Gavin O’Neill

Reveal Menu

Investment Commentary: Monthly Bulletin February 2020

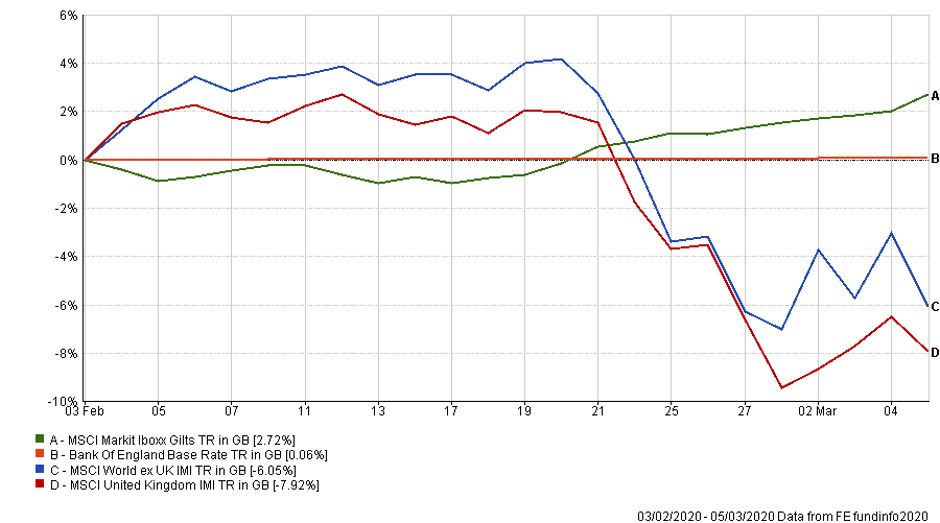

Since our January update was issued, global equity markets have experienced a significant downturn as can be seen from the chart below.

Up until the beginning of last week, equity investors appeared to have largely discounted the potential impact of Coronavirus (COVID-19), due principally to the belief that it would largely be restricted to China and one or two other Asian countries. Once this perception changed, share markets have been quick to react adversely as the information flow across all media channels has gone into overdrive. However, it remains the case that, at this stage, no-one knows exactly what the outcome will be.

Over the last week or so we have experienced very volatile trading days, with wild swings both up and down. The sharp movement in share prices has, at times, been indiscriminate across market capitalisations and as an example, the FTSE 100 may have a positive day whilst the broader market may be down. This applies across all global equity markets where the UK, Europe and the Far East may have a positive day, only for the US market to be subsequently down (possibly only in the latter trading hours when European markets are closed).

As one would expect given such share volatility, bond markets have largely been positive (as shown by the Gilt index movement above) and this endorses our approach of a well-diversified portfolio.

Boolers Investment Strategy

Our investment philosophy has always been to invest with a significant equity bias, this strategy being based on the fact that this asset class generally provides the greatest long term returns. This approach is unlikely to change, even in the short term.

We can trade tactically and indeed we have had numerous internal discussions re-examining our views and the potential to reduce some equity exposure. The problem is always just when to ‘go back in’ and it is against our natural human instincts (fear) of investing when prices are weak – just where will ‘the bottom’ be? Global equity markets have already fallen significantly from recent highs and therefore the market has already re-priced risk to a certain degree.

Some sectors, not just travel, have performed poorly and may suffer some more prolonged short term pain, but we fully expect that these will recover at some stage. Confidence must return, but in the meantime Central Banks have provided some stimulus and there is room for more, albeit there is less scope than in the past as interest rates are already very low. The US has already cut rates and is likely to do so again at some point. For the moment, we are taking encouragement from the latest news from China where the position already appears to be less threatening and markets have been much more resilient.

Coming back to our own strategy, given the recent falls we believe that equities certainly offer better relative value than bonds, with strong dividend yields on UK equity funds (4-5% pa, higher in some cases) comparing with Gilts and Corporate Bonds offering sub 2% pa. As we write, the current annual redemption yield on 10 year UK Gilts is less than ¼%. That means that such an investment will pay you a total annual return of less than ¼% for the next 10 years – this is both capital and income, will reduce by an income tax liability (if appropriate) and dealing costs.

In this scenario, equity investors are being compensated for taking on equity risk and should be rewarded in the longer term. Our portfolios are also maintaining a slight ‘value’ bias and again we believe that this remains an appropriate strategy despite the strong performance of ‘growth’ during 2019 and naturally does provide more defensive qualities.

To conclude, we have monitored market movements and will continue to do so, along with all news on COVID-19, but for now, we have taken the conscious decision of not making any significant changes to our long term asset allocations.

If you do feel that your attitude to risk has changed we can adapt your portfolio accordingly. For example, if you want to formally de-risk your portfolio this will most probably involve a reduction of your UK and Overseas equity exposure and some reallocation into bonds / gilts.

Please contact one of our Investment Team or your designated consultant to discuss this further, or indeed any concern you have regarding your invested assets.

The Boolers Investment Committee