Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin December 2022

Markets

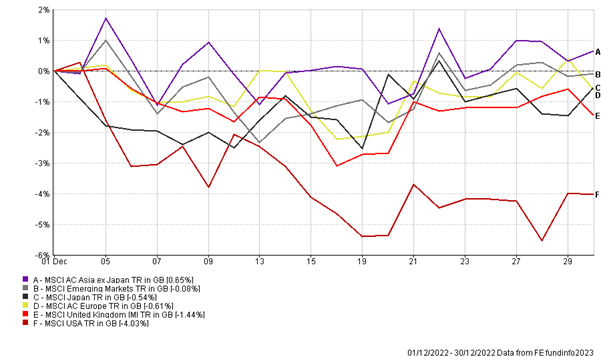

Markets finished 2022 on a mixed note, on what has been a volatile year for investors. The performance of the main indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

In its final meeting of the year the US Federal Reserve raised interest rates for the 7th consecutive time in 2022 by 0.5%, to a target range between 4.25% and 4.5%. The slower than expected move in interest rates is significant, as the pivot to smaller rate hikes was followed by the Bank of England and the European Central Bank, both raising their benchmark interest rates by 0.5% to 3.5% and 2.5% respectively. Most Economists now believe that inflation has peaked in these major regions with reductions in the US headline inflation rate falling to 7.1%, as well as annual consumer prices falling to 10.7% during November in the UK.

However, despite the encouraging signs of falling prices, central banks are still concerned that it will take a considerable amount of time before inflation falls to their 2% target rate. In his press conference, US Fed Chair Jerome Powell still emphasised that ongoing increases in the policy rate would still be appropriate and that the full effects of their policy tightening are yet to be seen in the US economy, to bring price growth under control both in the labour market and real economy.

December saw the Bank of Japan (BoJ) surprise financial markets with a change in its yield curve control policy. The BoJ announced that it will allow its 10-year bond yield to fluctuate by plus or minus 0.5% of its policy target rate of zero, instead of the prior range of plus or minus 0.25%.

The move by the BoJ is significant for investors because it shows signs that the BoJ are facing increasing pressures to end its ultra-loose monetary policy as global rates have risen. In addition, an annual inflation rate of 3.8% and the fact that the BoJ own a significant amount of Japanese government bonds, potentially may create liquidity problems in markets. The aim of the BoJ is to try and reactivate the market for Japanese bonds, which would see global yields rise and the Japanese Yen appreciate significantly against other major global currencies.

China announced wide relaxation of covid rules including allowing home quarantine for mild coronavirus cases rather than using quarantine facilities. In major cities such as in Beijing and Shanghai, provisions have also been relaxed with requirements to show a negative test before entering most public places being eradicated. The Chinese government also announced that it will remove any quarantine requirements for inbound travellers from 8th January. It is believed that the shift away from covid zero by Chinese officials will help boost domestic demand in the medium-term.

Over the longer- term, the impact of a policy shift from covid zero will also have positive spill-over effects for the global economy if China can sustainably implement re-opening policies throughout 2023 without crippling its health system. It can mean that global supply chains can begin to become robust again, China’s major trading partners can prosper from an increase in international demand and most importantly global price pressures can ease. In turn, the following should result in a rise in demand for global stocks.

Over the month our risk models have moved broadly in line with markets, continuing to outperform their respective benchmarks and peers, which was a common theme throughout 2022.

As always, should you wish to discuss your portfolio or markets more generally with your investment manager, then please do not hesitate to contact us.

We would like to take this opportunity to wish all our clients a Prosperous and Happy New Year.

THE BOOLERS INVESTMENT COMMITTEE