Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin June 2026

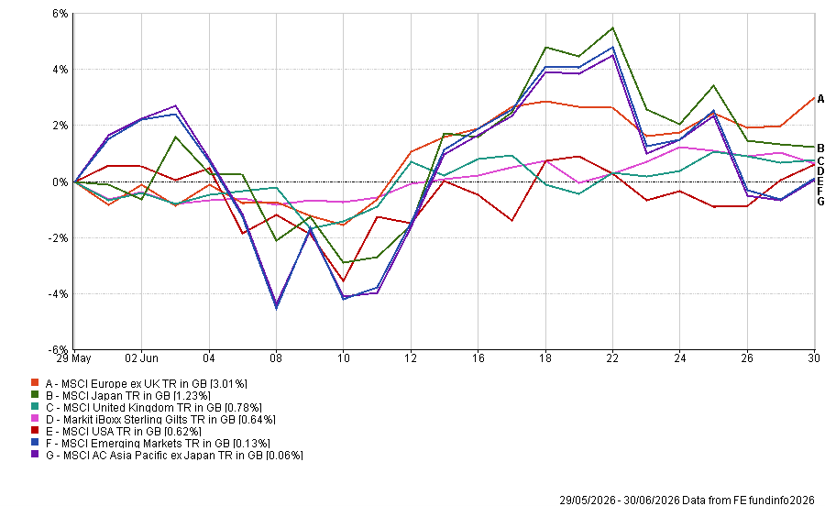

June saw the start of the FIFA World Cup in Mexico, USA and Canada and the performance of major global equity indices have certainly followed a game of two halves (fortunately without hydration breaks!) falling in the first part of the month with a recovery in the second part of the month, as highlighted in the table below.

(All figures are based on bid‑bid prices with income reinvested unless otherwise stated)

With the first half of 2026 behind us, it is a good moment to step back and look at the bigger picture. Markets this year have been driven by the same handful of themes since January and understanding them explains both the strong returns and the wide gaps between regions.

Key Points

Inflation and More Hawkish Central Banks

The year’s biggest headwind came from the conflict involving Iran, which disrupted energy supplies and pushed the oil price sharply higher. Because energy feeds into the cost of almost everything, this reignited inflation just as it had been coming under control. This was not simply an energy story; however, the wider economy has been resilient.

The enormous build out of data centres to power the AI boom has poured investment into the economy, and this spending ripples outwards through a ‘multiplier effect’, creating jobs and demand well beyond the technology sector. Tax cuts contained in the ‘One Big Beautiful Bill’ have added further fuel, putting more money in the hands of both companies and consumers. The result has been strong economic growth which, combined with higher energy prices and the potential knock-on ‘secondary’ effects that follow, is likely to keep inflation stickier than expected.

Central banks in the US, UK, and Europe responded by turning noticeably more ‘hawkish’, signalling that interest rates would need to stay higher for longer and dampening earlier hopes of cuts. Higher for longer rates are a particular drag on expensive shares and on bonds.

Solid Earnings and the AI Frenzy

Set against these headwinds, companies kept delivering. Corporate earnings across most regions came in solidly, reassuring investors that businesses could keep growing despite higher costs. At the same time, enthusiasm for artificial intelligence, the ‘AI frenzy’, showed no sign of fading, and demand for the chips and hardware that power AI benefited technology manufacturers around the world, many of which are based in Asia.

Excitement was further fuelled by a wave of high-profile listings, the largest of which was SpaceX. Its June flotation was the biggest in stock market history, raising around $75 billion. The shares were priced at $135, opened at roughly $150 and closed their first day near $161, briefly valuing the company at more than $2 trillion.

After spiking above $225, the price fell back sharply during a wider technology sell-off and, by the end of June, had settled at around $150, still comfortably above where it floated. Speculation about potential future listings from leading AI companies such as Anthropic and OpenAI is likely to keep appetite for the sector high, though we will always weigh such excitement against valuation and long-term fundamentals.

Asia and Emerging Markets Lead, the US Lags

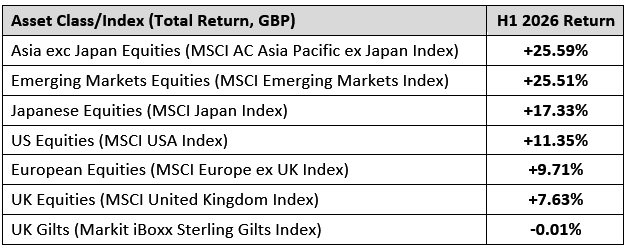

These themes combined to reshape the usual pecking order. For much of the past decade the US led global markets; Asia Pacific (excluding Japan) and Emerging Markets each returned more than 25% over the half-year, benefiting from the AI boom, stronger growth, and attractive valuations.

The US still made progress, rising 11.35%, but lagged the leaders as higher-for-longer interest rates weighed on its richly valued technology giants. A weaker US dollar compounded the effect for UK investors like us, reducing the value of American returns once converted back into pounds. Europe (excluding the UK) and the UK delivered solid returns of 9.71% and 7.63% respectively. The table below summarises how each major market performed over the first half of the year.

Source: FE fundinfo, 31/12/2025 – 30/06/2026.

Portfolio Changes

After such a strong period, particularly in Asia and Emerging Markets, we have recently been taking some profits by trimming a number of our best performing holdings across our three OEIC Funds and re-allocated the profits to the Jupiter Global Equity Absolute Return fund, to provide protection against short-term market volatility while still being able to benefit should markets continue to rally.

This is a deliberate part of how we manage risk. When certain areas of a portfolio grow rapidly, they can come to represent a larger share than we are comfortable with, and locking in some of those gains helps keep portfolios balanced and resilient.

This reflects a philosophy we describe as ‘protect and participate’. We want to protect the strong gains our clients have enjoyed, mindful that resurgent inflation, more hawkish central banks, or any cooling of AI enthusiasm could trigger a pullback. We do this by not letting a single theme dominate and by rebuilding a modest cash buffer that can be put to work if markets fall back.

Equally, we have no wish to sit on the sidelines while these trends continue, so portfolios remain substantially invested and able to participate in any further market strength.

In short, we are not calling an end to the rally, but we are being disciplined. By gradually trimming winners and holding a little more in reserve, we aim to preserve what has been achieved while remaining well placed to benefit from the opportunities that lie ahead. As always, we continue to monitor markets closely and will act as conditions evolve.

BOOLERS INVESTMENT COMMITTEE