Amandeep Mandair

Reveal Menu

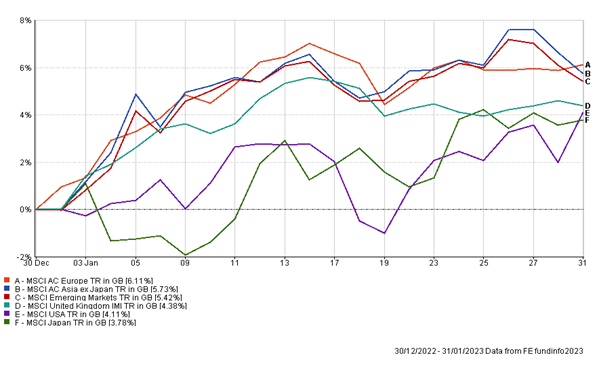

Market Commentary: Monthly Bulletin January 2023

Financial markets started the year on a firm footing, with both global equities and bonds moving in a positive direction. An uptick in returns was largely due to China’s relaxation of rules surrounding their Zero Covid policy as well as a relatively mild winter in Europe, which eased pressure on the Energy Crisis, with average gas purchase prices falling in comparison to 2022 highs. The performance of the main indices are highlighted below.

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

A resilient jobs market in the US continued to support equity movements, as the January labour market report showcased stronger than expected increase in job vacancies, as well as a fall in the unemployment rate to a 53-year low of 3.5%. Nonetheless, investors remained heavily focused on inflation figures as well as further manoeuvres in the Fed’s tighter monetary policy regime. Headline CPI dropped from 7.1% to 6.5%, as energy and food prices started to moderate, with investors now pricing in for slower rate rises from the Federal Reserve as wage price pressures also begin to ease. Whilst markets have pared back some losses from 2022, investors remain cautious of whether this is a bear market rally or a longer trending theme for positive gains. Earnings season also made headway at the beginning of the year, with 4th quarter results indicating domestic earnings are compressed and forecasting a lower growth guidance. The S&P 500 blended earnings for the quarter showcased a decline of -5.3%, indicating economic uncertainty is set to continue in the short term.

UK equities also mirrored the performance of overseas counterparts, as the FTSE 100 reached highs of 7,860 during the month supported by sectorial performance in consumer discretionary and financials. UK small and mid-cap equities particularly outperformed as the UK domestic market showed signs of resiliency, indicating a predicted ‘soft landing’ is more likely. UK manufacturing PMI edged higher to 47 in January up from 45.3 in December, as reducing gas prices supported this. Downward momentum in the annual inflation rate also caused some optimism in markets as the rate fell from 10.7% to 10.5%, matching market expectations.

Although some areas of the UK economy have shown signs of strength, weakened demand in retail and home sales points towards an ongoing economic slowdown, with a higher proportion of consumers on short term fixed mortgage rates, which will continue to cause a squeeze on spending throughout 2023.

Signs of cooling inflation and loosened Covid-19 restrictions led to robust gains for Chinese equities over the month. The latest region to relax its rules was Beijing and with peak infection rate in some cities having passed, the outlook on the Chinese economy looks more promising. In addition, the IMF revised its annual growth forecast from its October forecast of 4.4% to 5.2%, further signalling an improved macro backdrop for China should lead to a sustained recovery over the course of 2023.

Moreover, curbs on property developers and easing of regulation on China’s technology companies is a tailwind for Chinese equities over the medium-longer term, however the extent of government stimulus to support these areas of the market remains in question. In the wider context, a resurgence in China’s constrained consumer and investment activity will support global demand as well as easing pressures on global supply chains.

In other parts of the Far East, the Bank of Japan remained centre stage, following the surprise adjustment of the yield curve control policy In December from +/- 0.25% to +/- 0.5%. Although, there was speculation that the policy may be altered in the January meeting, the policy remained unchanged. Further intervention from the BoJ in bond markets may have implications on its balance sheets and a balancing act between controlling inflation which currently stands at 4% year-on-year and quantitative tightening may become problematic.

Over the month our risk models have moved broadly in line with markets, starting the year on a positive note.

Part way through the month, we have sold our position in the iShares FTSE 100 ETF taking advantage of the strong performance of UK equities in the short term. The proceeds have been retained as cash, pending reinvestment.

As always, should you wish to discuss your portfolio or markets more generally with your investment manager, then please do not hesitate to contact us.