Duncan Pickering

Reveal Menu

Investment Commentary: Monthly Bulletin August 2020

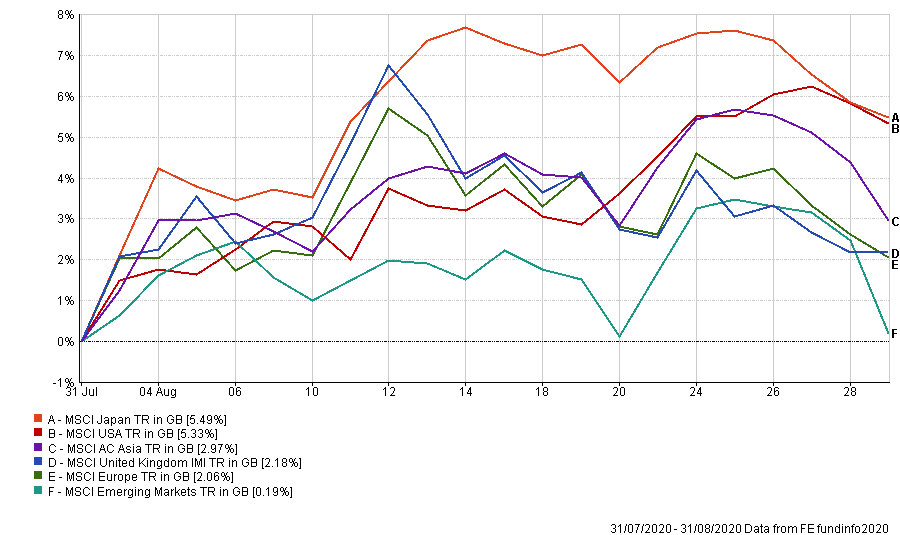

After a disappointing end to July markets trended higher through August with risk assets rebounding well. Performance of some of the main indices are highlighted below:

(All figures are based on bid to bid pricing with income reinvested, in Sterling terms)

On the health front, the Coronavirus pandemic has now passed 25 million cases worldwide, with over half of the new cases coming since the start of July. Whilst concerning, the increased transmission is undoubtedly part of a function of increased testing and also helps shine new light on mortality rates which suggest that new treatment protocols are working. Clearly there is still a very long way to go, not least until vaccines are readily available, but with lockdown restrictions becoming more flexible and targeted in their approach, there is hope that the economic damage from this point forward can at least be contained.

Across the pond, America’s Coronavirus relief bill continues to be debated whilst preparations for November’s election ramp up with bookmakers currently unable to split President Trump and Democrat candidate, Joe Biden. August saw the conclusion of a more positive earnings season in the States helping to stimulate markets, although the full effects were tempered for our investors as the Dollar continued its path of weakening.

In the UK, Q2 economic data release confirmed a 20% fall in q-o-q GDP. Whilst alarming, this in many ways was expected and indeed on a monthly basis, figures for May & June provided a more encouraging outlook moving forward. The next marker will come when schemes such as “Furlough” and “Eat out to Help Out” end, revealing any medium-term damage to the economy in the form redundancies and changes of individual behaviours – remembering the UK economy is over 70% consumer & services led.

Elsewhere through the month, European markets (buoyed by July’s €750bn Recovery fund) and Asian/Emerging Markets both consolidated the considerable gains they’d achieved through June and July. In Japan, stock markets performed strongly and led global returns, despite PM Shinzo Abe announcing his decision to step down on grounds of ill-health.

Our portfolios managed to capture more of the market gains this month thanks in-part to a rally in “Value” style stocks at the beginning of August. This outperformance now extends to three months versus benchmarks which has been pleasing to see after a period of weakness.

September sees the start of a new school year and with it the UK now moves to another crucial phase of re-opening. We hope to be able to report further positivity in next month’s bulletin. Until then, we would like to remind you that we remain readily available and at hand, should you wish to discuss anything more specific regarding your individual investments or the wider market environment more generally.

The Boolers Investment Committee