Sian Kent

Reveal Menu

Everything your clients need to know about the rise in Dividend Tax

As the economic fallout from the coronavirus pandemic continues, low interest rates and high inflation have led to some tough decisions for the government.

Following the freezes to various allowances in March – and with more changes anticipated from the chancellor’s third budget on 27 October – September announcements included the suspension of the State Pension triple lock, the introduction of the Health and Social Care Levy, and a rise to Dividend Tax.

The latter of these changes will have significance for investors and business owners alike and could change the way your clients think about the income and the salaries they receive.

Keep reading to find out how the Dividend Tax rise will affect your clients and how Boolers’ expert financial advice can mitigate the impact.

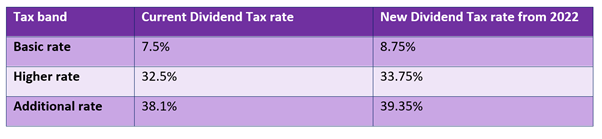

What are the changes to Dividend Tax and when do they come into effect?

Dividend Tax is set to rise by 1.25% across all tax brackets from April 2022.

Clients receiving dividends through shares or who are using dividends to supplement the salary they pay themselves from a company they own will be affected if they exceed the Dividend Allowance. The Dividend Allowance for 2021/22 stands at £2,000.

It is also worth noting that individuals also don’t pay Dividend Tax on dividend income within their Personal Allowance. This stands at £12,570 for the 2021/22 tax year and is currently frozen until at least 2026.

A client paying the higher rate of tax on dividends of £10,000 will be liable for tax at a new rate of 33.75% on £8,000. This equals £2,700 in tax and is a £100 increase compared to the current system.

Who will the rise affect?

The rise in Dividend Tax will affect investors but could be most keenly felt among your business-owner clients.

Company directors and business owners will often pay themselves a low salary, topped up by dividend payments. While the Dividend Tax rates remain below those for Income Tax, the imminent increase is likely to make dividends a less attractive proposition than previously.

The National Insurance burden for employers’ National Insurance contributions (NICs) has also been negatively affected by the announced rise to National Insurance effective from April 2022, which is set to become the new “Health and Social Care Levy” from April 2023.

Whether it is time for business owners and company directors to change their strategy for paying themselves a wage will depend on the individual, but financial advice could help to ensure that your clients make the right choice for them.

How can Boolers help your clients?

The Dividend Tax rise is just one of a raft of changes the government has announced this year as it attempts to recoup its coronavirus borrowing, aid the economic recovery, and tackle the social care crisis.

The rise of National Insurance for employers, employees, and those workers over State Pension Age will affect all of your clients differently.

The changes also need to be considered alongside the freezing of other allowances, including:

These will all impact your clients over the next five years as the value of property and investments increases and threshold amounts remain frozen.

At Boolers, the long-term financial plan we put in place for your clients will be aligned to their goals and dreams for retirement.

Through managing risk versus reward in a client’s portfolio, placing money in tax-efficient products such as ISAs (there is no Dividend Tax to pay on dividends taken from an ISA) and helping clients to focus on the long-term, we can help them mitigate the impact of changing tax allowances and legislation.

And the changes might not be finished yet, with the chancellor’s Autumn Budget due on 27 October.

Get in touch

As the government struggles to recoup coronavirus borrowing and bolster the UK’s economic recovery, more tax changes could be on the way.

Boolers can help to give your clients confidence, a sense of control, and peace of mind that their finances are on track and that their long-term goals can still be met, whatever changes occur.

If you have clients who would benefit from expert financial advice, please get in touch. Email enquiries@boolers.co.uk or call 0116 240 7070.

Please note

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.