Amandeep Mandair

Reveal Menu

Market Commentary: Monthly Bulletin July 2022

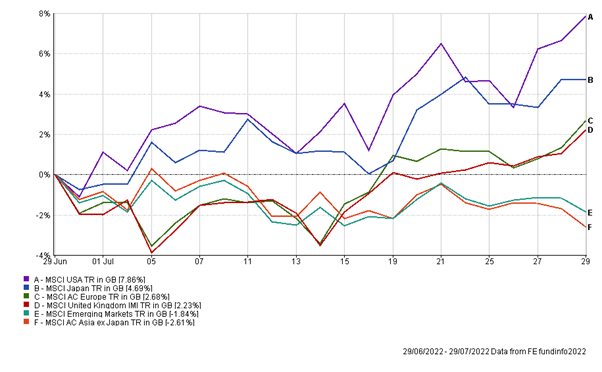

Markets continue to trade on choppy waters against a backdrop of weaker growth and tighter financial conditions. Economic data further evidencing a slowing global economy, led to markets increasingly pricing in interest rate cuts at the beginning of 2023, which supported risk assets in some geographical regions over the month. The performance of the main indices are highlighted below:

The Fed reaffirmed market expectations as they continue to hike interest rates into restrictive territory to rein in inflation. The most recent FOMC meeting concluded a widely expected 75-basis-point rate increase, however, with a surprisingly dovish tone from Fed Chair Jerome Powell in the post-meeting conference paired with underwhelming economic data, this could lead to rate hikes winding down sooner than anticipated, which markets received well. GDP contracted by an annual rate of 0.9% in the second quarter sending the US into a technical recession, as the economy experienced two consecutive quarters of negative growth, however, at this point, the National Bureau of Economic Research are hesitant to formally declare a recession as the labour market remains resilient.

Q2 earnings season also took centre stage towards the end of the month, as investors eagerly awaited earnings-per-share (EPS) news from the likes of Alphabet and Apple. With 56% of S&P 500 companies having reported results and 73% of those companies reported a positive EPS surprise, earnings surprised to the upside, beating market expectations. Nonetheless, developed markets remain under pressure to EPS downgrades, with expected headwinds to valuations over the short term.

The economic impacts of the Ukraine/Russia conflict continued to be felt across the Euro area, as the IMF recently downgraded economic growth to 2.6% for 2022 and slashed its projection for 2023 from 2.3% down to 1.2%. The European Central Bank also boasted tighter financial conditions, delivering a half-point increase in its deposit rate this month, as consumer prices jumped to 8.9% a year earlier in July. Rising prices paired with fears of gas shortages over the winter months in the region will lead to prolonged volatility, particularly across European market indices, however, this will also present investment opportunities over the longer term.

Economic indicators in the UK also suggested a more subdued economic backdrop as UK manufacturing PMI moved lower to 52.1, as factory activity slowed due to weaker market demand and transportation delays. In addition, UK inflation hit a new 40-year high of 9.4% and was above market expectations as the cost-of-living crisis deepens. The Bank of England implemented a 25-basis point hike in July, with the committee suggesting a 50-basis point hike may be necessary in its August meeting to ease inflation. Nonetheless, major UK market indices posted their strongest month in performance over the course of July as upbeat earnings from financials, such as NatWest, supported an uptick in UK markets.

China continued to navigate its way through the Covid outbreak, with some cities softening the zero covid policy restrictions, nonetheless, major announcements are not expected until the Party Congress in the Autumn, where a more stringent strategy in its Covid policy will be implemented. The impacts of Covid controls led to GDP growth of 0.4% in the second quarter, as the economy struggled to accelerate an anticipated economic recovery. In addition, ongoing woes in the property market weighed in on the MSCI China index returning -9.3% over the month, however, Beijing plans to set up a real estate fund worth between CNY 200-300 billion to support developers, which may be the light at the end of the tunnel for the sector.

As we have commented previously, during this volatile period in markets we continue to manage our portfolios with the belief that equity-based investing remains appropriate over the medium to long-term and investors who are patient and adopt such an approach, will ultimately be rewarded. We of course are monitoring markets closely and will take any appropriate action we deem necessary to adapt to the continuously changing macro-economic and geo-political environment.

If you have any queries regarding your portfolio, please do not hesitate to contact your investment manager.

The Boolers Investment Committee