Gavin O’Neill

Reveal Menu

Investment Commentary: Monthly Bulletin April 2019

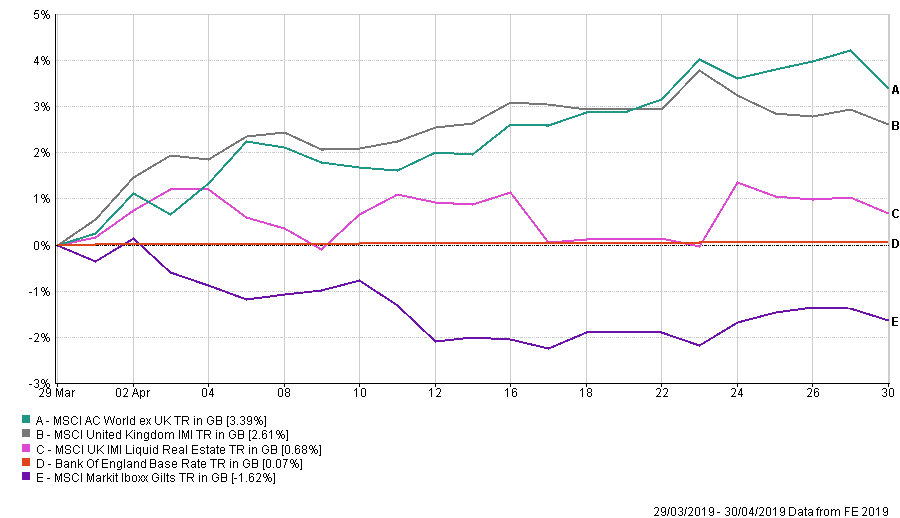

April has seen a continuation to the strong start to 2019 with equity markets recovering from the lows reached at the end of 2018. We have highlighted the performance of the main asset classes over the month in the chart below:

Source – Financial Express

All data based on bid to bid prices with income reinvested

The year to date so far has seen a general move upwards for global equity markets with a much more positive tone between US and Chinese trade negotiators. At the same time, the price of oil has continued to rise with the US confirming that it will end waivers on Iranian sanctions. This has benefited major oil companies, which within the UK in particular do make up a significant proportion of our main index (BP/Shell).

Portfolio Changes

At the beginning of the month, we made some changes across the board within our portfolios. Within the ‘alternatives’ sector, we have sold our holdings in the Henderson and Merian absolute return funds and reallocated these monies to mainly US equities for long term growth, combined with a (predominantly) fixed interest fund for Cautious and Balanced risk investors.

Performance

Whilst only a short-term period, it is pleasing to see that our portfolios have outperformed their respective benchmarks over the last 1 and 3 months. We would expect to see this given that we remain overweight towards UK and Global equities and consider that these will provide higher, more competitive returns over the longer term.

THE BOOLERS INVESTMENT COMMITTEE