Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin April 2025

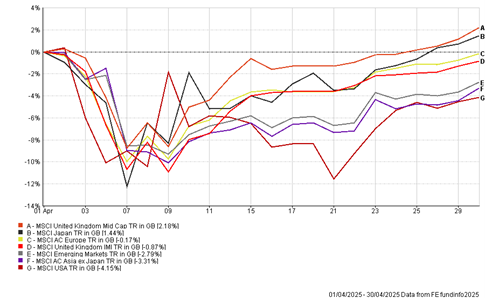

Global equity markets had a difficult start to April but rebounded strongly after the initial fallout from Trump’s Trade War on the rest of the world. The performances of the main equity indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

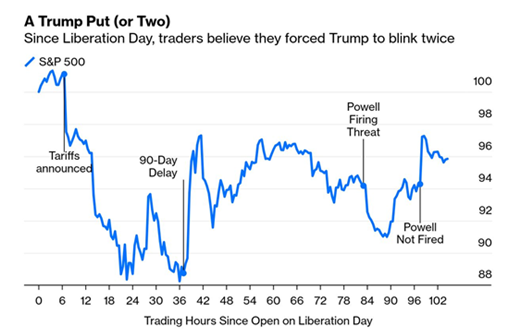

The Trump Put

Since ‘Liberation Day’ on the 2nd April, US equity markets have recovered much of their ground they initially lost. Much of the recovery has been attributed to Trump issuing a ’90 day pause’ on his reciprocal tariffs, so countries can come to the negotiating table. In addition, Trump removed his initial threats with regards to firing the Federal Reserve Chairman Jerome Powell for not lowering interest rates.

It is hard to decipher which countries have approached the US regarding trade negotiations with speculation that deals with India, South Korea and Japan could be completed soon. However, the most important trade negotiation will be with China given the tariff rate is currently at 145% on US import duties. For the time being, China is denying that any talks are taking place with the Trump administration.

With nothing confirmed, all this speculation has led to uncertainty for consumers, business and investors which is likely to dampen economic growth. For the moment, markets are giving Trump the benefit of doubt that he will in fact get trade deals done in principle for the US without any further escalation.

Source: Bloomberg

Where do Equity Markets Go from Here?

Analysts have been downgrading their expectations for earnings this year at a dramatic pace but expectations for earnings in subsequent years remain quite high on the hope that we will get a rollback on tariffs and tax cuts to offset the detrimental effect on earnings.

In an era of heightened uncertainty one lesson from the pandemic is that equity investors are prepared to look through a drop in earnings if they can see a subsequent rebound. In the pandemic there was an external shock that was met with unprecedented monetary and fiscal stimulus to more than offset the impact of a fall in household incomes and corporate profit.

By contrast today, the current trade war has been self-inflicted and unlikely to be offset by outsized policy stimulus in the US. However, falling inflation does give central banks in Europe a green light to cut interest rates and fiscal policy stimulus is likely in both Europe and China but policy stimulus on the scale of the pandemic is unlikely.

Therefore, the bull case for equities then rests on the hopes that trump is sufficiently scolded by the immediate market reaction to his reciprocal tariffs, and he has no option but to capitulate and give the market what it wants through strategic tariffs targeted in the right sectors like technology and healthcare that benefit the US economy, not hold it back.

THE BOOLERS INVESTMENT COMMITTEE