Simon Watts

Reveal Menu

How slow-falling inflation and a rising base rate could damage your finances

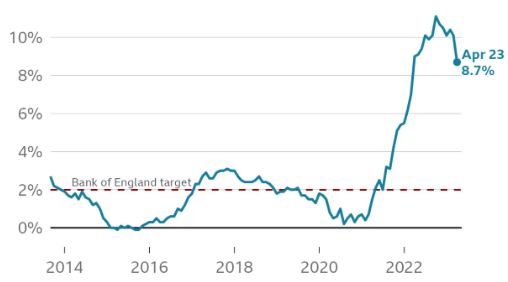

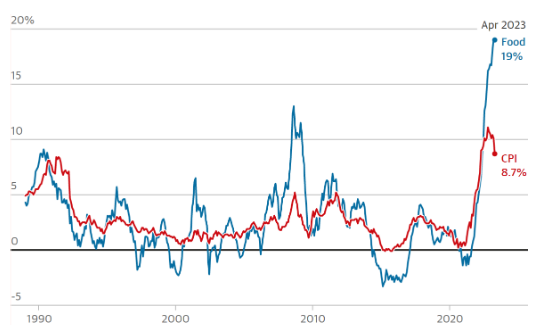

The latest figures from the Office for National Statistics (ONS) confirm that UK inflation is falling. From a 41-year peak of 11.1% in October 2022, the Consumer Prices Index (CPI) for the year to April 2023 fell to 8.7%.

But food inflation and energy costs remain high, and the UK is still experiencing higher inflation than much of the rest of Europe.

With inflation falling slower than anticipated, the Bank of England (BoE) recently announced that it had increased its base rate for the 12th consecutive time since December 2021. It now stands at 4.5%.

High inflation and the rising base rate are linked and both could affect your day-to-day budgeting as well as your financial plans.

Keep reading to find out what the two figures mean for you.

Inflation is falling slowly but it remains high

Inflation has been rising across Europe since coronavirus lockdowns ended in 2021. Consumers keen to spend their “accidental” lockdown savings rushed out to buy, while sellers – caught off guard – struggled to keep up.

Source: BBC

The issue was exacerbated by a global supply chain crisis and then the war in Ukraine, which caused already high fuel and energy prices to skyrocket.

In the UK, the further effects of Brexit may well have played a part in keeping inflation high.

Supply chain issues, worker shortages, and increased costs have all helped to see food inflation, in particular, soar.

Source: The Guardian

According to Reuters, UK inflation is currently at the joint highest level among the larger advanced economies, alongside Italy.

And, as we have seen already, while the CPI is falling, it is doing so more slowly than predicted. In its latest Monetary Policy Committee (MPC) report, the Bank of England (BoE) confirms that it expects inflation to return to its own 2% target sometime in late 2024.

The BoE’s base rate rise is intended to combat inflation

The main tool the BoE uses to control inflation is its base rate of interest.

Higher interest rates make it more expensive to borrow money and so saving becomes more attractive. A population that is saving is also spending less, reducing demand for goods and services. It is hoped that this will, ultimately, lower inflation.

At its latest MPC meeting, the BoE opted to raise its base rate of interest for the 12th time in a row. From just 0.1% in December 2021, the base rate now stands at 4.5%.

The increase to the base rate means that you will likely face higher borrowing costs, but you might also see your savings rates improve.

With inflation remaining high, though, it’s important to remember that the buying power of your savings is reduced. Your money could still be losing value in real terms.

Your robust financial plan can withstand economic changes

There are several factors you need to consider in the current climate of high interest rates and high inflation.

Managing your emergency fund

Rising interest rates are intended to encourage saving, so now is a great time to check in with your emergency fund.

Ideally, you’d have at least three to six months of household expenditure put aside in an easy access account, to use if the unexpected strikes.

Remember to factor in the reduced buying power of your cash savings due to inflation and top-up your rainy day fund if you need to.

Weighing up saving v investing

The current interest rate on your savings account is likely to be less than inflation, meaning your cash savings are effectively losing real terms value.

For this reason, be sure to hold just enough in your rainy day fund, but not too much.

If you have excess cash, adding it to an existing investment portfolio (via an ISA or a general investment account) or contributing to your pension could be a good way to combat high inflation and see real returns.

Of course, you’ll need to be clear about your long-term investment goal and be sure the choices you make align with your risk profile and capacity for loss. Inherent investment risk means that the value of your wealth could go down as well as up.

Staying focused on your goals

Global social and political events can have a short-term impact on world markets. Economies worldwide are still recovering from the effects of the pandemic, while the war in Ukraine has led to further uncertainty.

UK inflation is expected to fall sharply during the rest of 2023 but remember that this doesn’t mean prices will fall, just that they will begin to rise more slowly.

Keeping on top of your household budget is important but be sure to focus on your long-term goals too. Remember, your financial plan is a long-term proposition so if your goals haven’t changed, your plan doesn’t need to either.

Get in touch

If you would like to discuss the effects of the current economic climate on your long-term financial plans, please contact us today.

Please note

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.