Gavin O’Neill

Reveal Menu

Investment Commentary: Monthly Bulletin February 2019

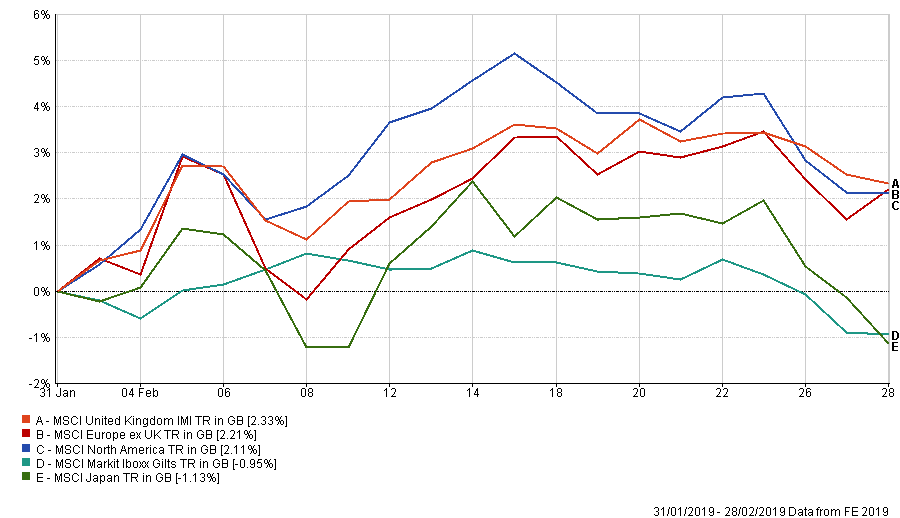

February proved to be another volatile month for markets, but ultimately one that saw further gains for the major global indices that built on the strong performance witnessed in January. Performance of some of those main Indices is highlighted below:

(All figures are based on bid to bid pricing with income reinvested, in Sterling terms)

Pleasingly there have been further signs of progress in the US/China trade saga as Donald Trump agreed to delay imposing the latest round of tariffs on the emerging powerhouse following a series of apparently productive meetings with his Chinese counterparts. This, along with more dovish tones from the Federal Reserve, really set the foundations for the overall improvement in global markets.

Closer to home, Brexit rumbled on without any further clarity in terms of an ultimate outcome. Theresa May remains hopeful she can get another iteration of her Withdrawal Agreement pushed through Parliament over the next couple of weeks but has opened the door to extending the process past March’s proposed deadline if this fails.

Underscoring all of the political noise, we continue to have economic growth figures which despite slowing, remain in positive territory for now and with earnings season well underway, corporates are still showing the strength that should help to support markets further.

Following the negative performance experienced in 2018, it has been pleasing to see our portfolios exhibiting a positive return over the first two months of 2019.

THE BOOLERS INVESTMENT COMMITTEE