Sian Kent

Reveal Menu

A Child Trust Fund: What is it? And what should your child do with their money?

A Child Trust Fund (CTF) is a savings or investment account for young children. It was designed to introduce youngsters to financial concepts while ensuring they had a savings account in place when they reached adulthood.

Launched in 2005 for those children born after 1st September 2002, the first CTFs matured this month.

If your child is due to receive a payout from theirs, how much might they receive, what should they be doing with their money, and what financial lessons can you pass on?

First off though, a brief history lesson.

What is a CTF?

Introduced by the government to encourage children to think about long-term savings and to give a financial boost to those reaching age 18, parents could open a CTF account using a government voucher worth £250. This amount was boosted by an additional £250 for low-income families.

Parents, grandparents, and family friends were then free to pay into the account, up to an annual limit. The limit began at £1,200. It stands at £9,000 for the 2020/21 tax year, in-line with the JISA allowance.

All money earned from a CTF is tax-free, with no tax on interest or Capital Gains Tax (CGT) to pay.

CTFs were phased out from 2010 and the last children eligible for one would have been born before 2 January 2011. They were replaced by the Junior ISA.

If you hold a CTF for your child, it remains valid and will mature when your child reaches age 18.

There are three main types of CTF:

1. Cash

You make deposits just as you would with a savings account. Any interest you earn is tax-free.

2. Stakeholder

The money you place in the account is invested in the stock market. Financial risk is minimised by a gradual move to lower-risk investments when the child reaches age 13.

3. Shares-based

The money you deposit is invested in shares but without the protections of a stakeholder account. You are though free to choose where the money is invested.

How much are they worth?

The value of your child’s fund will depend on several factors, including:

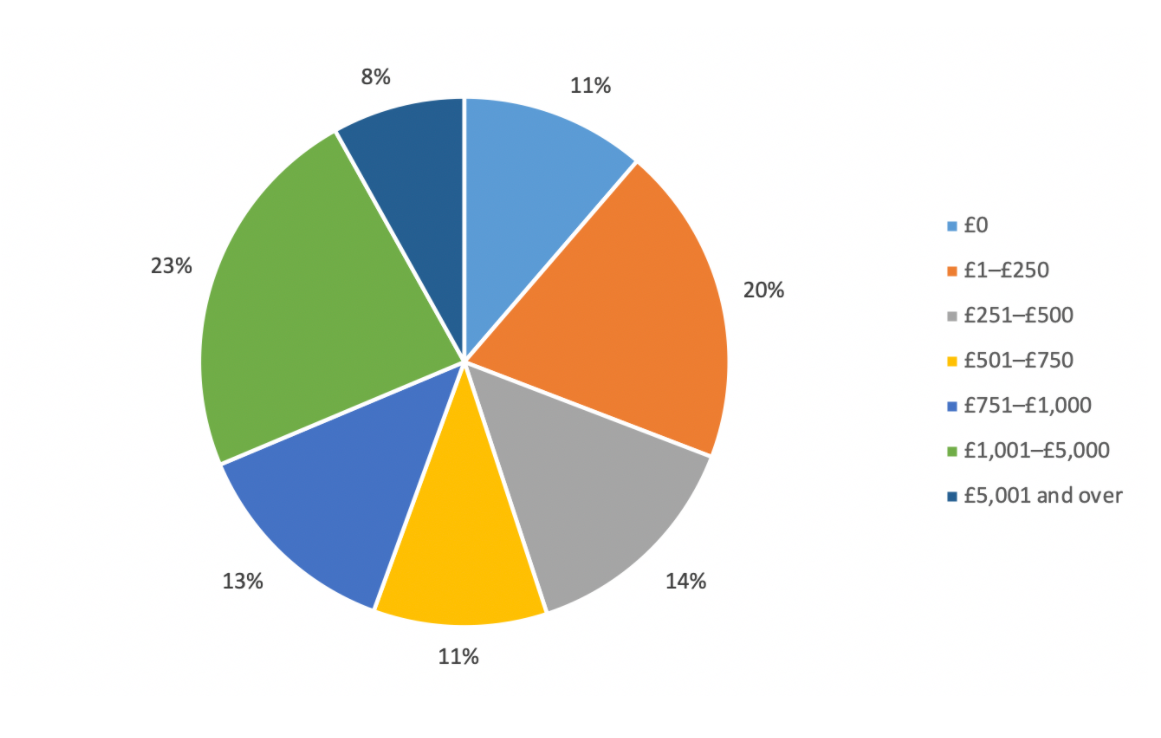

The Institute for Fiscal Studies has looked at the average values of 2016/18 CTFs for those born during the first year of eligibility (between September 2002 and August 2003).

Source: Institute for Fiscal Studies

While 45% of the CTFs taken out during that time will have a fund value of less than £500, nearly a quarter (23%) will have more than £1,000.

A lucky 8% will be in line to receive more than £5,000.

However much your child is about to receive, it’s important they use the money wisely.

What should your child do with their CTF payout?

As long as your child’s CTF provider is authorised to offer ISAs, if your child chooses not to take the cash now, it will be converted to an adult ISA. This will be a Cash or a Stocks and Shares ISA, depending on the type of CTF held.

ISAs are tax-efficient. As with the CTF, interest from a Cash ISA is tax-free and any gains your child makes on investments in a Stocks and Shares ISA are free of both Income Tax and Capital Gains Tax (CGT). The ISA allowance currently stands at £20,000 a year.

It’s also never too early to start saving towards a pension.

The earlier financial advice is received, the higher the chance of beneficial outcomes in later life. If you’d like to talk to us about savings or investments for your child, get in touch.

If your child is looking to start saving towards a first home, they might consider a Lifetime ISA.

Available to anyone aged between 18 and 39, investments made into a LISA receive an additional 25% top-up from the government each year. But the fund must be used to buy a first house or left invested until after your child’s 60th birthday.

A great way to help your child onto the property ladder, be aware that withdrawals made before age 60, and not used towards a first house purchase, will be subject to a 25% charge.

The annual LISA Allowance is £4,000. That means that your child could receive up to £1,000 a year from the government while also investing a further £16,000 into any other ISAs they hold.

If your child is heading to university, it might seem like a good idea to use the money to pay tuition fees upfront. This is often a waste of money.

Interest rates on Student Loan Company loans are small, and repayments only begin when your child earns above a certain threshold – for those starting university on 1st September 2020, the threshold is £26,575. But your child only pays off a percentage of the value above this threshold.

Even if your child is expecting to leave university as a high earner, paying off higher-interest debt or using the money to increase the deposit on a first home might be more beneficial in the long term.

Get in touch

Please get in touch if you’d like to discuss any aspect of your child’s finances or the best ways for you to save for their future.

Please note:

The value of investments can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.