Gavin O’Neill

Reveal Menu

Investment Commentary: Monthly Bulletin November 2018

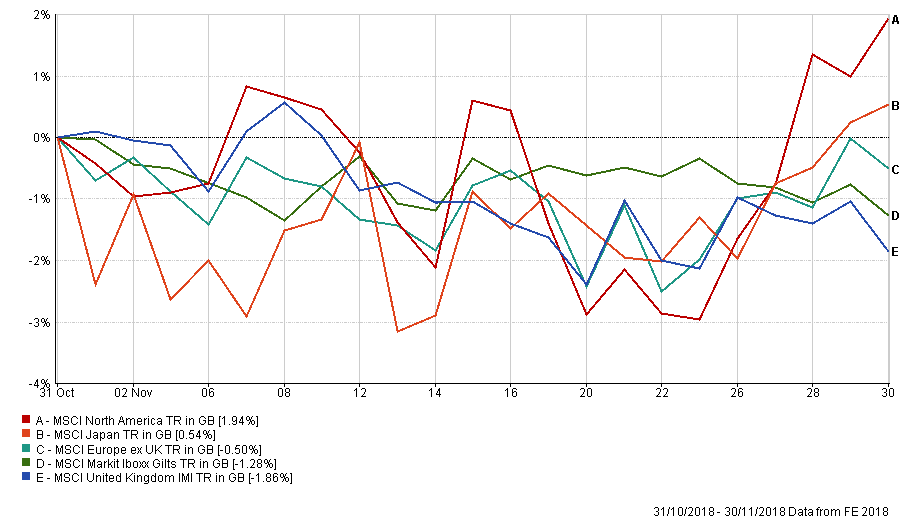

Markets consolidated their levels in November after a painful period that’s now being dubbed “Red October”. They remained range-bound throughout the month, albeit it with increased levels of volatility and significant daily moves. We have highlighted below the movement of the main developed markets over the month.

(All figures are based on bid to bid pricing with income reinvested, in Sterling terms)

We are still no clearer on the final outcome of Brexit and this continues to be a headwind for our own equity market, as the above chart reflects. November saw the “Withdrawal Agreement” ratified in both European Parliament as well as by Teresa May’s own Cabinet but the next challenge, of getting it passed through Parliament at the December 11th vote seems a much harder task. Speculation remains on both the agreement and her own position within the Conservative party and it’s likely to be another stormy couple of months in UK politics.

Elsewhere, the China/United States trade dispute remained a hot topic for investors but despite these concerns, the global economic backdrop remains resilient for markets. The price of Oil continued its decline with Brent Crude dropping to $60 per barrel – and this should help support activity further.

It is pleasing to see that all of our portfolios outperformed their respective benchmarks during November.

Index Data

Regular readers may have noticed the indices quoted in the above chart have changed from last month’s commentary and we now have access to the full range of global indices provided by MSCI. The indices are used as a way of depicting performance and are only ever designed as a guide. Therefore, whilst not as recognisable as the previously quoted indices, the new MSCI range remain equally as relevant as before and reflect the underlying companies within these regions.

THE BOOLERS INVESTMENT COMMITTEE