Prabhdeep Gill

Reveal Menu

Market Commentary: Monthly Bulletin June 2024

Markets were mixed over the month, with US technology stocks outperforming, followed by Asia/Emerging market equities due to better-than-expected economic data from China. The performances of the main equity indices are highlighted below:

(All figures are based on bid-to-bid pricing with income reinvested, in Sterling terms)

The Strong Get Stronger

In the US, the equity market has been driven by momentum and speculation, with investors increasing their allocation to those ‘Mag 7’ stocks (Apple, Amazon, Alphabet, Meta, Microsoft, Nvidia & Telsa). These stocks tend to have quality characteristics of strong free cash flows, meaning they can reinvest for future earnings growth, which helps them maintain leadership in their respective sectors. One of the main sources of growth for these companies is from betting that Artificial intelligence (AI) will become increasingly important to productivity in the global economy.

Based on the current valuations and projected earnings growth, it appears that investors agree that this will be the case. For example, Nvidia, which engineers the most advanced chips needed for AI reached a $3 trillion dollar market cap, making it the most valuable company on the planet before selling off from all-time highs.

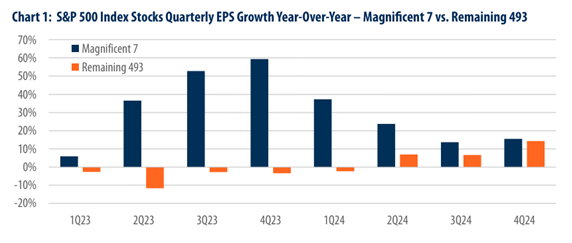

However, the question remains whether earnings growth which is baked into current share prices is sustainable in the future. While earnings growth for the first quarter of this year was dominated by the Mag 7 and technology stocks. What is significant is that earnings growth rates for those names are anticipated to slow this year while the rest of the market is expected to have an increase in earnings growth. By the 4th quarter of 2024, the rest of the market is expected to be growing as fast as these technology companies, as highlighted in the chart below.

Source: First Trust

For example, small and mid-cap companies trade on significantly cheap discounts compared to their large cap peers. Faster earnings growth combined with better starting valuations indicate great opportunities for active fund managers to outperform in a broadening market.

The Year of Elections – Don’t mix politics with portfolios

French President Emmanel Macron called a snap election early this month following the success of far-right parties in the EU elections in June. Financial markets in Europe have responded negatively to the possibility of the Far-Right National Rally (RN) led by Marie Le Pen forming a government.

Days after the announcement by President Macron, we saw the French CAC 40 Index down by more than 6%, wiping out the majority of gains year to date. The risk-off sentiment was also mirrored in the bond market with the spread between the French and German 10-year government bond yields reaching their highest point since February 2017.

The most likely outcome according to the latest polls is that the RN wins a relative majority rather than achieve a clean sweep and markets have responded positively so far. However, the good news for investors in Europe is that large cap multinational companies tend to generate majority of their revenues overseas therefore any fallout from the French election is likely to be muted, with earnings generation still being a key determinant of share prices.

In the UK, the latest polls are showing that a Labour majority is the most likely outcome on the 4th of July.

In truth, it seems equity investors are relatively relaxed about the impact on markets given there is not much difference between the parties’ plans. It is expected that there will be higher spending under Labour than the Conservatives, which will be a positive for smaller and mid cap companies, which are more geared toward the domestic economy than companies that are listed on the FTSE 100.

The benchmark FTSE 100 is up around 7% so far year to date and with inflation falling to the Bank of England’s 2% target this month, rate cuts are just around the corner which will further support UK equities. One potential headwind for the main index is the uncertainty around what Labour does with its energy policy given its plans to pursue a £1.2 billion windfall tax on the sector.

In terms of the UK Gilt market, the front end of the yield curve is priced in for two rate cuts from the Bank of England this year and any disappointment may send bond yields higher. The benchmark 10-year gilt is expected to remain at around 4% with uncertainty over longer term spending and fiscal plans from the new Government.

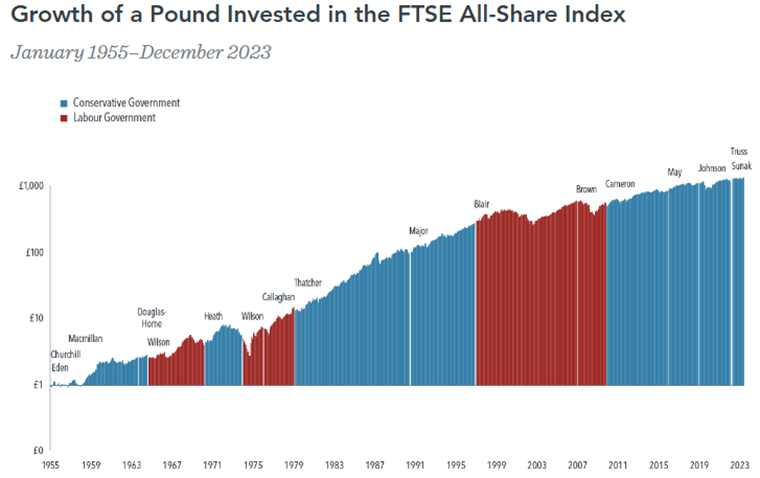

Overall, history has shown that policies put in place by governments can have some influence on share prices, however, there are many factors that drive returns, interest rates, inflation, oil, geo-politics and tech advances to name a few.

As shown in the chart below, no matter what policies are pursued, share prices ultimately reflect company fundamentals and ‘time in the market’ rather than ‘timing the market’, is the most important factor for achieving positive returns.

Source: 7iM

Later in the year we have the US Presidential election and whilst interest is increasing with the first televised debate between the two candidates, there has been little reaction from markets so far.

The Central Bank Conundrum – When to cut interest rates?

The good news for major central banks is that inflation has continued to fall to their target rate and there is a consensus in global markets that we are finally going to see monetary policy easing which should support risk assets.

In June, the European Central Bank (ECB) was the first major central bank to cut interest rates by 0.25% to 3.75%, citing that the fall in the deposit rate was in response to a more than 2.5 percentage point fall in Eurozone inflation since September 2023. In the UK, it is expected that the first interest rate cut of 0.25% will take place at the Bank of England’s August meeting.

However, in the US, a question mark remains over when the Federal Reserve (Fed) will make their first move. The Fed’s preferred gauge of price pressures Core Price Consumption Expenditures (PCE) fell to 2.6% in the year to May, helping to keep the central bank on course for at least one interest rate cut this year, with investors expecting September being the mostly likely month the Fed will cut interest rates by 0.25%.

The delay in rate cuts this year has been down to sticky core service inflation and wage growth because of a stronger than expected labour market. In addition, there is a sense that the Fed is afraid of making the same mistake as it did in 2021 of calling inflation ‘transitory’ and falling behind the inflation curve and then having to raise rates aggressively. If rates were to be cut prematurely and inflation were to pick up again, this would result in aggressive rate hikes, which would decrease consumer and investor confidence.

However, cutting too late could result in a slowdown in economic growth through a rise in unemployment, which would be negative for risk assets. At this point, the risks of a policy mistake are finely balanced, but we would say skewed to the upside, given the strength of company earnings and the trend rate of falling inflation.

Portfolio Changes

During the month, we have reduced our cash weighting within portfolios.

For Balanced and Adventurous risk clients we have added cash to the Polar Healthcare Blue Chip fund to provide further global equity exposure and the long-term trend for increasing health demand. We have also added to the fund for Cautious clients with a slight reduction in our exposure to M&G Global Listed Infrastructure fund.

For Cautious risk clients we have added cash to our holding in the Vanguard UK Government Bond fund to add further diversification to our equity exposure and to benefit from future interest rate cuts.

THE BOOLERS INVESTMENT COMMITTEE