Duncan Pickering

Reveal Menu

Market Commentary – Breaking News: The War in Iran

Key Points

Breaking News: The War in Iran

Over the weekend, the US and Israel have mounted a military campaign against the Iranian regime. This has triggered a sharp, immediate shift into risk‑off positioning, with markets pricing in fears of wider regional escalation and potential disruption to the Strait of Hormuz, a chokepoint for up to 20 million barrels of oil per day. Oil prices have spiked materially, driving expectations of a short‑term inflation bump and higher volatility across global assets. Safe‑haven flows have pushed gold higher, while equities, particularly in oil‑importing regions have weakened as investors reassess growth risks. Analysts note that while the conflict is more intense than recent flare‑ups, it is still expected to be short‑lived, limiting the likelihood of a structural stagflation shift. Overall, markets are reacting in a textbook geopolitical pattern: higher oil and gold, weaker equities, and heightened volatility, but with the expectation that extreme moves may fade if disruption remains contained to weeks rather than months.

Given the events over the weekend, we have sold 1.5% of the iShares S&P 500 in Cautious and Balanced Funds and reinvested the proceeds by allocating 0.5% each into Premier Miton Strategic Monthly Income focused on quality short‑duration bonds, VanEck S&P Global Mining to increase exposure to precious metals miners, and Jupiter Absolute Return for added tactical protection within the portfolios.

We are monitoring events as they unfold and will manage portfolios both tactically in the short term, if deemed appropriate, and strategically based on our medium-term views.

Our normal monthly market commentary for February is detailed below.

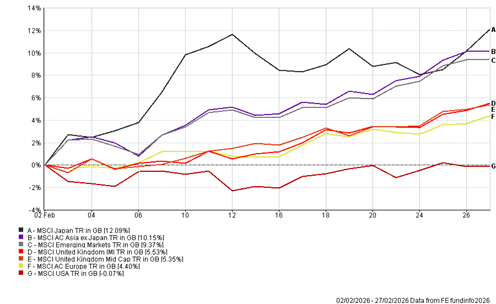

Markets – Equity Leadership Outside the US

Global equities extended January’s broadening leadership beyond the United States in February. Japan led gains as the Nikkei 225 surged by roughly 10% on continued strength across the semiconductor supply chain and governance tailwinds, while Europe and the UK posted solid gains, with the Euro Stoxx 50 up about 3.6% and the FTSE 100 nearly 5.7%, approaching 11,000. By contrast, the S&P 500 edged lower by about half a percent as investors digested tariff headlines and a patient Federal Reserve.

(All figures are based on bid‑bid prices with income reinvested unless otherwise stated.)

Equity leadership has shifted outside the US because several international markets are delivering stronger performance, supported by distinct macro and structural drivers. A macro‑economic backdrop of higher rates and inflation has favored value stocks over quality/growth stocks, while a weaker dollar and uncertainty around trade policy have led international investors to rethink their overallocation to the US.

Valuations are also more attractive abroad, as US equities still trade at elevated multiples, whereas developed ex‑US and emerging markets offer more moderate pricing, prompting a rotation into cheaper, higher quality opportunities. Diverging monetary policy reinforces this trend, while the Fed remains on hold, several non-US central banks from the BoE to Korea and Brazil are closer to, or already, easing, improving funding conditions and supporting earnings outside the US.

Stronger earnings growth momentum across Asia and Latin America, combined with structural themes such as European fiscal support, and shareholder reform cycles in Japan, further underpin non-US leadership. History suggests such leadership cycles are normal, often following long periods of US outperformance, with conditions now firmly in place.

Court in Session, Tariffs in Recession

The Supreme Court’s decision to strike down Trump’s tariffs imposed under the International Emergency Economic Powers Act carries significant implications for markets. In the near term, markets may experience volatility as investors digest the ruling and evaluate the transition to alternative tariff mechanisms. Although the ruling invalidates the legal basis for sweeping emergency tariffs, many duties under other statutes remain in place, and the Trump administration has already moved to restore broad tariffs, initially at 10–15%. This means the effective tariff burden declines only modestly, limiting immediate economic relief.

However, the removal of emergency tariff powers reduces the scope for rapid, unpredictable tariff shocks, which is broadly positive for risk sentiment. Lower prospective import costs imply mild disinflation, supporting consumer real incomes and helping moderate interest rate expectations. Historically, global equities often rebound when tariff pressures ease, particularly in sectors relying on imported inputs (retail, autos, capital goods, semiconductors) and in export heavy markets abroad.

A key uncertainty lies in potential refund liabilities, estimated at up to $175 billion, which could lead to lengthy litigation and uneven corporate outcomes. Overall, while the ruling does not eliminate tariffs, it signals a shift toward slower, more procedurally constrained trade policy, improving global risk appetite, and slightly easing inflation pressures.

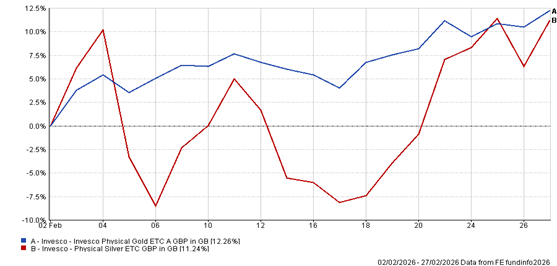

Precious Metals Bounce Back

Gold set fresh record highs near $5,200/oz into month end as investors sought portfolio insurance, with silver outperforming over the month. Precious metals rebounded in February primarily because the late‑January sell off created deeply oversold conditions, triggering bargain‑hunting, short‑covering, and renewed physical and investment demand.

Dip buyers, both institutional and retail, stepped back in at these lower price levels, viewing them as attractive entry points amid unchanged long‑term fundamentals, including persistent geopolitical uncertainty, fiscal‑dominance concerns, and robust central bank demand. Physical buying also strengthened, with renewed interest in bullion and ETFs after the correction. Silver’s inherently higher volatility amplified both the downside and the subsequent recovery, driving sharper percentage rebounds.

(All figures are based on bid‑bid prices with income reinvested unless otherwise stated.)

Portfolio Changes

Earlier in the month, we sold our position in the Natixis Long/Short Equity Growth Fund due to its focus on semiconductor shorts that have not performed as expected. We reinvested the proceeds into Jupiter Absolute Return to increase exposure to a pure play tactical protection strategy for Adventurous clients, mirroring positioning used in Cautious and Balanced portfolios.

BOOLERS INVESTMENT COMMITTEE