Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin January 2025

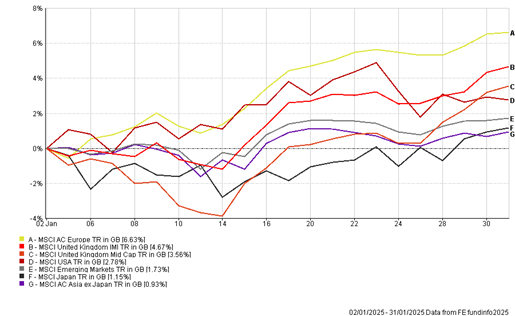

January was generally a mixed month for markets, as investors assessed what economic policies Donald Trump would pursue as he became the 47th President of the United States. The performances of the main equity indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

The Global AI Race

This month we saw the release of DeepSeek’s latest R1 model which is China’s answer to Open AI’s ChatGPT. This free, open-source AI search engine is more efficient and can run on less advanced Nvidia chips and is trained for real-time problem solving. It is now the number one free app downloaded on the apple store. This news sent shock waves through equity markets and particularly US technology, as Nvidia lost $592.7 billion in market cap in one day.

So, is this the beginning of the end of US technology dominance? We think not, in fact, the release of DeepSeek is bullish for technology and the adopters of AI in general. Since the creation of the first computer in the 1950’s, technology has become more efficient and cheaper to run overtime as companies innovate and competition increases.

A more cost-effective advancement in an AI model means companies like Nvidia, Microsoft Alphabet and Meta will be able to get access to a larger universe of customers across different industries that will demand more AI solutions (a larger percentage of users that would not have considered using AI). Although lower margins may put pressure on valuations in the short-term, the long-term efficiency of these businesses will increase, as costs are reduced because these companies will have to invest less in their own AI infrastructure such as data centers, helping to boost cashflows and margins over time.

Trump’s Tariffs

On 31st January, President Trump announced that he is planning to implement tariffs on US’s major trading partners. It is expected that 25% tariffs will be implemented on Mexico, Canada and 10% additional tariffs on China on most goods imported from the region.

When Trump last threatened to impose tariffs in 2019, he used them as a negotiation tactic to stem the flow of immigration, announcing an increase in tariffs by 5% every month until Mexico undertook measures to stop illegal immigration into the US. The result in 2019 was Trump calling off an increase in tariffs with Mexico after the two countries met at the negotiation table. It appears that this is déjà vu, as leaders in Canada and Mexico will likely meet with Trump to discuss and reach an agreement between countries.

Nevertheless, it is important for investors to be aware which sector would be hit the most with any potential tariffs. In the interim, it is likely that automakers which have global supply chains and massive exposure to Mexico and Canada will be hit the most. In addition, China revenues for Asian chip manufactures are also likely to be hit with the likes of Samsung and Taiwan Semiconductor Manufacturing both likely to come under pressure given the US aims to keep the most advanced chips away from China.

Portfolio Changes

This month we sold Artemis Income Unit Trust, reducing our UK overweight exposure to take advantage of the recent positive performance. We will be aiming to redeploy the cash shortly to take advantage of any short-term market volatility in the best valuation opportunities available.

THE BOOLERS INVESTMENT COMMITTEE