Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin April 2022

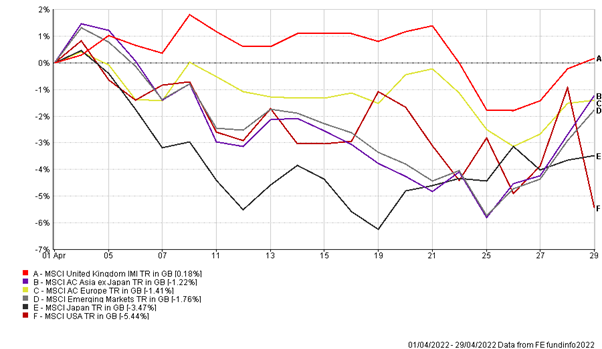

Overall markets were negative for the month of April, as investors became more concerned that higher inflation and tighter monetary policy may dampen down economic growth prospects for the year. The performance of the main indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

The latest minutes from the US Federal Reserve highlighted that Fed officials were willing to increase rates aggressively to take control of inflation expectations. It was pointed out that several participants would have advocated for a 0.5% rate rise during the March meeting, if it hadn’t been for Russia’s illegal invasion of Ukraine and that most of the policy makers stated that at least a 0.5% increase would be appropriate for later in the year.

This is as preliminary estimates of first quarter US GDP showed the economy contracted unexpectedly in the first three months of the year by -1.4% due a rising trade deficit because of higher import prices and volumes rather than a weak US consumer, as personal consumption grew by 2.7%. This also comes at the back of annual US inflation hitting 8.5% for the month of March, the fastest pace since 1981, as the cost of food and energy surged. The minutes also showed that fed officials had started up drawing plans to reduce its assets from the Fed’s balance sheet at much faster pace than in their previous efforts in 2017, with Fed officials hinting that the Federal Reserve could begin reducing it’s $9 trillion balance sheet from early as May.

In the UK, the annual inflation rate hit 7% in March, the highest reading in 30 years, after major increases in the price of petrol, reflecting the surge in global energy prices after the invasion of Ukraine. The sustained increase in prices puts further pressure on the Bank of England to increase interest rates at a faster pace, even as growth is expected to slowdown this year. The latest data showed retail sales in March fell 7.9% compared to the previous month, with online sales falling the most. The Bank of England have already increased its main rate three times since December 2021 from a historic low of 0.1% to 0.75% and a further rate increase is likely at the May meeting, however the question remains by how much the increase will be.

Despite data showing China’s economy grew at a faster rate than expected in the first quarter of this year, recent events have shown a general weakening in the economy, as the reintroduction of lockdowns in major regions such as Shanghai and Shenzhen in the pursuit of a strict covid zero policy have caused consumer spending and industrial production to fall. In response to the slowdown of the Chinese economy, the central bank cut the reserve requirement ratio for banks by 0.25%, to help inject liquidity to its financial system and introduced incentives to encourage major financial institutions to provide financial services to industries most negatively impacted by the pandemic.

During this volatile period in markets, we continue to manage our portfolios with the belief that equity-based investing remains appropriate over the medium to long-term and investors who are patient and adopt such an approach, will ultimately be rewarded. We of course monitor markets closely and will take any appropriate action we deem necessary to adapt to the continuously changing macro-economic and geo-political environment.

If you have any queries regarding your portfolio, please do not hesitate to contact your investment manager.

The Boolers Investment Committee