Simon Watts

Reveal Menu

2025 End of Year Market Commentary – Mad World

At times, it felt during 2025 as though we had slipped into another dimension. The Boolers’ Investment Committee often found itself debating issues in global economics and geopolitics that would have seemed unimaginable only months before.

For this, we largely have President Donald Trump to thank. In a unique way, almost every major global economic, market, or political event during 2025 bore traces of Trumpian influence. Whatever one’s view of him, few would dispute that his work rate is extraordinary. Combining his relentless activity with a worldview that can be generously described as “unconventional” made for a rollercoaster year — and we have at least three more of these still ahead of us.

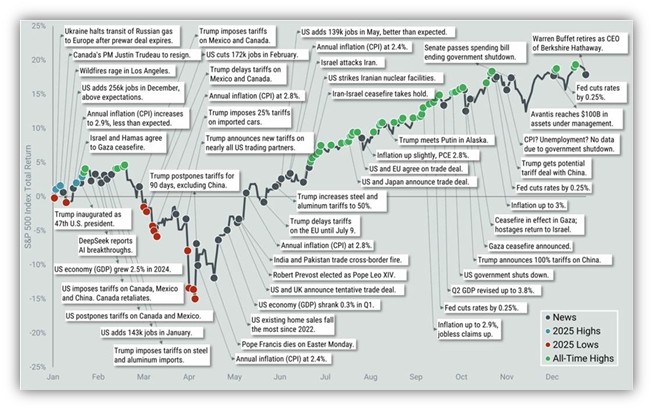

The following chart captures, in part, just how eventful 2025 proved to be, using the S&P 500 index to reflect its highs and lows.

Source: Avantis Investments

January brought one of the few notable market developments that did not involve the US President. When DeepSeek’s AI language model (chatbot) was reported to match leading Western models while costing 20–50 times less to operate, investors feared that such efficiency could sharply curtail long‑term demand for Nvidia’s advanced chips. NVIDIA briefly endured the largest single‑day loss in market capitalisation in history – a 17% share price fall, erasing roughly £600bn from its market value.

Even so, 2025 began on an optimistic note after the re‑election of a “market‑friendly” president. That optimism was promptly tested in February when Trump threatened a new wave of global trade tariffs — broader and higher than anything proposed during his first term.

On 7th March, the release of the UK’s Eurovision Song Contest entry, What the Hell Just Happened? presciently captured our immediate reaction to Trump’s “Liberation Day” speech on 2nd April, which outlined tariff proposals far more punitive (and, in places, more surreal) than expected, sending markets into sharp decline again.

Yet the resulting turmoil in both bond and equity markets prompted the US President to reverse or at least postpone his most severe tariff proposals, earning him the tongue‑in‑cheek acronym TACO: Trump Always Chickens Out.

As markets came to realise that many of these tariff threats would go unfulfilled, confidence gradually returned from May onwards. Whilst the legality of US trade measures remains under Supreme Court review, investors are largely pricing as though the issue were resolved.

In the technology sector, caution sparked by January’s AI shock faded quickly, replaced by another wave of AI‑fuelled enthusiasm that helped drive valuations higher once again.

Thus, 2025 concluded on a positive note after a turbulent first half – a rare example of uncertainty without volatility – though concerns about market complacency now follow us into 2026. After reviewing key asset classes, we’ll consider briefly what the year ahead might hold.

Bonds – Under Pressure

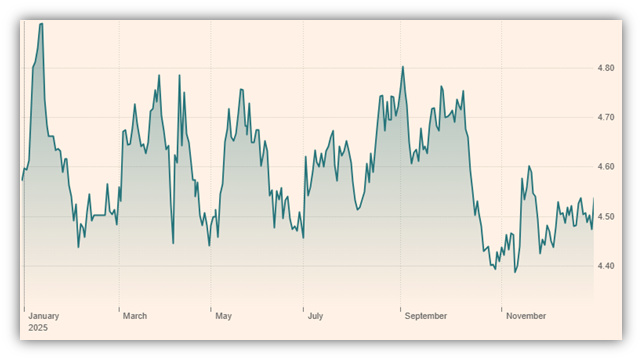

UK gilts started 2025 under pressure, with long‑dated yields reaching levels last seen in the late 1990s. 10‑year yields revisited ranges associated with the 2008 Global Financial Crisis as markets reassessed the “higher for longer” UK interest rate path and heavy supply (higher government borrowing).

Later in the year, softer employment and pay data, and expectations of additional Bank of England easing into 2026, supported gilts, with several managers describing yields as cheap versus UK growth fundamentals and peers.

Gilt yields finished the year roughly where they started, which means that investors would have benefited from an income return of around 4.5%, based on the default 10-year yield.

10 Year Gilt Yields in 2025

Source: Financial Times

Globally, government bond markets oscillated between worries over sticky inflation and growth resilience early in the year, then by increasing confidence that cooling labour markets and slower growth would permit gradual rate cuts by major central banks through 2026.

Episodes of geopolitical tension and tariff announcements periodically pushed yields higher and capital values lower, but these moves tended to fade as policymakers stepped back from the most extreme measures, leaving global sovereign indices broadly flat to modestly positive.

In summary, bonds have been a pretty reliable home for client money over 2025 (though, like equities, not without periods of volatility), as real yields have been positive without having to take excessive risks with bond duration or quality. Interest rate cut expectations in 2026 (provided they are fulfilled) should provide further upside, but in the UK especially, this has to be balanced with government borrowing levels (new debt issuance) and how the bond markets themselves view the Labour government’s economic policy and growth expectations.

Currencies – Money For Nothing

Whilst equity and bond markets learned to live with Trump’s notably unconventional trade and foreign policies, currency markets appear to have marked down the US on account of “policy volatility”, reflected in eroding institutional credibility, concerns over Federal Reserve independence, persistent large fiscal deficits and unpredictable tariff policy.

An alternative explanation is that the dollar was simply at the end of a long period of strength, having risen by roughly 40% over the 14 years from 2010 to 2024, with 2025 marking the start of a new phase as the Federal Reserve moved into easing and markets priced in deeper interest rate cuts.

The appreciation of Sterling was also helped by perceptions that the Bank of England would cut rates more cautiously than the Federal Reserve and by relatively calm domestic politics into the Autumn budget.

Whatever the mix of drivers, the dollar index fell by around 9–11% in 2025, its weakest calendar year since the 1970s or 1980s, depending on the measure used.

Why is this important? Many commodities, including oil, are priced in dollars, so a weaker dollar is broadly positive for UK consumers. However, UK holders of US assets will have seen around 8% of their value eroded by currency depreciation over 2025. Consequently, whilst we continue to seek exposure to US and other global markets, currency remains a material consideration and forms part of our justification for maintaining a measured degree of “home bias” towards UK assets.

Against the Euro, Sterling was modestly firmer, reflecting similar inflation and rate‑cut trajectories between the UK and the Euro Area. However, Sterling was notably strong against the Japanese Yen, reflecting the stark policy divergence between a still‑restrictive Bank of England and an ultra‑accommodative Bank of Japan. By year‑end, GBP/JPY was trading close to multi‑decade highs, with the Sterling up just over 7% versus the Yen over the year.

Interest Rates & Inflation – The Land of Make Believe

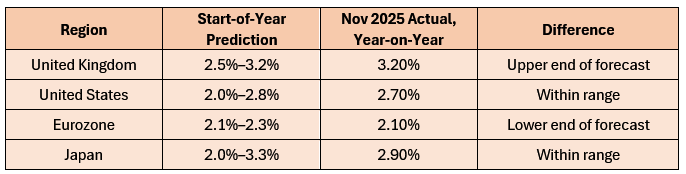

Over recent years of higher interest rates and inflation, markets have repeatedly priced in overly optimistic inflation and rate forecasts, only to adjust abruptly when reality fell short of expectations. In contrast, 2025 was more benign; for most major economies, start‑of‑year expectations for inflation and policy rates were broadly in line with what actually materialised.

The table below compares the start-of-year inflation forecasts with the latest actual year-on-year rates (November 2025).

Many forecasters expect the Bank of England to continue modest rate cuts in 2026, easing from around 3.75% toward 3.5% or lower as inflation moves toward the target. UK inflation is forecast to fall toward the BoE’s 2% target – one credible projection (PwC) predicts 1.9% by late next year.

In the US, forecasts suggest the Fed may hold rates relatively steady in 2026 after a series of cuts in 2025, with only modest easing expected rather than aggressive cuts. If US inflation rises, there could be adverse consequences for tech valuations as rates may be held for longer or even increase. US inflation for 2026 is currently predicted to be about 2.7%.

In the Eurozone, rates are more likely to be increased by the ECB by as much as 0.5%, though inflation is predicted to be 1.7%-1.9%, whilst the BoJ may increase rates to 1%, with inflation predicted to sit around 1.6%.

UK Equities – Back Where We Belong

Whilst it has been a positive year for global equities overall, UK equities have, in many cases, outshone their peers without the same degrees of currency, valuation or political risks.

UK equities had a very strong but uneven year in 2025, with large-cap stocks significantly outperforming mid and small caps, and with clear style and sector skews rather than a broad-based domestic recovery.

In 2025, the FTSE 100 delivered 25.8%, its best performance in well over a decade, helped by currency weakness, robust commodity prices and strong performance from a handful of global blue chips. Mid and small-cap stocks also performed well, with the FTSE 250 and FTSE Small Cap indices returning 13.0% and 14.4% respectively, reflecting greater sensitivity to UK fiscal (tax) policy and the domestic growth outlook.

Value stocks continued their outperformance at the large‑cap end, particularly banks, mining and defence companies, where rising rates, higher commodity prices and elevated geopolitical risk supported earnings and valuations. Quality Growth stocks with strong cash generation and defensible franchises generally outperformed cyclical, profit‑light names, while more speculative small‑cap growth continued to de‑rate or tread water.

Overseas‑earning multinationals significantly outpaced domestically geared UK names, helped by global demand in areas like defence, resources and healthcare, and ongoing international investor interest in “cheap UK” large caps.

Starting valuations for UK equities in 2026, particularly for mid and small caps, remain undemanding relative to developed‑market peers, with higher cash dividend and buyback yields offering a supportive starting point. If global growth holds up and domestic policy noise stabilises, there is scope for upside in UK mid and small caps, as well as continued interest in high‑quality, globally diversified FTSE 100 names from international investors seeking diversification away from the US.

We remain bullish on the UK equity market, believing that despite its recent outperformance at the large cap end there is still further upside, that the market as a whole (but particularly mid and small caps) is still relatively undervalued at a point when global investors are beginning to look for alternatives to the expensive US market for some of their equity allocations.

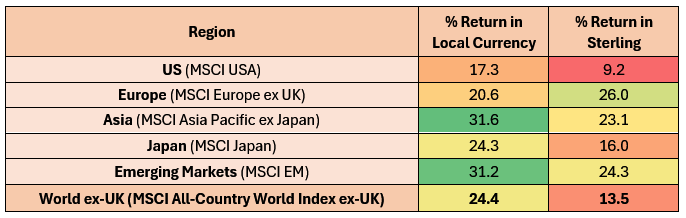

Overseas Equities (in Local Currency & Sterling-Adjusted) – Say Hello, Wave Goodbye

Index performances for overseas equity markets in 2025 are shown below in both Sterling and local currency:

The above table shows that US equities still had a very positive, but in relative terms an uncharacteristically poor year in 2025, bringing up the rear in both local currency and Sterling terms. In Sterling terms Europe was slightly ahead of resurgent Asian and Emerging Markets, with Japan above the US and the global ex-UK index (which is two-thirds weighted in the US).

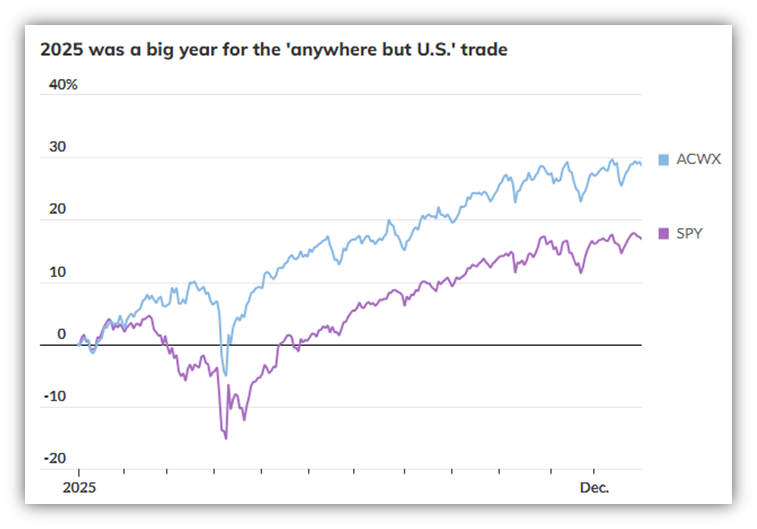

North America – The Lion Sleeps Tonight

ACWX = MSCI All-Country World ex-US Index

SPY = S&P 500 Index

Source: Factset

In our year-end commentary last year, we noted that the US offered a fascinating investment opportunity with extraordinary recent returns, but cautioned that prolonged outperformance had stretched valuations beyond reasonable bounds for many stocks.

Revisiting the so-called Magnificent 7 (Nvidia, Microsoft, Amazon, Alphabet, Meta Platforms and Tesla), valuations for most remain no more overstretched than a year ago—with Tesla a clear exception—though the risks from extreme index concentration persist.

US equities underperformed straightforwardly in 2025: they started from elevated relative valuations, bore the brunt of Trump tariff fallout, and missed much of the dollar weakness boost that aided Asia and emerging markets.

We stay constructive on US equities, anchored by consistently strong corporate earnings and the fact that America hosts global leaders across key industries; we are expecting to add further to our weighting as and when opportunities arise in 2026.

Solid if slower US growth looks likely, aided by easier financial conditions, fading tariff drag and resilient consumer demand, with an ongoing focus on quality balance sheets and reasonable valuations in tech, industrials and healthcare rather than chasing Magnificent 7 multiple expansion.

Key risks remain: renewed inflation, mistimed Fed cuts, tariff/geopolitical shocks, AI productivity/profit shortfalls against hyped narratives, a softer labour market and possible stagflation.

Europe – One Step Beyond

European equities delivered stellar performance in 2025, significantly outperforming US markets with a charge led by large cap Value stocks, banks and cyclical stocks, despite persistent downward earnings revisions, unlike the more stable US trajectory.

Fiscal stimulus provided a strong tailwind, notably Germany’s infrastructure/debt-brake reform, ramped-up defence spending and elevated capital expenditure in infrastructure, energy transition and security.

Positive momentum could feasibly continue into 2026 with broadening leadership beyond banks and defence, though tariff escalation or a China slowdown pose key risks. However, attractive valuations offer something of a buffer.

Historically underweight Europe, we added an Exchange Traded Fund (ETF) focused on large-cap, high-dividend value stocks in 2025 — its 30%+ weighting in banks made a meaningful positive contribution. Our European equity exposure is currently under review and could increase further in 2026.

Japan, Asian & Emerging Markets – Eye of the Tiger

Japan, Asian and Emerging Market equities delivered divergent but generally strong performances in 2025, with standout regional leaders powered by monetary stimulus (China), AI supply chain tailwinds and dollar weakness, though China and India showed mixed results amid trade noise from the US.

Japan benefited from corporate governance reforms, wage growth and AI/semiconductor exposure, with domestic stocks performing particularly well in what turned out to be a broad-based rally.

China/Hong Kong performance was led by AI optimism (DeepSeek), fiscal/monetary stimulus, resilient exports (despite US tariffs) and domestic consumption (travel, electric vehicle sales). In recent years, China has prudently desensitised its reliance on the US for its exports, possibly in anticipation of a second Trump term!

South Korea/Taiwan enjoyed exceptional gains from AI enthusiasm and semiconductors, whilst South Korea also saw defence demand surge.

India lagged regional peers due to high starting valuations (similar to the US), tariff exposure concerns and post-election volatility, though economic growth remained very solid at 7%.

The strong momentum seen in 2025 is expected to continue into 2026, with 12–15% earnings growth expected, which could be assisted by continuing dollar weakness and further policy support (China stimulus, Japan reforms) plus AI demand. However, as is the case elsewhere, geopolitical risks loom large.

Gold – Indestructible?

Gold and silver prices have surged dramatically since January 2025, with gold rising over 70% to near $4,460 per ounce and silver soaring nearly 150% to around $80 per ounce by year-end, driven by central bank purchases, geopolitical tensions and safe-haven demand amid economic uncertainty.

Gold shattered historical norms in 2025, with both gold and silver breaking decade-long resistance levels, but why all of a sudden? For gold, one could point a finger towards Donald Trump. Central banks, particularly in emerging markets like China and India, accelerated de-dollarisation by accumulating physical gold at unprecedented rates. Silver, on the other hand, benefited from explosive industrial demand in solar panels and EVs.

Other reasons for the rise include persistent inflation fears and constrained mining supply from years of underinvestment. Geopolitical risks, including US tariff policies and global conflicts, elevate the safe-haven appeal, while silver’s dual monetary-industrial role created a supply-demand imbalance.

So will the rise continue? Likely yes, but perhaps not at the same pace as 2025, as investors in these markets are already highly leveraged. Ongoing central bank buying looks set to continue – China has steadily been reducing its reliance on US Treasury debt, and by some estimates is only just over a third of the way through this exercise. Industrial silver demand is projected to hit new records in 2026, with green energy growth providing a tailwind to further gains.

However, whenever one considers investing in an asset that has just seen a spike in its price, the downside risks should be considered far more carefully. Sharp reversals could result from any Fed rate hikes, economic slowdowns curbing industrial demand, or dollar strength if US growth outperforms (which it has a nasty habit of doing in recent years). Historical precedents show precious metals vulnerable to post-rally corrections, with 2025’s extreme gains (gold’s strongest since 2010, silver’s since 1980) inviting profit-taking and volatility. Over-allocating risks to significant drawdowns, as metals lack any form of income yield and can lag equities in risk-on environments, making heavy bets a dangerous strategy without diversification.

So how do we play this current rally? We favour the long-term industrial demand thesis over shorter-term geopolitical drivers, so in October, we added exposure via the VanEck Global Mining ETF, which invests roughly equally in mining stocks across precious and industrial metals. These miners had rallied strongly in preceding months yet remained attractively valued against historic norms and broader US equities, buoyed by prospects for rising capex, enhanced operational efficiencies, and expanding profit margins. We view them as less exposed to downside risks than pure-play metals, offering leveraged upside with a buffer from equity diversification. We will be reviewing this position early in the New Year.

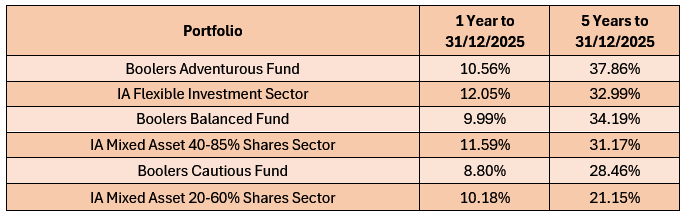

Portfolio Performance & Changes – Dear Prudence

Portfolios across all risk categories in the main will have finished in positive territory for a third consecutive year, with the more equity-heavy Adventurous portfolios outperforming as they did in 2023 and 2024.

In March, we launched three fund structures (Open-Ended Investment Companies, or OEICs) as a natural progression for our Discretionary Fund Management Service; many of our clients have successfully transitioned to the new structure, which now accounts for the majority of assets under our management.

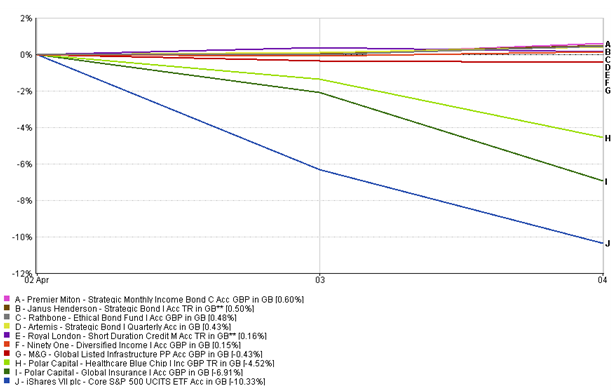

Trump’s Liberation Day speech and the ensuing market turmoil struck during this transitional phase; however, we leveraged the new fund structure to our clients’ benefit by monitoring daily cash inflows and deploying them tactically – first into lower-risk and alternative assets, then rotating back into higher-risk opportunities at depressed prices.

As the following table illustrates, our alternative assets and bond holdings fared well at the time relative to the S&P 500, which lost over 10% in the two days following the speech:

Source: Financial Express

The performance of Boolers’ different risk models is shown below:

Notes

Whilst our funds comfortably outperform peer group averages over 5 years, the 1-year returns trail slightly. This reflects no issues with the new fund structure transition but a deliberate, measured stance (where cash levels have been elevated within the funds) amid unprecedented equity market volatility triggered by President Trump’s policy pivots and shocks. Importantly, this also gives us flexibility to deploy cash selectively when compelling opportunities arise.

Heightened uncertainty from Trump’s Liberation Day speech, tariff announcements and fiscal shifts created sharp drawdowns, rewarding aggressive risk-on bets only in hindsight. Our tactical deployment—prioritising lower-risk and alternatives initially, then re-entering equities at discounts – preserved capital and positioned for recovery without chasing peaks. This approach prioritises long-term compounding over short-term FOMO (Fear Of Missing Out), as evidenced by superior 5-year results and alignment with client mandates for prudence.

Cautious navigation through 2025’s turmoil avoided permanent losses, enabling outperformance over cycles where peers suffered deeper reversals. Investors benefit from this discipline, as volatility often punishes the reckless whilst rewarding patience.

Conclusion: Trump 2026 – Friend or Foe?

President Trump’s aggressive foreign policy in 2026—marked by bold moves on Venezuela, Greenland, and threats against Iran intensifies global tensions, challenging the post-WWII rules-based order with a stark “Might Is Right” doctrine.

His administration’s intervention in Venezuela, seizing the leader of a sovereign nation and incarcerating him in the US, seizing oil tankers and declaring an intention to “run the country”, regardless of any humanitarian or economic justifications, undermines international norms. This stance, alongside overtures to annex Greenland and hawkish rhetoric toward Iran, signals US unilateralism, potentially emboldening China to invade Taiwan under similar pretexts of strategic necessity, justifying aggression with Trump’s precedents.

Such actions erode trust in multilateral institutions, elevating tail risks for energy markets and supply chains and pressuring inflation. Yet global equities have historically decoupled from isolated conflicts – outside of a China/Taiwan crisis, which could trigger semiconductor shortages and a huge tech selloff – greater self-reliance from European nations has already led to fiscal stimulus, and this is likely to continue, which is positive for equity markets.

However, we believe 2026 warrants measured optimism. Resilient corporate earnings, AI productivity gains, further fiscal stimulus and monetary easing all provide a very promising backdrop for global equity returns, somewhat in spite of the geopolitical noise in the foreground.

Our tactical caution through 2025’s shocks placed a premium on preserving capital amid volatility, aligning with client goals for steady compounding. Trump may prove a foe to stability but a friend to US-centric growth and growing self-sufficiency elsewhere; prudent positioning across regions and assets navigates both.

THE BOOLERS INVESTMENT COMMITTEE