Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin February 2024

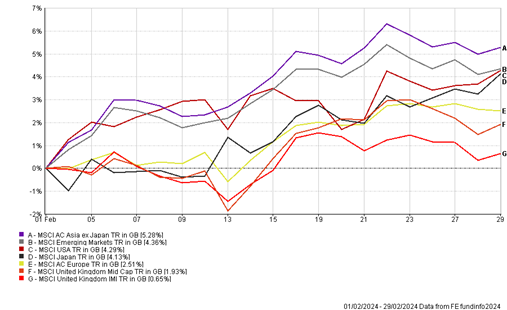

We start our commentary by highlighting the performance of the main equity indices over the month, as shown below.

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

China – Value Trap or Value Opportunity?

Emerging and Asian market equities outperformed over the month as Chinese authorities boosted stock prices by encouraging institutional investors to hold A-shares (domestic listed shares) for a longer period, with more buying from state run financial institutions. Much of the buying focused on exchange traded funds tracking the CSI 300 Index and other mainland stock market benchmarks.

For Chinese equities to outperform over the longer term, more fiscal policy support is needed to boost the economy to see a sustained bounce back in consumption, exports, employment, and incomes. This is unlikely to happen overnight as it requires structural reforms at the state and local level. Therefore, there is still a lack of confidence and economic weakness which will hamper the future profitability of Chinese companies.

However, the good news is that the Chinese economy has a lot of room to improve which may provide an upside to corporate earnings in the medium term. We continue to monitor our China exposure and remain overweight in Asia and Emerging markets which contributed positively to performance this month.

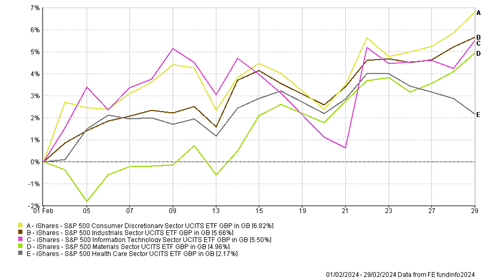

Magnificent Seven vs S&P 493

US technology stocks continued their positive performance in February, as Nvidia reported positive earnings and sales revenue for the fourth quarter of 2023, beating expectations. The company has been a beneficiary regarding the market’s fixation with artificial intelligence models, which are developed using Nvidia’s graphics processers for servers.

Even though technology has continued to lead markets in 2024, in February we saw a broadening out of US equities with 10 of the largest companies providing 74% of the returns in February year to date, down from 90% in January.

As a result, other sectors such as consumer discretionary, healthcare, industrials and materials provided positive contributions to performance, with companies having more certainty on the cost of capital compared to last year and a better than expected earnings season with 73% of S&P 500 companies exceeding EPS estimates for Q4 2023.

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

Japan – Party like it’s 1989?

The Nikkei 225 closed at an all-time high, surpassing its past record which was last set in December 1989. However, in 1989 valuations were much more stretched, with the Nikkei 225 having an average P/E ratio of 70 times earnings as the rally was driven by liquidity. This time round valuations trade at a P/E ratio of 28 times earnings and has been driven more by corporate fundamentals such as increased dividends and share buybacks.

So far, large cap companies who are big exporters to the rest of the world have outperformed because of yen devaluation over the past few years. However, there is a sense that this could change as the Bank of Japan begins normalising monetary policy and the yen starts to appreciate. This would boost mid/small-cap businesses that are more domestically orientated in terms of revenues and earnings.

For this rally to continue, Japanese companies must continue to increase their profitability by increasing their margins to catch up to the rest of the world in providing value to shareholders. This is starting to happen but is being implemented at a slow pace.

THE BOOLERS INVESTMENT COMMITTEE