Prabhdeep Gill

Reveal Menu

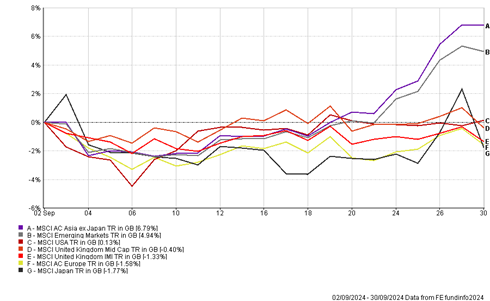

Market Commentary: Monthly Bulletin September 2024

Markets were mixed over the month, as China Stimulus measures helped boost Asia and Emerging market stocks. Meanwhile, in the US we saw a surprising 50 basis point rate cut from the Federal Reserve which signaled to markets that the economy could be slowing.

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

CHINA!

Chinese equities outperformed over the month, President Xi Jinping announced monetary and fiscal stimulus measures to help support sluggish economic growth. The Chinese economy has been in the doldrums due to a struggling real estate sector, which has led to weak consumer demand for goods and services. As a result, over the past three and half years, the Chinese stockmarket has suffered large falls in foreign investment.

The fiscal package consists of a $100bn incentive to encourage investors and companies to buy shares, where the People’s Bank of China (PBOC) introduced a lending pool to the country’s capital markets for companies to buy back their own shares. In addition, the PBOC cut interest rates initially to 2.0% and it is expected further rate cuts are expected to other lending instruments to help stimulate the property sector.

Although the stimulus measures are a positive step for the Chinese economy, it remains to be seen as to whether they are enough to change the long-term outlook for China, as they do not address the underlying structural issues of weak consumer demand. Chinese consumers still have a lot of wealth in the property sector, and animal spirits in the economy may require further stimulus to return to pre-pandemic levels. Nevertheless, Chinese equities represent great value with institutional investors looking for quality businesses that have major growth opportunities, regardless of how the Chinese economy is projected to perform in the short term.

The Fed Goes 50

In September, the US Federal Reserve cut interest rates by 50 basis points with an expectation of gradually reducing to the ‘neutral rate’ (a theoretical rate that would allow the economy to grow sustainably without causing inflation – currently 2.9%) anticipated, given the significant progress on inflation. The head of the Federal Reserve Jerome Powell signaled to markets that they are ‘recalibrating’ rates in the US to avoid the risk of leaving them elevated for too long, which might cause a major labour market slowdown.

The rate drop was announced against a backdrop of weaker numbers in the labour market, with US job openings falling to the lowest level in more than three years in July. It is anticipated that the Fed will continue to cut rates by 25 basis points at every meeting until June next year, to reduce the Fed funds rate to 3.3%.

Equity and bond markets had a mixed reaction with most market participants expecting a narrower rate cut of 25 basis points. Falling interest rates in the US are positive for global stocks, particularly if the US economy can avoid a major slowdown and achieve a relative soft landing, with economic growth remaining robust throughout.

A fall in interest rates will boost more rate-sensitive sectors such as real estate, utilities and consumer discretionary stocks, which have lagged compared to communication services and technology stocks. This should help see a broadening out in markets, with small and mid-cap companies outperforming, given the valuation gap when compared to mega/large cap companies, within which the rally has been more heavily concentrated year to date.

Trump versus Harris

The final major US Presidential Debate took place on 11th September, with several commentators declaring Kamala Harris the overall winner. However, at the time of writing, with less than 35 days remaining until the election, markets are currently pricing in a 50/50 chance of either candidate winning.

If Donald Trump wins the Presidential Election, it will likely benefit US domestic stocks, with the financial sector benefitting from lower regulation. His focus is on protectionism and the reshoring of supply chains and production, supporting industrial businesses.

However, from the macro perspective, policies to reduce immigration and the prospect of tariffs would likely result in higher inflation as wages and import costs rise. Therefore, any gain from expansionary fiscal (taxation) policy would likely be offset by monetary headwinds of higher rates over the long-term.

If Kamala Harris were to win, markets may react with a degree of caution due to fears over increased corporation taxes and greater regulation in certain sectors, such as energy and financials. Sectors which may benefit include clean energy, technology, infrastructure and healthcare, the latter via reforms through which democrats aim to create opportunities for companies to provide better level healthcare services to consumers.

While there is likely to be further volatility in the run up to the US Election on the 5th November, it is important to point out that markets tend to perform well following an announcement of a US presidency, with other variables such as stages of economic cycle, sentiment and corporate fundamentals being key drivers of returns over the long-term.

Source: Oxford Economics

Bank of England Holds Firm

The Bank of England left interest rates unchanged at 5% after inflation remained at 2.2%. However, service inflation increased to 5.6% due to in part to sharp increases in air fares. Nevertheless, they indicated that interest rates may still be cut by a further 25 basis points in November.

The Bank of England have forecasted that inflation is likely to increase to 2.5% towards the end of the year and the UK economy will grow at 0.3% in the final quarter of the year. However, despite what mainstream media states we believe the UK economy is in good shape due to the resilience of the consumer.

Consumer cashflow is improving dramatically, unemployment remains low and individual savings rates remain high. Alongside this, with global interest rates now starting to fall and arguably greater political stability in the UK, this should help support UK equities which are still cheap compared other developed markets.

The Boolers Investment Committee