Gavin O’Neill

Reveal Menu

Investment Commentary: Monthly Bulletin March 2019

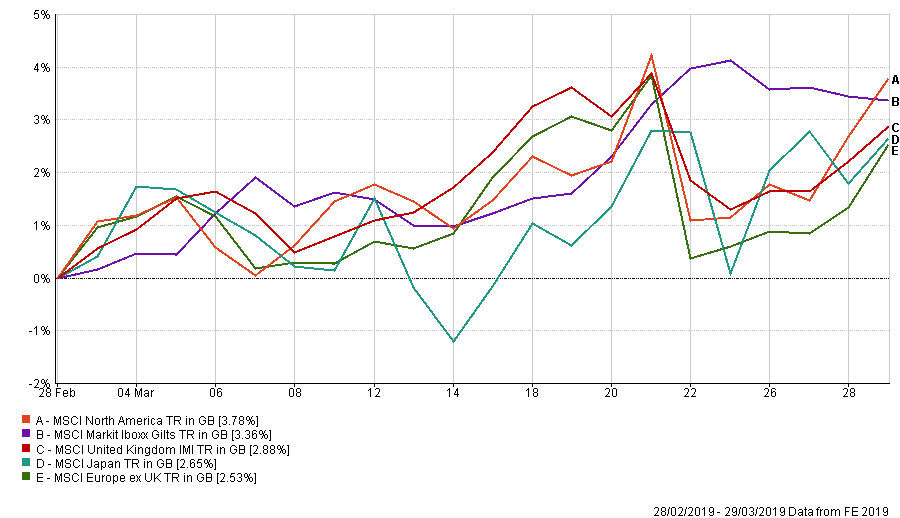

Markets once again posted positive returns through the month of March, capping a strong quarter for investors. Performance of some of the main indices is highlighted below:

(All figures are based on bid to bid pricing with income reinvested, in Sterling terms)

Much of the improvement can again be attributed to a reduction in concerns over some of the factors that drove markets down during the fourth quarter of last year. March has seen further, positive strides made in the US-China relationship as well as significantly more market friendly tones from the Federal Reserve in the States. Both of these should provide support to markets and the wider global economy.

Despite the overall gain, one area that hasn’t been so supportive is Brexit and markets sold off sharply intra-month after Theresa May requested to delay proceedings. March 29th – our proposed date for leaving the EU – has been and gone and focus now turns to getting a deal of sorts by Friday 12th – our current extension deadline. Political wrangling continues and each outcome remains as realistically possible as every other. That is with the exception of one, as Theresa May signalled her intent to quit her role as Prime Minister in the not too distant future. Britain and the European community wait with baited breath for the next development in this on-going saga.

We are mindful of the ever-changing backdrop but for now our preference for Equity remains and pleasingly this allowed our models to track the fortunes of markets, producing a positive return for the month and ensuring a successful quarter for investors.

THE BOOLERS INVESTMENT COMMITTEE