Chris Ball

Reveal Menu

How does our UK pension system rank globally, and what does it mean for your clients?

Holland and Denmark have the best pension systems in the world according to a newly released pension index. Not only that, but these countries hold onto their respective spots for the second year running.

The 2020 Mercer CFA Institute Global report – which sees pension systems awarded points for adequacy, integrity, and sustainability – lists 39 pension systems throughout the world.

But where does the UK pension system place, and what – if anything – does this mean for your clients’ retirement?

Coronavirus and pensions

The coronavirus pandemic has led to financial instability across global markets. For those saving toward retirement, the impact of being furloughed or forced to temporarily close a business will have made for a challenging and worrying year.

For some of your clients, pension contributions might have been one of the first things to go.

Reducing or halting pension contributions can have a massive impact on when and how your clients retire. Although the impact of a short-term decrease might seem small, factor in the missed effects of compounding and the shortfall at retirement could be more significant. A client may find they have to work longer or live less comfortably in retirement than they originally planned.

The BBC recently reported that 2020 has been the worst year for the FTSE 100 since the global financial crisis. Market volatility and government borrowing globally, mean that 2020 was a tough year for national pension systems. But how did the UK fare?

The UK pension system

Out of the 39 countries included in the Pension Index report, the UK finished fifteenth. The UK’s overall score improved slightly from 2019 and does score highly in the ‘integrity’ category, highlighting trust in the system.

During a difficult year for pensions, the government’s Job Retention Scheme guaranteed employer contributions for furloughed workers. And yet, research from Employee Benefits found that 16% of employees reduced their pension contributions during 2020, while 7% stopped altogether.

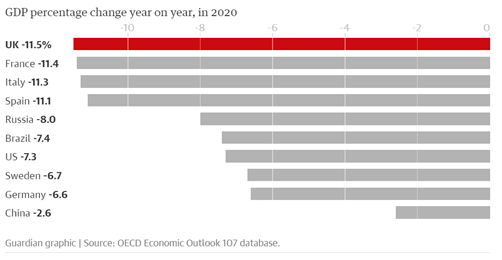

Back in June, the Organisation for Economic Cooperation and Development were predicting the UK’s fall in GDP would outstrip that of all other countries in the developed world.

Source: Guardian

By October 2020, the projected loss for the UK had fallen to 10.1% but the effect of the pandemic on the economy at least partly accounts for the UK’s low score in the ‘sustainability’ category of the pension index, indicating a system’s ability to provide benefits into the future.

What the Index means for your clients

The index is one measure of the UK pension system’s adequacy and sustainability. It considers policy and governance issues, as well as economic factors, outside of your client’s control.

What your clients can do is focus on the areas where they can influence their future retirement. Boolers can help, directing your clients to the best ways to make the most of their disposable income, and helping to build realistic and sustainable retirement plans.

Here are three ways for your clients to enhance their retirement fund.

1. Maximise contributions

Maximising pension contributions early gives your clients the best chance of reaching their retirement goals.

Pension contributions are liable for tax relief up to the Annual Allowance so clients should make full use of this if they can afford to. For 2020/21, the amount an individual can contribute and still benefit from tax relief is £40,000 (or 100% of pensionable earnings).

It’s also important your clients make the most of auto-enrolment. A 5% monthly contribution (with 3% added by the employer) is a great way to build a retirement fund. And your clients can increase their contribution too, if they can afford it.

2. Make the most of other allowances

Your clients might plan to use other savings and investments to part-fund their retirement. This might include savings or ISAs.

Like pensions, ISAs are also tax efficient. Interest made on a Cash ISA is tax-free and investment gains in a Stocks and Shares ISA are free of Income Tax and Capital Gains Tax (CGT). The current ISA allowance is £20,000.

Making the most of this allowance, if it is affordable, can supplement a client’s pension income in retirement.

3. Factor in the State Pension

To receive the full State Pension, an individual needs 35 ‘qualifying years’ on their National Insurance record. An individual with less than ten years will not receive a State Pension at all.

For the 2020/21 tax year, the full State Pension is £175.20 per week, or £9,110.40 annually. This is rising to £179.60 per week, or £9,339.20 annually in 2021/22. The amount received will vary for those with qualifying years between ten and 35.

Although the State Pension is unlikely to be the only pension your clients receive in retirement, it can be a solid foundation from which to build a financial plan, especially when a workplace pension and other investments are factored in.

Get in touch

The Mercer CFA Institute Global report highlights the integrity of the UK pensions system, as well as making clear the impact of the coronavirus pandemic.

For those saving for retirement, the advice remains the same. Stay patient, stay calm, and stay invested. Maximising tax-efficient pension contributions now is the best way for your clients to achieve their long-term financial goals and to live their desired lifestyle in retirement.

If you have clients who would benefit from help in managing their financial plan, please get in touch with us. Email enquiries@boolers.co.uk or call 0116 2407070.

Please note

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Levels, bases of and reliefs from taxation may be subject to change and their value depends on the individual circumstances of the investor.

Workplace pensions are regulated by The Pension Regulator