Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin February 2022

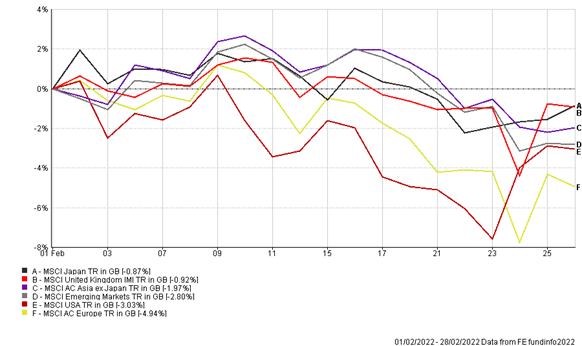

Markets were more volatile this month, as Russia began what appeared to be a ‘full-scale’ invasion of Ukraine and investors assessed the potential short-term and long-term impacts of the invasion on risk assets. Performance of some of the main indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling Terms)

In the shadow of rising geo-political tensions, central banks still mull over monetary policy tightening to control inflation. The Bank of England increased interest rates to 0.5% at the beginning of the month and voted to not reinvest any of the £875bn government bonds under their quantitative easing programme, as they forecast inflation to reach 7.25% in April. Currently, the Bank of England is treading a fine line between controlling inflation expectations without dampening down economic growth, as the labour market continues to remain tight and the economy continues to recover from the pandemic, with latest figures showing annualised GDP increased by 6.5% in the final three months of 2021.

In the US, the Federal Reserve minutes indicated that policy makers were unlikely to increase interest rates aggressively in March to tackle the 7.5% annual inflation rate. The minutes indicated that members of Federal Reserve were concerned that increasing rates too quickly would likely cause damaging effects on markets and the wider economy. This comes at the back of strong economic data from the US, which showed that first estimates of annualised GDP figures indicated economic growth accelerated by 7% in the final quarter of 2021 and the number of jobs created in January in all non-agricultural businesses increased by 467,000 beating economist’s estimates significantly.

As highlighted in our recent Ukraine conflict update, our portfolios continue to be invested in equity and non-equity assets, diversified across different geographical regions, sectors and companies. We still believe equities will continue to outperform other asset classes over the medium to long-term, as company fundamentals remain intact, hence investors which take such a view on their portfolios will ultimately be rewarded.

Portfolio Changes

With the increase in market volatility, we have taken the opportunity to reduce our exposure to Emerging markets equities (and in part Russia), with the sale of our holding in the UBS Global Emerging Markets Equity Fund. For now, monies have been retained as additional cash during this volatile period.

Tax Year End

We are approaching the end of the tax year and will be focusing on utilising ISA (and Capital Gains Tax) allowances where possible within existing portfolios. If you would like to contribute to your ISA allowance(s) out of cash, then please contact us accordingly.

The Boolers Investment Committee