting that interest rate cuts will be slow and steady compared to the US and Europe. UK Gilts returned 1.9% over the month in sterling terms.

In the Eurozone, government bonds in periphery countries such as Spain and Italy continued to outperform bonds in core countries such as Germany and France. As investors seek higher yields in anticipation of further European Central Bank interest rate cuts, with Italy outperforming all other major government bond markets year to date.

THE BOOLERS INVESTMENT COMMITTEE