Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin August 2023

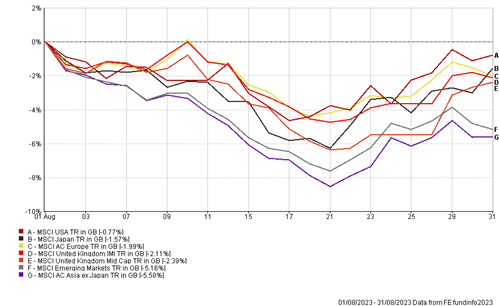

August has been a negative month for markets, due to the heightened volatility concerning China’s economic growth prospects combined with a potential slowdown in developed markets, because of higher interest rates. The performances of the main equity indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

In August, global investors turned their attention towards the Jackson Hole Symposium where major central banks discussed the prospects of monetary policy and the future of their economies. Federal Reserve Chairman Jerome Powell made it clear that US inflation remains too high (3.2% US headline inflation and 4.7% core inflation (ex-food & energy) and policy is likely to remain restrictive to bring down inflation, with further rate rises on the table until inflation sustainably falls to their 2% target rate. However, he also acknowledged that he needs to get the balance right between making sure the US central bank does not tighten policy too little, to let inflation get embedded in the system but at same time not raising rates too high to hinder economic growth.

Emerging markets and Asian stocks sold off during the month, as investors became more pessimistic about China’s economic outlook. Disappointing manufacturing data, signs of deflation, record youth unemployment and loss of confidence in China’s property sector all contributed to a decrease in fund flows from China’s mainland market. In response, the Chinese Ministry of Finance cut stamp duty and cut transaction fees for brokers to help stem the negative flows for Chinese stocks, with an aim to boost investor confidence.

In addition, in the property market local governments abolished rules that disqualify citizens who have ever had a mortgage from being considered a first-time homebuyer in major cities. This was to help mitigate a further drop in home prices and to curtail the number of property developers defaulting on their debt.

Despite the current negative sentiment regarding the Chinese economy, it is important to highlight that economic growth for the first half of this year was 5.5% and they are still on track to meet their targets for economic growth of 5% overall for 2023, following a 3% expansion in 2022, which is considerably better when compared to developed markets. The Chinese government have growth as their main priority and will continue to pursue policies to help support entrepreneurship and innovation in the private sector and overall animal spirits from consumers, likely at any cost.

In the UK, headline inflation fell to 6.8% in July from 7.9% in the previous month, due to lower gas and electricity costs. Although these figures are positive and heading in the right direction, the underlying price pressures in service inflation and overall wage growth remains too high, for inflation to fall back to the 2% target. This will likely result in the Bank of England continuing to raise interest rates, as they did at the start of August by 0.25%.

On the positive side, economic growth continues to be robust, with the latest data showing the British economy grew by 0.2% in Q2 2023, following a 0.1% expansion in Q1, beating economists’ forecasts of a flat reading. As time goes by, more consumers are likely to feel the pinch of higher rates, which is likely to result in a slowdown in consumer spending, and hence slower growth.

However, there are also a significant number of consumers and businesses that were able to lock in low interest rates in 2020 and 2021. Therefore, they are in a much better position in terms of personal finances and corporate balance sheets. A major slowdown is by no means a done deal, hence the economy and markets have remained resilient thus far. Over the long term, inflation is expected to fall as indicated by future consumer and business inflation expectations, which will be a net positive for equity prices.

In the short-term, volatility is part of the journey of investing in equity-based investments, mainly because of the swings in shorter term investment sentiment, regardless of the fundamentals of profitability and earnings potential of companies we own. We believe that over the longer term, markets will overcome any short-term negative sentiment and the companies that we invest in via the investment funds held within portfolios will continue to be profitable and their valuations continue to recover and move higher.

We believe the best way to navigate market volatility is to be diversified across different asset classes, investment styles (value, quality, growth & momentum), market caps of different sized companies (large, medium, small) and geographical regions. We also avoid reacting impulsively to sentiment-based swings in short prices that belie the fundamental valuer of assets held.

As always, your investment manager is happy to discuss any concerns you may have.

THE BOOLERS INVESTMENT COMMITTEE