Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin July 2025

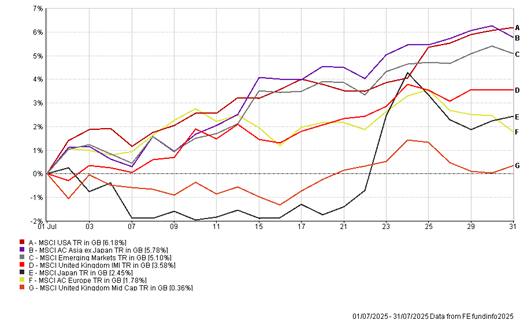

Markets had another positive month, as (secured) US trade deals and companies reporting solid earnings helped further boost investor sentiment. The performances of the main equity indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

Equities Climb the Wall of Worry

US indices, led by the S&P 500 and Nasdaq 100 benefited from strong earnings in technology and sentiment was buoyed by resilient consumer spending, AI enthusiasm and confidence that broad tariff threats have receded, with major trade deals completed with Europe and Japan. While investor confidence has held up well, valuations are becoming increasingly stretched in certain sectors, particularly US tech—highlighting the importance of selectivity and diversification. The accelerated gains have raised concerns including rising bond yields, a weakening labour market and overreliance and concentration in AI stocks.

In Europe, sluggish growth, weaker PMI data and reduced forward earnings guidance led to relative underperformance. The Euro Stoxx 50 rose 0.8% over the month, supported by a rebound in financials and industrials. On the positive side, the FTSE 100 rose above 9,000 during the month rising by nearly 4% led by energy, mining, and banking sectors and overall is up 11% year to date, as investors have increasingly re-allocated from US equities into other value opportunities such as the UK.

Inflation Isn’t Done…Quite Yet

Across the US, UK, and parts of Europe, inflationary pressures made an unwelcome return in July, particularly in the US and UK. US consumer prices rose to 2.7% YoY, surprising markets to the upside. UK core inflation remained persistently high at 3.7%, despite earlier signs of easing. Central banks including the Federal Reserve, European Central Bank (ECB) and Bank of England (BOE) maintained hawkish or cautious tones, pushing back expectations for near-term rate cuts. This forced investors to recalibrate their timelines for central bank easing, pushing bond yields higher and keeping risk assets on edge.

This shift in expectations pushed bond yields higher globally and led to a more cautious outlook for rate-sensitive assets. Markets now expect the US Federal Reserve to first cut in December 2025 at the earliest. The ECB are expected to possibly cut in Q4, but outlook is clouded by energy prices. The BOE are still battling high services inflation, and it is likely cuts may be delayed to late 2025 but recent weakness in the labour market may mean rate cuts could come sooner rather than later.

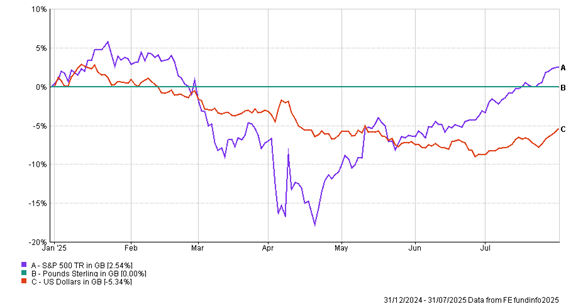

The Dollar Strikes Back… But Remains Structurally Under Pressure

With the Fed staying hawkish and US growth holding firm, the dollar strengthened significantly in July. This added pressure to emerging market assets and commodities, while reigniting debate over how long the global policy divergence can last. The dollar index rose 1.5% for the month. Sterling and Euro both weakened, and emerging market currencies came under renewed pressure.

This year so far, the US dollar Index is down 5.3% versus Sterling, which has been a headwind for non-US based investors. For example, year to date the S&P 500 is up by 8.3% in US dollar terms and in sterling terms the S&P 500 has increased by 2.5%.

Since the start of the year, long-term capital flows have been declining in the US, as foreign investors reassess the fundamentals of the US economy due to rising fiscal deficits, which have have pushed long-term bond yields higher. We think this likely to continue in the future and suspect that fiscal imbalances, weakening capital inflows, and evolving monetary/fiscal policies across the G10 are expected to weigh on the dollar in the medium term.

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

Portfolio Changes

Within the Boolers Funds, this month we have sold the Fidelity Emerging Markets OEIC due to relative underperformance and to gain greater exposure to China, with reinvestment made into the Artemis SmartGARP Global Emerging Markets Equity OEIC which will provide a blended exposure to EM companies with a value tilt. The changes are also being mirrored across our DFM models shortly.

BOOLERS INVESTMENT COMMITTEE