Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin April 2023

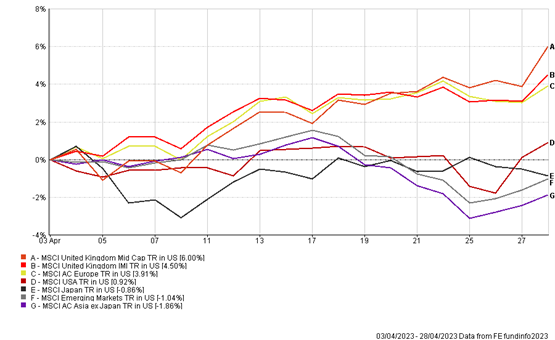

Markets were overall mixed in the month of April, as global inflation continued to remain sticky, and companies began reporting their earnings for the first quarter of 2023. The performance of the main indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

Global earnings by and large have been resilient, with positive surprises coming from companies such as LVMH, Coca-Cola, Alphabet, Meta and Microsoft, where these companies have pricing power, brand loyalty and strong market share. This shows that aggregate demand in the global economy remains strong, with a concentration of solid demand for companies in the service sector. The better-than-expected earnings season so far demonstrates that the expectation by economists of a recession in the second half of this year is not a done deal and that central bankers may be able to sustainably bring inflation down without causing a contraction in output growth in the real economy.

The US Federal Reserve released minutes of their latest meeting in March which showed that despite the recent banking fall out, that Fed are still primarily focused on reducing price pressures in the economy. Latest figures showed that the US consumer price index year over year (YoY) fell from 6% in the previous month in February to 5% and core inflation which excludes volatile items such as food and energy increased by 5.6% YoY, following a 0.4% monthly jump indicating that goods and services price pressures remain high.

The minutes also revealed that a few fed officials considered ‘pausing’ interest rate increases, stating it would give them a chance to assess the impact of banking turmoil on the financial system and economy, with a mild recession being mentioned for the first time as a likely possibility in the second half of the year and a recovery over the next two years. Based on the recent minutes and latest inflation figures, economists are forecasting that we will see another 0.25% increase in the federal funds rate at the Fed’s May meeting, which would push US interest rates to 5.00 – 5.25%.

UK inflation continues to remain stubbornly high, with latest readings showing UK annual consumer prices at 10.1%, which was lower than the previous month’s figure of 10.4% and core inflation excluding food and energy remained unchanged at 6.2% YoY. Most of the price increases were from sharp rises in the costs of food which were up 19% YoY in March and recreation such as concerts and sporting events, although motor fuel costs continued to decline to offset some price rises.

With recent labour figures showing wage growth continuing to be persistent and core service inflation continuing to be sticky, markets are now pricing in that the Bank of England (BoE) are likely to increase interest rates at their May meeting by 0.25% to 4.5% to help dampen down demand in the UK economy.

China’s economy grew by 4.5% YoY in the first quarter of this year, as the growth in exports, infrastructure investment and a rebound in consumption and property sector helped the Chinese recovery. However, despite the stronger than expected growth, Asian-pacific equities underperformed, as investors doubted whether China can sustain its growth rate and concerns that the concentration in growth may be limited retail consumption and exports rather than a broad-based recovery. Furthermore, strong economic growth indicates that less stimulus is needed to support the economy, which has a negative impact on share prices, where markets had originally priced in a rate cut. In their latest meeting, the People’s Bank of China (PBoC) left interest rates unchanged at 3.65% and announced that credit supply will continue to remain robust but unlikely to increase.

Despite the continued volatility within financial markets, portfolios across the board posted very slight positive returns for April and added to the positive start we have experienced year to date. Our formal quarterly valuation reports (for the quarter ending 31st March) are currently being printed and will be issued out shortly.

THE BOOLERS INVESTMENT COMMITTEE