Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin April 2026

Key Points

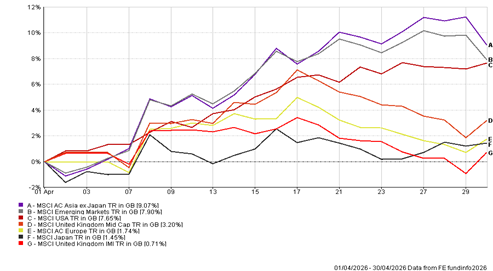

After the market falls we experienced in March, April has provided a much-welcomed turnaround, as highlighted in the indices chart below.

(All figures are based on bid‑bid prices with income reinvested unless otherwise stated)

Company Profits Give World Markets a Much-Needed Lift

April marked the start of the quarterly period when the world’s largest companies report how much money they have been making, and for the most part the news was better than expected. In the United States, where many of the world’s biggest businesses are listed, many companies reporting in April delivered results that beat what analysts had forecast, even against the backdrop of higher oil prices and the uncertainty caused by the ongoing conflict in Iran.

Some of the standout results came from large technology companies, with search and advertising giant Alphabet (the owner of Google) jumping 10% on the day of its results after reporting strong revenues and announcing plans to invest up to $190 billion in its technology infrastructure this year. Industrial giant Caterpillar, seen by many as a barometer for the health of the global economy, also surged by almost 10% after raising its outlook for the year, driven by booming construction demand linked to artificial intelligence data centres. The encouraging results helped the S&P 500, the main measure of US company shares, close April at a record high of 7,209, its best monthly performance in several years. The message from company boardrooms was clear, despite the turbulence around them, many businesses are continuing to grow and generate healthy profits.

Central Banks Between a Rock and a Hard Place

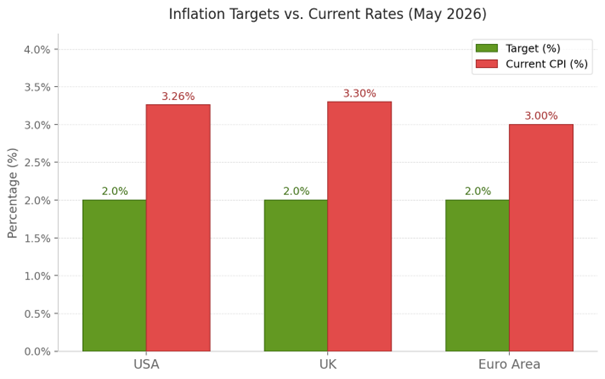

The last week of April brought a flurry of decisions from the world’s most important central banks, the institutions responsible for setting interest rates. In the United States, the Federal Reserve held its key interest rate unchanged at between 3.5% and 3.75%, in what turned out to be the final meeting chaired by Jerome Powell before his departure as Chair. The Bank of England kept its rate at 3.75%, and the European Central Bank held at 2.0%. All three arrived at the same conclusion: with inflation still running well above their targets, now is not the time to start cutting the cost of borrowing.

The reason prices are proving so difficult to bring down is largely because of the cost of energy. UK inflation rose to 3.3% in March, up from 3.0% the month before, and the Bank of England warned it could climb as high as 3.5% over the summer months ahead. In Europe, the picture is similar, with the ECB raising its inflation forecast for the year. Put simply, when the cost of filling up a car or heating a home goes up sharply, the knock-on effect ripples through almost every price in the economy. For investors, this means interest rates are likely to remain where they are for some time to come, and the prospect of cheaper borrowing costs, which markets had eagerly anticipated at the start of 2026, has been pushed back considerably.

(Source: ONS, Eurostat, US BLS)

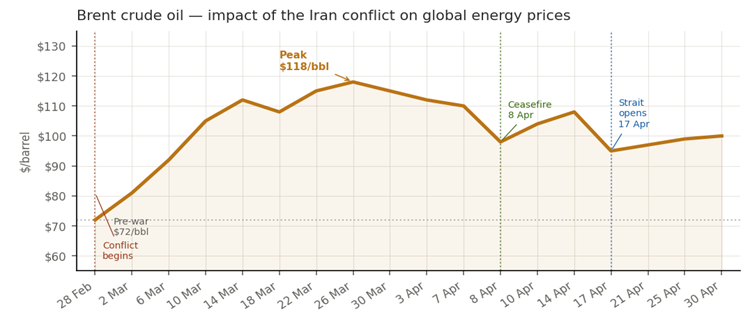

War, Ceasefire, Blockade, Repeat

April was a month of dramatic twists and turns in the Middle East, with developments moving quickly enough to whipsaw financial markets from one day to the next. On 8 April, a two-week ceasefire was announced between the United States and Iran, brokered by Pakistan, with Iran agreeing in principle to reopen the Strait of Hormuz, the critical shipping lane that had been effectively closed since late February. Share prices surged immediately on the news, with the oil price falling sharply on hopes that supply disruptions would ease.

However, the relief was short-lived. Peace talks held in Islamabad on 11–12 April collapsed without agreement, largely over two unresolved issues: who controls the Strait of Hormuz and what happens to Iran’s nuclear programme. Following the breakdown, the United States announced a naval blockade of Iranian ports, creating what observers described as a ‘dual blockade’, Iran restricting shipping through the strait, and the US restricting access to Iranian ports. In a partial breakthrough, Iran declared the strait open to commercial shipping on 17 April as part of a separate ceasefire in Lebanon, causing oil prices to drop by 11% in a single day.

But by the end of the month, the wider situation remained unresolved: Iran was still seeking war reparations and postponement of nuclear talks, while the US continued to insist on the nuclear issue being settled as part of any final deal. For markets, the conflict remains the single biggest source of uncertainty heading into the summer and we are continuing to monitor events closely and position portfolios accordingly.

(Source: Bloomberg, Reuters)

Portfolio Changes

During the month, we made a number of changes across our funds in response to ever changing financial conditions. Within fixed income, we sold the Royal London Short Duration Credit Fund, the Janus Henderson Strategic Bond Fund (Cautious and Balanced), and the JP Morgan Global Aggregate Bond ETF (Balanced), reinvesting into the PIMCO GIS Income Fund and the Schroder Strategic Bond Unit Trust. The changes provide greater flexibility and we feel they are better suited to navigate ongoing interest rate uncertainty.

Within our equity exposure, we sold the Liontrust UK Smaller Companies Fund in favour of the UBS MSCI United Kingdom ETF (Balanced and Adventurous), which focuses on larger, more established businesses, reflecting concerns around inflation and the likelihood of fewer interest rate cuts than previously expected. Finally, we switched from the Landseer Global Artificial Intelligence Fund into the Polar Global Technology Fund, which we believe offers greater flexibility across the AI and Technology sector and to benefit from the significant AI-related spending highlighted earlier.

BOOLERS INVESTMENT COMMITTEE