Caroline Athey

Reveal Menu

How to bridge the menopause retirement gap in your business

A recent report has taken a fresh look at the gender retirement gap and found that the effects of menopause are largely overlooked. The subject can even be taboo, with more than two-thirds of women not speaking to colleagues about it.

Menopausal symptoms can be so severe that women leave employment earlier than planned, with a huge impact on their retirement savings.

Alongside wage inequality and work pattern disparities, menopause is a hugely important factor to consider, whether you are planning your retirement or looking to support employees within your business.

Keep reading to discover more about the menopause retirement gap and how financial advice can help make up a pension shortfall.

Menopause could cost some women more than £126,000 in lost retirement savings

The Royal London report found that symptoms of menopause are leaving women much more likely than men to reduce working hours in their 50s.

By this stage in a career, you could be earning the highest salary you’ll ever earn. For this reason, it is during this decade that pension saving usually peaks. Reducing hours could be costing women £63,000 compared to their male counterparts who remain in full-time work.

When menopausal symptoms are severe, it can force women to quit work entirely. Royal London suggests that this is the case for around 1 million women.

The effect of finishing work early due to menopause is partly responsible for a £126,000 shortfall in pension savings compared to male colleagues in the same position and who continue in employment.

Losing employees to menopause harms businesses so support is vital

Losing experienced members of staff is always bad news for a business.

Industry and company knowledge – possibly built up throughout a decades-long career – can’t be easily replicated. Training new staff to the same level of expertise, meanwhile, is expensive and time-consuming.

A disproportionate loss of women later in their careers can also lead to a loss of diversity in senior management roles and a disparity at executive levels.

Employees can take steps to support their staff, and it is vital that they do.

The report found that more than three-quarters (77%) of women experience “very difficult” symptoms, while more than two-thirds (69%) experience anxiety or depression. And yet the level of support received is worryingly low:

Menopause can still be taboo in some businesses. Of those surveyed:

Breaking this taboo, by encouraging an open workplace where these issues can be discussed is key to supporting staff at all levels and retaining those that are invaluable to a business.

The emotional wellbeing benefits are huge, as too are the financial ones, for the employer and employee.

Talking about the issues affecting women is crucial but increasing financial literacy is important too. This is where professional financial advice comes in.

Menopause is just one factor contributing to the gender retirement gap

While the gender retirement gap is closing, there are still issues that affect women’s ability to amass pension savings in line with their male counterparts.

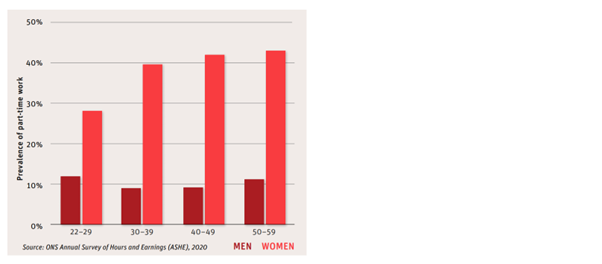

Back in 2021, Scottish Widows reported that women are much more likely to work part-time.

Source: Scottish Widows’ Women and Retirement Report 2021

This has an impact on salary, and so on the amount that is paid into a pension, but it can also leave women ineligible for auto-enrolment. While the average salary for a UK part-time worker is £7,000, the eligibility threshold for auto-enrolment is £10,000.

Another contributing factor is time spent out of work to start a family. Retirement contributions can suffer during maternity leave and on the return to work, possibly part-time. The continuance of “traditional” gender roles means that women are still more likely to be primary caregivers.

These factors are contributing to the gender pay gap that sees women earn 35% less on average. The median salary for a man is £31,400 compared to £20,500 for a woman.

Professional financial advice can help to close the gap

Retiring with adequate pension savings as a woman isn’t easy but a long-term financial plan can help.

Scottish Widows suggest that in the current system, a 25-year-old woman needs to save an extra £116 a month until she retires to achieve a pension fund comparable to that of a man at the same age.

A financial plan can help you understand your capacity for pension saving, helping you to align your contributions with the retirement you want.

Once you understand when and how you want to retire, we can put a plan in place to get you there, whatever obstacles you face during your career.

Get in touch

At Boolers, our team of financial experts is on hand to help build a financial plan that works for you. If you would like to discuss how a financial plan can help you to bridge the gender retirement gap, or you have questions on any other aspect of your long-term plans, please contact us today.

Please note

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Levels, bases of and reliefs from taxation may be subject to change and their value depends on the individual circumstances of the investor.

Workplace pensions are regulated by The Pension Regulator.