Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin August 2022

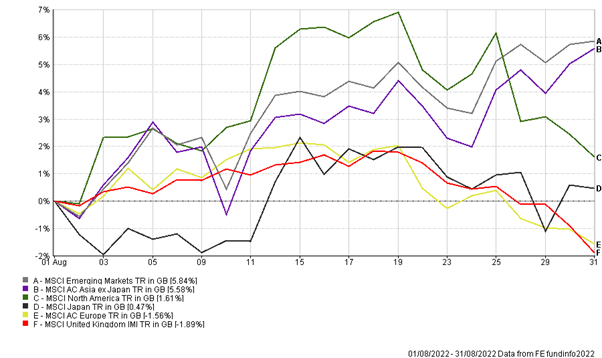

After a positive start to August, markets gave up some gains in the final week of the month, as investors reacted to Federal Reserve Chair Jerome Powell’s hawkish stance on US interest rates. The performance of the main indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

In what is normally a quiet month for news flow and trading volumes, Fed Chair Jerome Powell shook markets with his Jackson Hole Symposium speech, announcing his most hawkish message to date, with the US central bank’s determination to bring down inflation. In his speech, he highlighted that interest rates would need to stay higher for longer, which would restrain growth for ‘a sustained period of time’ and this would very likely lead to ‘some softening of labour market conditions’ and ‘some pain’ for consumers and businesses.

Despite US annual inflation falling to 8.5% in July from a 40 year high of 9.1%, the Fed Chair made it clear that a single month’s data clearly fell short of what the Federal Market Open Committee would need to see before they are confident that consumer prices are meaningfully moving lower.

Closer to home the Bank of England raised its benchmark interest rate from 0.5% to 1.75% to continue the fight against inflation which is now at a 40 year high of 10.1%. The Bank stated that the latest increase in gas prices by Russia’s restriction of supplies is likely to push inflation above 13% by the end of the year, with inflation to remain elevated throughout 2023 and eventually falling back to the 2% inflation target rate in two years’ time.

Governor Bailey highlighted that ‘there is an economic cost to the war’, UK households are more exposed to the energy price shock than US households, with the Bank estimating that the UK economy will contract in the fourth quarter of 2022 for five consecutive quarters and GDP will fall by more than 2% from peak to trough.

In the Far East, The People’s Bank of China (PBOC) cut its medium-term lending rate for one-year loans to the banking system by 0.1% to 2.75% and its five-year loan prime rate (LPR), a reference for mortgages, by 0.15% to 4.30%. The rate cuts in the second largest economy comes at the back of weaker than expected economic data for retail sales and industrial production in the month of July and repeated lockdown measures in several Chinese cities.

As shown in the chart above, Emerging and Asian markets outperformed over the month, as investors responded positively to the move by the PBOC, signalling Beijing’s commitment to boost economic growth. Further measures of looser monetary policy and fiscal policy are likely to take place if the economy continues to slow down, with price pressures not being an issue and the current annual inflation rate considerably lower at 2.7%, when compared to its western counterparts.

Over the month our portfolios moved broadly in line with markets, outperforming their respective benchmarks, which is a trend that continues throughout the year to date.

We acknowledge that markets and the global economy are currently going through a turbulent time, and you may have concerns regarding your investments. Our portfolios are continued to be managed with a view that over the long-term, equities will overcome these macroeconomic and geo-political challenges and a well-diversified portfolio is key to help mitigate risk in times of short-term market volatility. As such, as we have seen over the many years in managing portfolios, investors who take such a view will ultimately be rewarded for their patience.

As always, if you have any queries regarding your portfolios, please do not hesitate to contact your investment manager.

The Boolers Investment Committee