Duncan Pickering

Reveal Menu

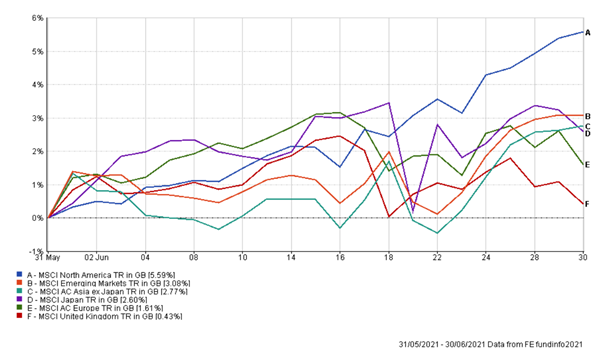

Market Commentary: Monthly Bulletin June 2021

As the second quarter draws to a close, markets continue to gain traction (notably in the US), as economies gradually re-open and many countries progress with their mass vaccination programs. Performance of some of the main indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

The noise surrounding inflation has seemingly been getting louder as we move into the second half of 2021. However, markets appear more convinced that elevated inflation will be transitory, as much of the increase in prices reflects post-covid supply and demand imbalances. We expect to see some normality in the medium term, as disruptions in supply chains caused by the pandemic resolve themselves.

In the US, following the Fed meeting on June 16th, a more hawkish Jerome Powell reiterated 2 hikes in interest rates are on the cards in 2023, with the Fed actively discussing Quantitative easing tapering to start early next year. In the meantime, markets have reacted well to positive economic data, with consumer and business confidence indicators pointing towards economic expansion.

Simultaneously, stronger than expected economic data in the UK continues to support market indices, as manufacturing PMI suggested a robust growth in activity over June as we continue to periodically lift lockdown restrictions. Although the official reopening was delayed by a further four weeks, a spike in household savings (up by 3% from the previous quarter) supports the view that consumers have plenty of firepower to support a rebound in spending over the coming months. Inflation has taken centre stage, as the MPC predicted CPI exceeding 3% this year, however with the view the higher inflation is transitory, policy tightening is unlikely in the near term.

Inflation on the other hand eased in the Eurozone down from 2% to 1.9% in June, as energy prices growth slowed to a moderate pace, further supporting an accommodative fiscal policy at least until the ECB’s September meeting. Positive consumer confidence, paired with a strong rebound in business sentiment across the Eurozone, led to a boost in market outlook with the likelihood of upward revisions in economic growth. However, headwinds are still prominent as the impact of the delta variant is yet to unfold fully.

Over the month our portfolios have generated positive returns, building upon the strong start to the year overall and we remain above our stated benchmarks.

The Boolerss Investment Committee