Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin February 2025

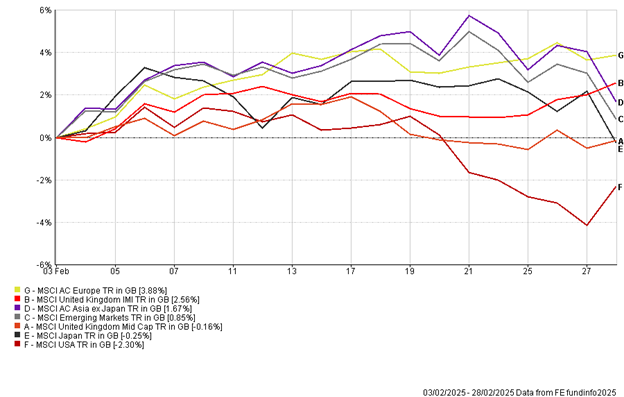

Global markets had a mixed month overall, with Europe, UK and Asia/Emerging markets leading the way and the US underperforming due to economic growth concerns. The performances of the main equity indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

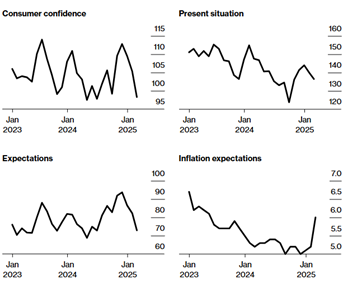

US Growth Scare?

US equities fell over the month, as investors became concerned about the sustainability of economic growth. Recent data by the Conference Board showed that consumer confidence declined at the fastest pace since 2021, while consumer inflation expectation levels rose to the highest level since 2023.

This tells investors that consumers are reacting to the uncertainty around trade, tariffs and actions of the Department of Government Efficiency (DOGE). As a result, we saw the biggest selloff in the ‘Magnificent 7’ technology stocks, which have higher valuations than the rest of the market.

US consumers are key to the US exceptionalism story, which has led to strong earnings from companies across different sectors. Although economic uncertainty does lead to a delay in spending decisions, it is important to highlight unemployment levels currently remain low and consumer balance sheets remain strong. If individuals are employed, they will continue to borrow and spend money to fund their lifestyle, which will support economic growth over the medium term.

Source: The Conference Board

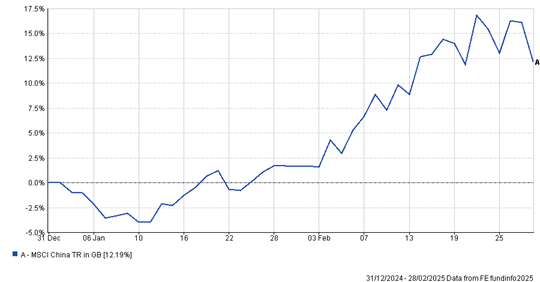

The China Bounce

Chinese equities have been one of the shining stars this year so far, as cheap valuations and the growing adoption of Artificial Intelligence across sectors helped boost sentiment in the region. Earnings expectations of companies are low and surprises to the upside in earnings have helped share prices rise. Alongside this, investors expect that this year, the Chinese Communist Party will implement long-term growth measures to stem the tide of the deflationary spiral, with a focus on the low-income groups that have strong consumer balance sheets.

However, tariffs, geo-political concerns and a weak property market are still of concern to investors and things can easily shift the other way, as we have seen in the past. For now, we believe that our current Chinese exposure remains appropriate, and we continue to be selective in the opportunities in China given the discounted share prices on offer.

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

European Equities Lead the Way

European equities have been the best performing market this year, as the threat of US tariffs look less threatening than first thought. This has led to the lowering of the risk premium for investing in equities in the region. This, combined with low valuations, the prospects of further European Central Bank (ECB) rate cuts and higher than expected corporate profits, has resulted in a rise in investor sentiment.

Approaching 2025, investors expected the effect of tariffs and weaker growth to put pressure on European equity valuations and as a result analysts downgraded earnings. Last year was a concentrated market, with US technology stocks helping US indices to reach all-time high valuations. The expectation was that this would continue indefinitely.

The improvement in both China and Europe along with the UK this year, highlights the importance of having exposure to a diversified range of assets across different markets to help manage risk, while providing comprehensive returns, whatever the prevailing market narrative echoed by analysts and strategists.

THE BOOLERS INVESTMENT COMMITTEE