Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin January 2024

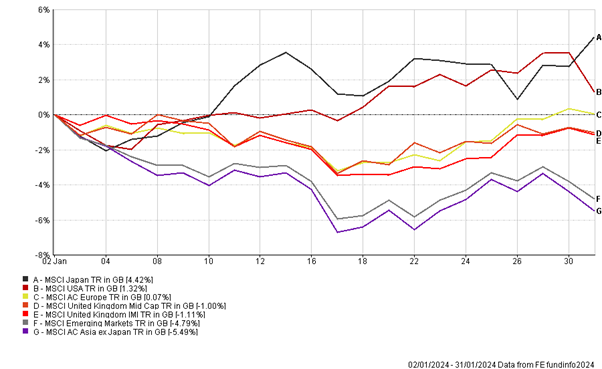

We start our commentary by highlighting the performance of the main equity indices over the month, as shown below.

The start to the year resembled the hangover after the Christmas and New Year’s Eve parties as, after a very positive end to the year, global equity markets pulled back slightly before recovering towards the end of the month, with the exception of Asia/China.

Inflation – Stick or Fold?

Many believe the inflation battle has been won and focus is turning to when interest rates will fall and this has been a positive backdrop for both equity and bond markets. On the other hand, some still see ‘sticky’ inflation remaining stubbornly above the central bank targets and thus rates will not fall as much as has been priced into markets and, as and when data releases have supported this view, markets have generally pulled back.

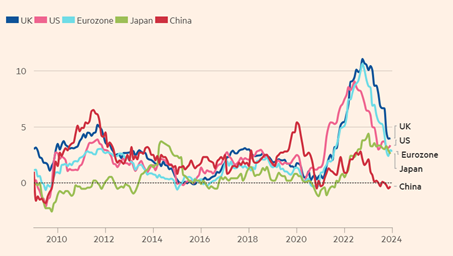

Despite bond yields having ticked back up slightly this year, we do believe that there has been sufficient rate increases to see further inflationary pressures reduce and that interest rates will start to reduce, in the second half of the year. The chart below highlights the movement in global inflation over the longer term and moving back to a more normalized level.

Global Inflation

Source: FT/Refinitiv

Yul Brynner or Denzel Washington?

You may be fortunate enough to remember the original film or the remake of The Magnificent Seven. Either way, the main technology stocks that have coined the film title continue their path to eternal glory with, in the main, another positive start to the year.

The valuations of these companies have become more expensive and arguably the potential earnings are fully priced in their current share prices. Latest earnings for Alphabet (Google) and Microsoft for Q4 2023 beat revenue and earnings (per share) estimates, however, not as much as investors’ expectations. Therefore, this is an example that any slowdown in revenues or earnings, which are below market expectations, could easily see valuations under greater scrutiny.

We believe that the concentration in the US stock market is adding further risk to portfolios and whilst we do have exposure to the S&P 500, we are diversified across other US stocks, both in style and size.

China’s Woes

Whilst China’s economy has continued to grow at a reasonable pace, this masks the underlying issues presented by their failing property sector and the impact of enforced regulation, both reflected in the weakness of their stock market. The former has certainly come to light this month with the news on the expected liquidation of their major property developer, Evergrande, and Chinese authorities continue to mull over various measures for stabilizing their stock market.

We remain cautious over China in the short term and this is reflected in our underweight position relative to our benchmark. Longer term China may present more opportunities and we continue to keep this under review.

Portfolio Changes

This month we have taken the decision to reduce our cash weighting within portfolios introducing the Vanguard UK Government Bond Index Fund. The fund will increase our exposure to UK Gilts, complementing our existing fixed interest funds and adding diversification to our equity exposure, whilst locking into attractive yields and the potential capital upside as and when interest rates fall.

As always, should you wish to discuss your portfolio or markets more generally with your investment manager, then please do not hesitate to contact us.

THE BOOLERS INVESTMENT COMMITTEE