Chris Ball

Reveal Menu

How financial advice could help your self-employed clients realise their dream retirement

We all aspire to our own version of a dream retirement. And yet the road to an ideal future beyond work isn’t always smooth. This could be especially true for your self-employed clients.

Pension participation rates among this group are on average much lower. So too, are the size of their pension pots.

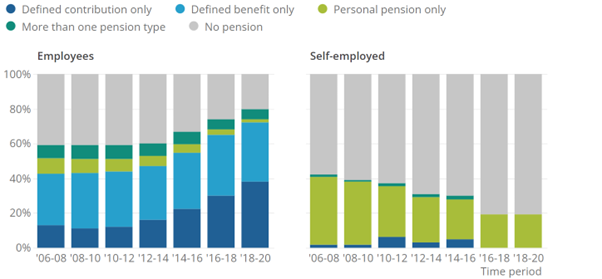

Auto-enrolment take-up has significantly increased the pension provision of employees, with 80% paying into a pension between April 2018 and March 2020. Just 20% of the self-employed did likewise over the same period.

Your self-employed clients will be accumulating wealth, possibly through ISAs or other savings and investment vehicles. But with financial advice – specifically around pensions – they might find that their dream retirement becomes more readily attainable.

Keep reading to find out how Boolers can help.

Understanding the need for pension saving

In June, the Office for National Statistics (ONS) released a report on the retirement savings of UK adults.

The following graph shows the percentage of people aged 16 to State Pension Age who contributed to different types of pensions between July 2006 and March 2020.

Source: ONS

The stark difference, in terms of the range of plans held and the numbers holding them, inevitably leads to a difference in pension pot size.

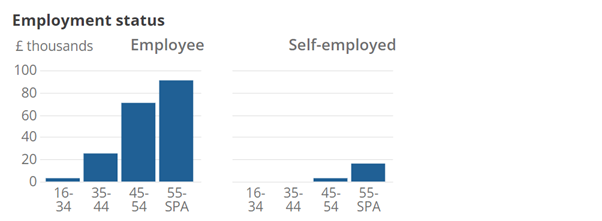

The ONS went on to look at the median pot size of different groups.

Source: ONS

The relative size of pension pots between the employed and the self-employed is marked. While employees over 55 hold average pots of around £90,000, the self-employed in the same age group hold less than £10,000.

But what is preventing your self-employed clients from taking out a pension?

The (limited) success of auto-enrolment

The Association of British Insurers (ABI) recently reported that auto-enrolment has been “an enormous success… bringing over 10 million more people into workplace pension schemes”.

This is a huge achievement, and yet, the same level of success has not been apparent among the self-employed. There are two main reasons for this:

Arguably, a proportion of auto-enrolment’s success comes from an inbuilt acknowledgement of employee inertia. By automatically enrolling employees and requiring them to opt-out, numbers are likely higher than if an opt-in was required.

With no one to enrol them automatically, your self-employed clients might simply have failed to set up a pension, despite planning to in the future.

Another stumbling block for the self-employed is that fluctuating income makes committing to a fixed contribution each month unfeasible.

In a 2017 review, the Department for Work and Pensions (DWP) acknowledged the limitations of the current auto-enrolment scheme for self-employed workers. The report stated that “there are 4.8 million self-employed people in the UK for whom a single saving initiative is unlikely to work”.

The report promises to test new approaches to improve participation and retirement outcomes for the self-employed.

Educating your clients on the advantages of pension saving

Pensions have several advantages that our Boolers experts can help your clients to understand. These include:

Funds held in a pension fund are invested and so have the chance of investment growth – albeit with risk attached – while benefiting from the effects of compounding.

A 2017 study by the Pensions Policy Institute found that the self-employed have, on average, overall wealth equivalent to their employed peers, but the wealth is held in different areas.

Of the survey respondents, 50% confirmed that they were saving into an instant access account, while 37% held a Cash ISA. It is important to note that these holdings were not necessarily intended for use in retirement.

While this data is now five years old, the current economic climate makes the findings worrying.

With inflation soaring and interest rates lagging significantly behind, money your clients hold in cash is effectively losing value in real terms.

When your clients contribute to a pension, they receive tax relief at the basic rate. A £100 increase to their pension pot will effectively cost them just £80.

For higher- and additional-rate taxpayers the level of relief is even higher. Using their self-assessment tax return, your self-employed clients can claim an additional 20% and 25% respectively.

When the government launches the Making Tax Digital scheme for the self-employed in April 2024, it is expected to make the taxation process more effective, more efficient, and easier for taxpayers. As the scheme is promoted, this might provide the nudge toward tax-efficient pension savings that your clients need. But why wait until then?

As well as tax relief on contributions, tax-free cash is available on withdrawals, usually up to a maximum of 25% of the pot value for defined contributions (DC) schemes.

Pensions also receive favourable Inheritance Tax (IHT) treatment on death in some circumstances.

Current legislation allows unused pensions to be passed on tax-free on death before age 75. If death occurs after age 75, a chosen beneficiary can still receive the unused pension amount, but they will pay tax on it at their marginal rate.

Be aware that your client must confirm the chosen beneficiary through their pension provider, rather than via a will.

Get in touch

Pensions are a great way for your self-employed clients to build wealth, helping to provide them with their desired lifestyle post-work.

If you have self-employed clients who would benefit from pension advice, including putting a long-term retirement plan in place, please get in touch. Email enquiries@boolers.co.uk or call 0116 240 7070.

Please note

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Levels, bases of and reliefs from taxation may be subject to change and their value depends on the individual circumstances of the investor.

Workplace pensions are regulated by The Pension Regulator.