Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin July 2023

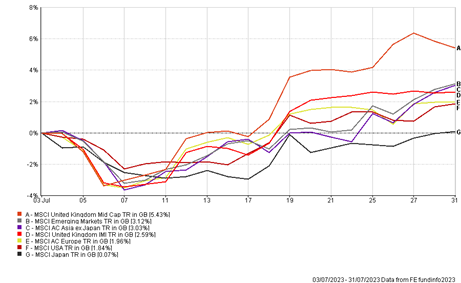

Markets rebounded strongly after a slow start to the month as core inflation numbers continued to remain sticky and economic data remained positive, despite rising interest rates. The performance of the main equity indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

Annual US inflation fell to 3% in June, which helped boost ‘soft landing’ market sentiment that the Federal Reserve can bring down inflation to their target of 2% without causing a recession or major slowdown. However, core inflation which strips out volatile items such as food and energy has been stickier, with core consumer prices falling to only 4.8% in June, well above their target.

As a result, in their July meeting the Federal Reserve raised interest rates by 0.25% to a range of 5.25 to 5.5%. In his subsequent press conference, Jerome Powell mentioned that further rate hikes are a possibility if the economic data warranted it, with the full effects of the Fed’s tightening yet to be felt by the US economy. Markets are now pricing a 50/50 chance of another interest rate increase later this year and a full expectation of rate cuts early in 2024.

UK inflation fell sharply to 7.9% in June after fuel costs and core service inflation eased. Markets are anticipating that the easing of price pressures should help slow the rate of interest rate increases with a higher probability of slower increases baked into markets, as shown by the boost in share prices for UK mid-cap companies. The biggest issue for the Bank of England continues to be sticky service led inflation and wage growth from the private sector which continues to remain strong. However, as with the other major developed markets we are still yet to see the full effects of monetary policy tightening and as these kick in, we will see a looser labour market that will start to reduce wage and service led price pressures.

Asian & Emerging markets had a positive month despite China’s lower than expected GDP expansion of 0.8% from the previous quarter, due to falling exports and weak retail sales and a lagging property sector. This year we have seen a trend of global investors increasing flows to other Asian and emerging markets ex China such as South Korea, India, Taiwan and Indonesia that have all been beneficiaries of increased investment from companies diversifying their supply chains away from China. In addition, such economies have much better growth prospects, nearing the end of their interest rates cycles, much earlier than developed markets.

However, on a valuation basis compared to developed markets, China remains attractive, with much better starting valuations and given its significant contribution to global growth (roughly one third), an allocation to China in our portfolios remains appropriate in our view.

The Bank of Japan (BoJ) slightly altered its ultra loose monetary policy by announcing it would offer to buy 10-year Japanese bonds at 1%, in effect widening the trading band on long-term yields. The move is to prevent inflation moving too far away from the 2% target rate, and a way to provide greater flexibility in pursuing yield curve control to help achieve stable prices and strong growth, with the latest figures showing prices rising to 3.3% in June on an annual basis. However, further moves in increasing the trading range for long-term yields will be dependent on further wage gains, with the BoJ announcing that they would not hesitate to intervene if the 10-year Japanese bond yield ever traded above 1%.

Over the month our risk models have moved broadly in line with markets, continuing to outperform their respective benchmarks and peers both on a short and long-term basis.