Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin August 2025

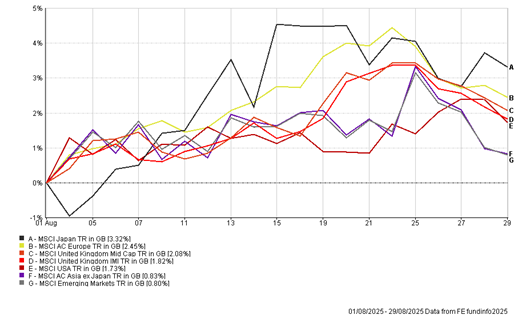

Overall, markets had another positive month, as Chair Powell used Jackson Hole to open the door to an adjustment in rate cuts if the balance of risks continues to shift from sticky inflation to a weakening labour market. The performances of the main equity indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

Equities: From Record Highs to Late-Month Chill

The S&P 500 and Nasdaq set all-time highs in mid/late August, powered by resilient mega cap technology. Yet the rally faded into month-end as semi-conductor companies such as Nvidia sold off, as cautious earnings guidance set in. Small caps outperformed, with the Russell 2000 surging 7% vs 1.5% for the Nasdaq-100, which was a rare rotation into domestic led US stocks on the back of potential rate cuts from the Federal Reserve.

In the UK, the FTSE 100 clocked record closes mid-month, led by consumer names, energy and staples,

defensive sectors that benefited from resilient global demand and commodity/energy exposures. Domestic-facing small caps (FTSE 250 / Russell-equivalents) were more volatile and underperformed in the month relative to large-cap exporters. The Bank of England (BOE) cut rates by 25 basis points to 4.0%, the first step down after years of tight policy. But July inflation CPI surprised at 3.8% year on year, forcing a cautious tone by the BOE, in that further easing isn’t guaranteed. Sterling gained modestly against the dollar, offering some relief to sterling-based investors holding overseas stocks.

While the U.S. Fed shifted toward potential easing (dampening the dollar), the Bank of Japan maintained its ultra-accommodative stance. This divergence strengthened the environment for equities and kept the yen weak, further boosting exporters’ earnings. The Nikkei and Topix soared to new records above 43,000 and 3,000, boosted by a U.S.–Japan tariff truce, a weak yen, and robust earnings momentum. Strong earnings came from industrials, semi-conductors, autos, and technology combined with renewed confidence in governance and profitability, further supported momentum.

Jackson Hole Jolts

Jerome Powell, in his last Jackson Hole speech as Fed Chair, acknowledged that while inflation is easing, it remains above target and the the “balance of risks” has shifted to the downside in the labour market, which now outweigh the risks of inflation.

Therefore, he signalled the economy may now warrant a policy adjustment, widely interpreted as a possible rate cut in September, although he stopped short of committing that was the case. The speech took place under the shadow of President Trump’s escalating pressure on the Fed, including public calls for rate cuts and targeting officials like Governor Lisa Cook.

Crucially, Powell reaffirmed that decisions would remain data-driven and independent, defending the Fed’s autonomy amid mounting political pressure. Futures markets quickly repriced the probability of a September cut to 85%, with further easing expected by year-end.

Portfolio Changes

This month we have sold our direct healthcare exposure, Polar Global Healthcare BlueChip OF due to tariff concerns and reinvested to provide additional diversification and protection within the portfolio in Jupiter Global Equity Absolute Return OEIC for Cautious/Balanced funds and models and Natixis Loomis Sayles Long Short Equity Fund OF for the Adventurous Fund.

In addition, for the Adventurous Fund/model, we have sold Kempen Global Small Cap OF and bought Janus Henderson Global Smaller Companies OEIC with the aim of providing better ‘consistency’ returns in global smaller companies over the long term.

BOOLERS INVESTMENT COMMITTEE