Chris Ball

Reveal Menu

How will the chancellor’s Lifetime Allowance freeze affect your clients’ retirement fund?

Back in March, the chancellor delivered his spring Budget and announced a freeze to the Lifetime Allowance (LTA).

As part of the government’s attempt to claw back some of its coronavirus spending, the freeze will raise £990 million for the Treasury by 2025/26, according to government costings.

It could have a significant impact on your clients’ future contributions, the size of their pension pot at retirement, and lead to tax charges of up to 55% on funds exceeding the frozen allowance.

So, what is the LTA, what level has it been frozen at, and what effect could it have on your clients’ long-term retirement plans?

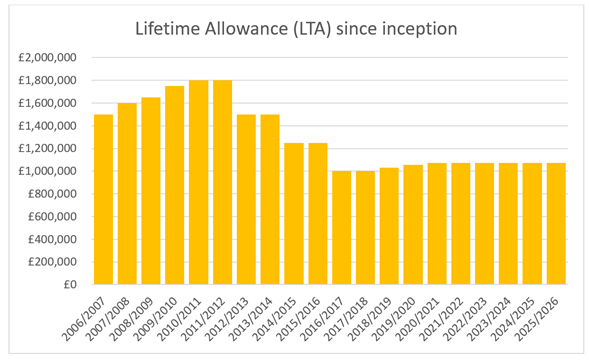

The LTA is a limit on pension withdrawals

The LTA is a limit on the amount that can be withdrawn from a pension fund without triggering an additional charge. It was introduced on 6 April 2006, known as “A-Day”, as part of wider pension simplification legislation.

Source: HMRC

The LTA began at £1,500,000 before rising to a peak of £1,800,000 between 2010 and 2012.

Since 2018, the LTA has risen in line with the consumer prices index (CPI). This would have seen the LTA reach £1,078,900 for the 2021/22 tax year. Instead, it has been frozen at £1,073,100 until at least 2026.

The charge for exceeding the LTA is 55% for any funds above the limit taken as a lump sum. Any excess amount taken as income triggers a 25% charge.

A test is carried out against the LTA every time a benefit crystallisation event (BCE) occurs. There are thirteen BCEs currently – including taking a lump sum via Pension Freedoms, moving defined contribution (DC) funds into drawdown, and reaching age 75 – but knowing whether a BCE has occurred can be difficult.

Speaking to us before a decision is made can help to ensure your clients don’t accidentally trigger a test against the LTA and find themselves liable for a charge.

The freeze could hit millions of pension savers

The government expects the £990 million of additional revenue to be raised in two ways. First, through LTA charges paid by those exceeding the frozen allowance. And second, through savings on tax relief as those approaching the threshold amount stop contributing to their pensions.

While £1 million might sound like a sizeable retirement pot, it could amount to a pension of only around £28,000 at retirement.

Figures from Canada Life suggest that a pension pot of £469,000 today could breach the LTA in 20 years, even if contributions are stopped now. This assumes an LTA frozen until 2026 and increasing annually by an average of 2% thereafter.

This means that even clients less than halfway to the LTA currently might need to start thinking about the effects of the freeze. If your clients continue contributing at 10% a year, Canada Life confirms that a pot of just £351,000 would exceed the LTA in 20 years.

Former pensions minister Steve Webb, speaking before the freeze was announced, said that while “at present, only a small number of people pay a tax charge when they exceed the lifetime allowance […] a long-term policy of freezing the limit could have implications for well over a million workers saving for retirement.”

Nathan Long, senior analyst at Hargreaves Lansdown, also confirmed that “this won’t just hit very high earners; committed and consistent pension savers risk running into the limit too and being punished for their efforts to save for the future.”

Boolers can help your clients mitigate the impact of an LTA charge

While the reason for the freeze is clear, a 55% charge on your clients’ hard-earned pension savings could seriously affect their plans.

It is important to remember that pensions are hugely tax-efficient. Stopping contributions might lower the possibility of an LTA charge, but the effects of compound growth – and the lack of Income Tax or Capital Gains Tax (CGT) while the pot is invested – might mean continuing to save is the best option.

Remember too that the 55% charge is only on the excess – the amount above the LTA limit at the time benefits are taken. It also only applies where the excess is taken as a lump sum. Clients taking the excess as income will see the charge immediately reduce to 25%.

Pension legislation can be difficult to navigate but we can look at your clients’ finances as a whole. Taking retirement earlier than planned, if affordable, might prevent the LTA charge from being triggered and some clients might opt not to take their pension at all. We can help your clients put a plan in place that works for them.

Get in touch

If you have clients who would benefit from help planning their retirement and understanding the impact of a potential LTA charge, please get in touch. Email enquiries@boolers.co.uk or call 0116 240 7070.

Please note

A pension is a long-term investment. The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Your pension income could also be affected by the interest rates at the time you take your benefits.