Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin September 2025

Key Takeaways

Markets

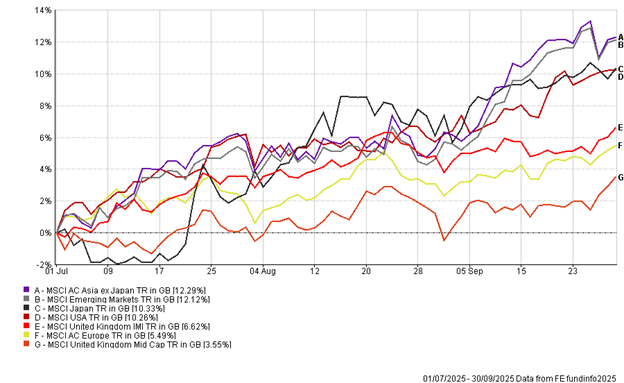

The third quarter of 2025 was characterised by a strong rebound in global equity markets, summarised in the chart below, despite persistent policy driven volatility and macroeconomic uncertainty. U.S. and global stocks rallied, led by large-cap growth names, as investors responded positively to signs of economic resilience.

All figures are based on bid-bid prices with income reinvested

The U.S. economy remained in expansion mode, though inflation risks lingered due to ongoing tariff implementations and a tight labour market. Central banks, including the Federal Reserve (Fed) and the European Central Bank, adopted a more cautious stance, with the Fed initiating a modest rate cut by 25 basis points (rather than a bullish 50 basis points) in September signalling a data-dependent approach going forward. For UK investors, this global backdrop provided a constructive environment for diversified portfolios, particularly those with exposure to U.S. and Emerging/Asian market equities.

Global Equities Lead the Charge

Valuations in U.S. equities remain elevated, prompting a shift in investor interest toward non-U.S. markets, where investors saw more compelling long-term value. International developed and emerging markets outperformed, buoyed by a weaker U.S. dollar and improving sentiment around global trade.

The tariff regime introduced earlier in the year continued to reverberate through supply chains, but markets appeared to have digested the worst of the impact, with investor risk tolerance rebounding from April lows. Emerging markets are up 27% year to date, buoyed by capital inflows and commodity strength. For UK investors, global equity funds especially those with U.S. and Asia-Pacific exposure, delivered strong relative performance.

Despite the higher valuations, S&P 500 and Nasdaq indices posted double digit gains for the quarter, the S&P 500 rose nearly 8%, while the Nasdaq jumped over 11%, in sterling terms, driven by strong earnings and optimism around AI and tech innovation. Small-cap stocks also outperformed, reflecting renewed confidence in domestic growth and interest rate cuts. Europe showed signs of structural recovery, particularly in sectors tied to infrastructure and industrial reform.

UK – Steady but Subdued

The UK equity market lagged global peers, with the FTSE 100 posting modest gains, reaching all-time highs amid a stronger pound and mixed economic data. Domestic inflation remained sticky in August, prompting speculation that the Bank of England will keep rates interest rates at 4% for the rest of the year. UK gilts rallied modestly initially with yields easing across the yield curve before pushing higher, the 10-year gilt yield currently trades at 4.73%. Sterling strength, driven by improving trade balances and capital inflows, slightly dampened returns on unhedged overseas assets.

Oil prices spiked due to OPEC+ supply constraints and geopolitical tensions in the Middle East, with Brent Crude climbing above $70. Precious metals like gold and silver held firm, supported by safe-haven demand and inflation hedging. UK investors with exposure to commodity-linked equities or diversified natural resource funds benefited from this trend, particularly in energy and mining sectors.

Stay Global, Stay Nimble

For UK based investors, Q3 reinforced the value of global diversification. While domestic markets underperformed, international equities and global fixed income provided strong returns. Looking ahead, the investment landscape remains complex, with central bank policy, tariff led inflation dynamics, and geopolitical developments all in play. A balanced approach, combining global equity exposure, quality credit at the short end of the yield curve, and inflation protection remain key to navigating the final quarter of 2025.

BOOLERS INVESTMENT COMMITTEE