Duncan Pickering

Reveal Menu

Investment Commentary: Monthly Bulletin October 2019

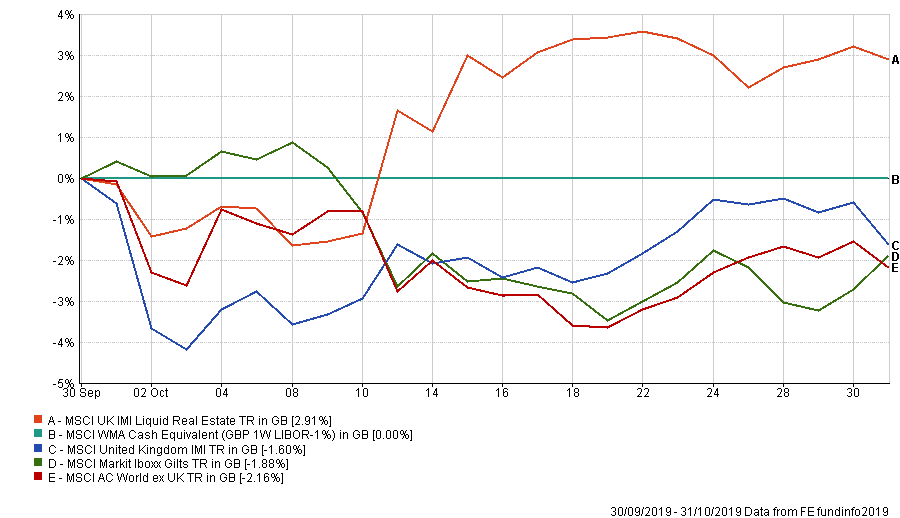

October has been a mixed month for markets with the UK ending lower and for domestic investors, a strengthening Sterling negating the gains made in Global markets. Performance of some of the main asset classes are highlighted below.

(All figures are based on bid to bid pricing with income reinvested, in Sterling terms)

In terms of what has been driving markets nothing too much has changed over the course of the month, in a light month of US/China trade news flow. The effects of the on-going saga are now firmly showing signs of impacting the global economy though and this has forced the Federal Reserve into cutting interest rates for the third time in four months to provide support.

Closer to home, October 31st came and went and we now move into General Election territory – scheduled for 12th December – causing further delay and uncertainty. The one positive has been Sterling’s reaction to the now reduced threat of a ‘No Deal’, as it gained 5% versus the Dollar. This has been beneficial to domestically focused stocks – of which we have an overweight exposure to – with Mid Cap stocks performing strongest over the month.

Overall, our portfolios fell slightly during the month, following markets lower, although pleasingly we managed to protect capital better and ended above benchmark across the range.

THE BOOLERS INVESTMENT COMMITTEE