John Allen

Reveal Menu

How expert advice can help your clients plan for later-life care fees

The Centre for Ageing Better confirms that the older population in England is getting larger. During the last four decades, the number of over-50s has increased by 47% (or around 6.8 million people). The number of people aged 65 has also increased by 52% (or 3.5 million people) during the same period.

Despite recent Covid-related downturns, UK life expectancy is generally rising, but so is the number of years we can expect to live in ill health. That makes factoring in later-life care a crucial part of any long-term financial plan.

From thinking about care costs early to including a contingency if care isn’t needed, professional financial advice can help ensure your clients are prepared and can afford the care they need.

Here’s how.

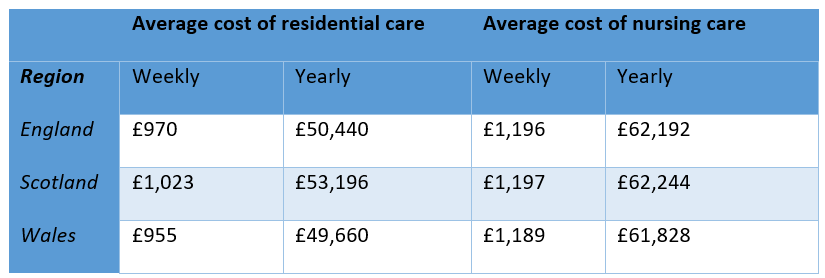

Care costs vary widely, so there’s a lot to think about

The latest figures from February 2024, published by The Telegraph, confirm that:

There are, though, regional differences.

Source: The Telegraph

As you can see, care is generally most expensive in Scotland and cheapest in Wales. Regions within those countries will have their disparities too, though.

In England, for example, a self-funded bed in a care home in the north-east in June 2024 would cost £1,035 a week. In London, though, this cost rises to £1,383.

Your clients will also need to factor in the type of care they might need. Receiving care at home for a set number of hours is cheaper, say, than live-in care, in which a carer moves in full-time.

Finally, it’s worth noting that dementia care can be particularly expensive due to the complexity of the care required. The Alzheimer’s Society says that an individual with dementia spends an average of around £100,000 on their care over their lifetime.

Financial advice could help your clients start planning for these care costs now

Factoring care costs into a client’s long-term plans from the outset

A client’s retirement spending is unlikely to be consistent. At the start of retirement, most retirees spend more as they tend to enjoy an active lifestyle – spending on travel, eating out, and other types of discretionary expenses. Then, as they age, retirees tend to slow down and spend less.

Finally, as discretionary expenses begin to decrease, health costs tend to rise.

The cost of any later-life care is difficult to predict because no one knows exactly what care they may need. Additionally, the price of care could also change in the coming years.

This is where working with a financial planner can be beneficial. We can use cashflow modelling to map out what assets a client has and “rehearse” various scenarios considering the costs of different levels of care. This gives a client some indication of what the effects of paying for later-life care could be on their wealth, so they can be prepared.

By understanding a client’s spending patterns and the potential costs associated with long-term care, we can give them the confidence that they have “enough” for whatever costs they might incur in their retirement.

Considering an immediate care plan

If your client is already receiving care or is about to move into a care home, they may be concerned about how they will meet the costs of this care.

An “immediate care plan” (sometimes called an “immediate needs annuity”) provides a guaranteed monthly payment for life to help pay for an individual’s care fees.

In exchange for a single premium, an immediate care plan pays a monthly payment to the individual’s UK-registered care provider for the rest of their life. Many such plans are also index-linked and will rise in line with the cost of living.

A financial planner can help by comparing the various immediate care plans in the market and finding an appropriate solution.

Managing wealth tax-efficiently

Planning for later-life care is a fine balancing act. If a client doesn’t save enough, they risk not having sufficient assets to meet the cost of care when they need it. Save too much, and if they never need care, their loved ones may have an Inheritance Tax issue when they pass away.

Financial planning can help your clients to build their wealth tax-efficiently. For example, retaining money in pensions (that typically sit outside an individual’s estate) can be an effective way to pass on wealth while drawing care costs from cash or other savings.

LPAs to help ensure your financial affairs are looked after

A Lasting Power of Attorney (LPA) lets your client nominate a trusted person (or people) to manage their affairs when they are no longer able.

Putting this valuable document in place ensures that a client can specify their wishes ahead of time and reassure them that someone they trust will carry out these wishes for them.

Remember that a client can’t make an LPA when they have lost mental capacity, so it’s generally better to set this up sooner rather than later.

Get in touch

At Boolers, we’re a Chartered firm of professional financial planners with decades of combined knowledge and experience. If you have clients who would benefit from speaking to our expert team, email enquiries@boolers.co.uk or call 0116 240 7070 now.

Please note

This article is for information only. Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate estate planning, cashflow planning, tax planning, Lasting Powers of Attorney, or will writing.